For CFOs evaluating equipment acquisitions before year-end, the financing structure is not an administrative detail. It determines whether your business captures a full tax deduction in the current year or loses it entirely. Get the structure right and you can acquire revenue-generating equipment with no money down, reduce this year’s taxable income, and preserve working capital at the same time.

The One Big Beautiful Bill Act (OBBBA) makes this window more valuable than it has been in years. The Section 179 deduction limit now stands at $2,560,000 for 2026. Bonus depreciation is permanently restored at 100% with no sunset date. These provisions are available now. Whether your business captures them depends on how the financing is structured before December 31.

The Two Tax Levers Every CFO Should Understand Before Q4

Two federal provisions drive most year-end equipment tax planning. Understanding how they interact changes the conversation with your CPA before a single lease document gets signed.

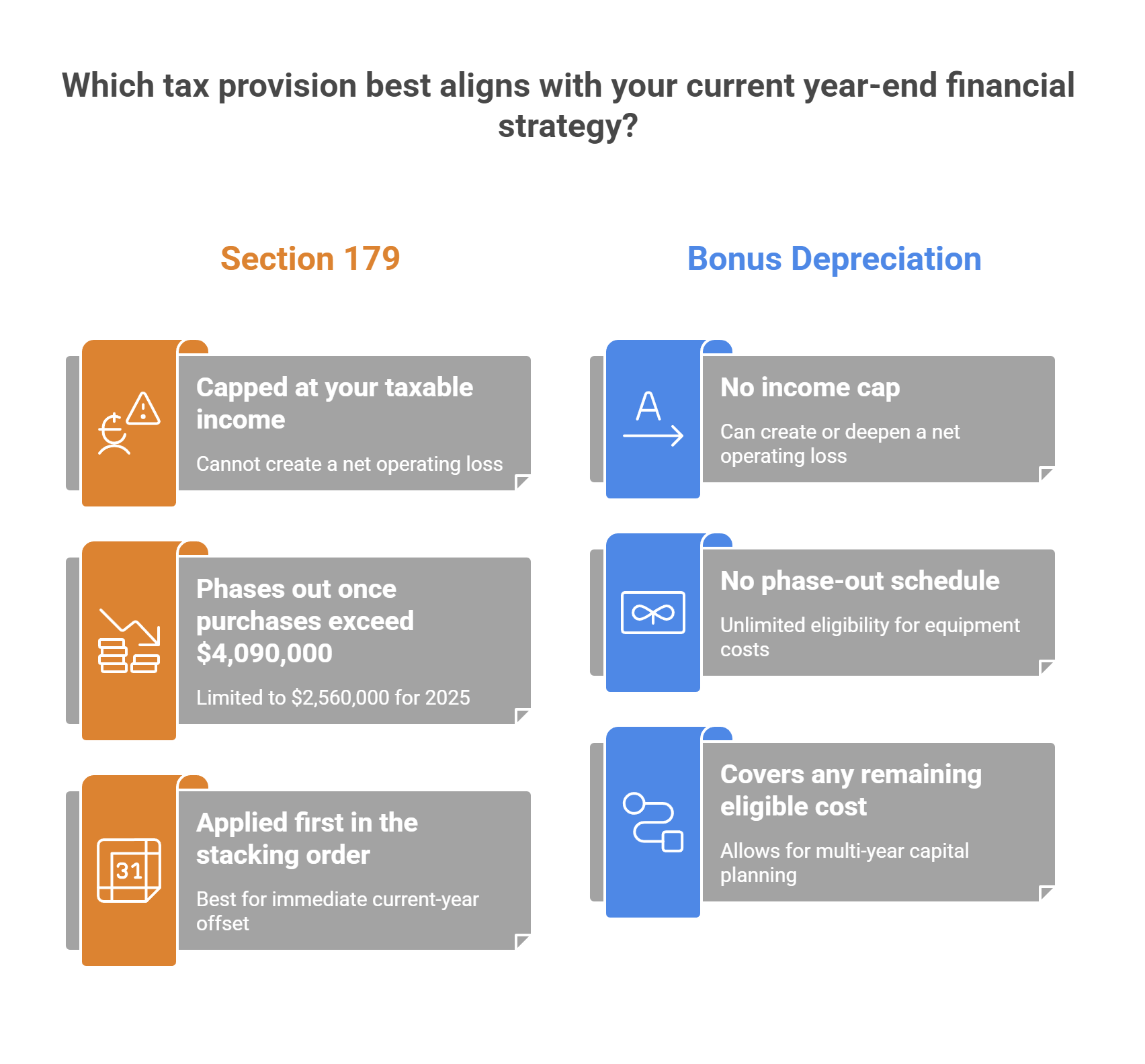

Section 179 allows a business to deduct the full purchase price of qualifying equipment in the year it is placed in service, up to $2,560,000 for the 2025 tax year. The deduction phases out dollar-for-dollar once total equipment purchases exceed $4,090,000. One important constraint: Section 179 cannot create a net operating loss. Your deduction is capped at your taxable income.

Bonus depreciation works differently. Under the One Big Beautiful Bill Act (OBBBA), Congress permanently restored 100% bonus depreciation with no income cap and no expiration date. Bonus depreciation can create or deepen a net operating loss, which carries forward to future tax years. The stacking order matters: Section 179 applies first, and bonus depreciation covers any remaining eligible cost.

Buddy Zarbock, Founder and CEO of Commercial Funding Partners, LLC, has followed the legislative history of bonus depreciation closely through his work on ELFA’s Political Action Committee and the AACFB Board. His perspective on the OBBBA restoration: “The permanent reinstatement of 100% bonus depreciation changes the math for businesses doing multi-year capital planning. You no longer have to time every acquisition around an artificial sunset date. But year-end still creates a real trigger for businesses with current-year income they want to offset.”

The OBBBA eliminated the old phase-down schedule (40% in the pre-2025 period) that forced Q4 panic buying. That does not make timing irrelevant. It means timing is now a strategic choice rather than a legislative deadline. For businesses with significant current-year taxable income, acting before December 31 still produces a measurable tax result.

See also: tax benefits of equipment financing for CFOs and how tax law changes affect used equipment

How Your Lease Structure Determines Your Tax Treatment

Lease structure is not a product preference. It is a tax planning decision. Two businesses buying the same piece of equipment can end up with entirely different tax outcomes depending on how the financing is structured. See the lease vs. buy comparison for additional context on this decision.

| Structure Type | Tax Treatment | Best For |

|---|---|---|

| Dollar-Out Capital Lease | Treated as a financed purchase. Lessee claims Section 179 and/or bonus depreciation. Interest payments are separately deductible throughout the term. | Businesses with significant current-year taxable income seeking maximum Year 1 deduction. |

| FMV Operating Lease | Lease payments are deductible as ordinary operating expenses. Lessee does not claim depreciation. Off-balance-sheet treatment. (ASC 842 note: accounting classification may vary.) | Businesses prioritize cash flow predictability, balance sheet positioning, or technology refresh cycles. |

| Equipment Loan | Full ownership from day one. Lessee claims depreciation, including Section 179 and bonus depreciation. Interest deductible. | Businesses that want ownership and direct control of depreciation timing. |

Dollar-Out Capital Lease: The Purchase Treatment

The IRS treats a dollar-out capital lease as a financed purchase. Because the lessee acquires ownership of the equipment at the end of the term for $1, the transaction is treated as a loan for tax purposes. The lessee, not the lessor, claims depreciation. That means Section 179 expensing and bonus depreciation are available in the year the equipment is placed in service, subject to applicable limits and your tax position.

Interest paid throughout the lease term is also separately deductible as a business expense. This gives a dollar-out capital lease two distinct layers of tax efficiency: the depreciation deduction in Year 1 and the interest deduction spread across the payment schedule.

This structure fits businesses that expect significant current-year taxable income and want to offset it aggressively. For a detailed look at how lease structure affects the purchase vs. lease decision, review our lease vs. buy comparison.

FMV Operating Lease: The Expense Treatment

A fair market value (FMV) operating lease functions as a true lease. The lessor retains ownership, and the equipment stays on the lessor’s books for depreciation purposes. The lessee deducts lease payments as ordinary operating expenses, which keeps the accounting straightforward and the deduction predictable.

Section 179 and bonus depreciation do not apply to the lessee under an FMV operating lease. The trade-off is that the deduction does not depend on taxable income thresholds. Payments are deductible whether or not the business shows a net profit in that period.

This structure fits businesses managing balance sheet exposure, working through technology refresh cycles, or simply prioritizing payment predictability over maximum Year 1 deduction. As Traci Dolphin, President of Equipment Leases, Inc., puts it: “We always refer them to their accounting specialist.” Neither structure is universally superior. The right choice depends entirely on your tax position and year-end goals.

How 100% Financing Preserves Cash While You Capture the Deduction

A widely misunderstood point: you do not need to pay cash for equipment to claim Section 179 or bonus depreciation. The deduction is taken when the asset is placed in service, not when the payment method is used. Equipment financed through a qualifying capital lease or loan is fully deductible in the year placed in service, regardless of how much came out of pocket.

We offer 100% equipment financing that covers the full project cost: equipment, shipping, installation, and warranties. A business can put $0 down, deploy revenue-generating equipment immediately, and still claim the full Section 179 or bonus depreciation deduction for that tax year.

The interest paid on the financing adds a second layer. Under the OBBBA, Congress also restored the 30% EBITDA-based cap on business interest deductions (Section 163(j)), reversing the tighter EBIT-based standard that had applied in prior years. That restoration means more of your financing interest may be deductible than it was before January 2025.

The practical math: equipment is generating revenue from the day it is installed. Those revenues cover the monthly payments. The deduction reduces your current-year tax liability. Your working capital stays intact. These outcomes are not in conflict. They are the point.

For businesses with expiring tax positions or year-end income spikes, a delayed acquisition means lost deductions. The window is fixed; the financing does not have to be.

Ready to move? Get a quote today and find out if your year-end equipment financing qualifies for Section 179 or bonus depreciation deductions.

The Placed-in-Service Rule and Why Q4 Timing Is Not Flexible

This is where year-end deals succeed or fail. To qualify for a current-year deduction, equipment must be in your possession, set up, and operational by midnight on December 31. Signing a lease agreement before year-end is not sufficient. Placing an order is not sufficient. If the equipment does not arrive and become ready for its intended use before the calendar turns, the deduction belongs to next year.

Long-lead equipment ordered in mid-November may not arrive until January, disqualifying the deduction entirely. Custom machinery, specialized medical devices, and heavy construction equipment all carry lead times that can stretch into Q1 without careful coordination between vendor, lender, and logistics.

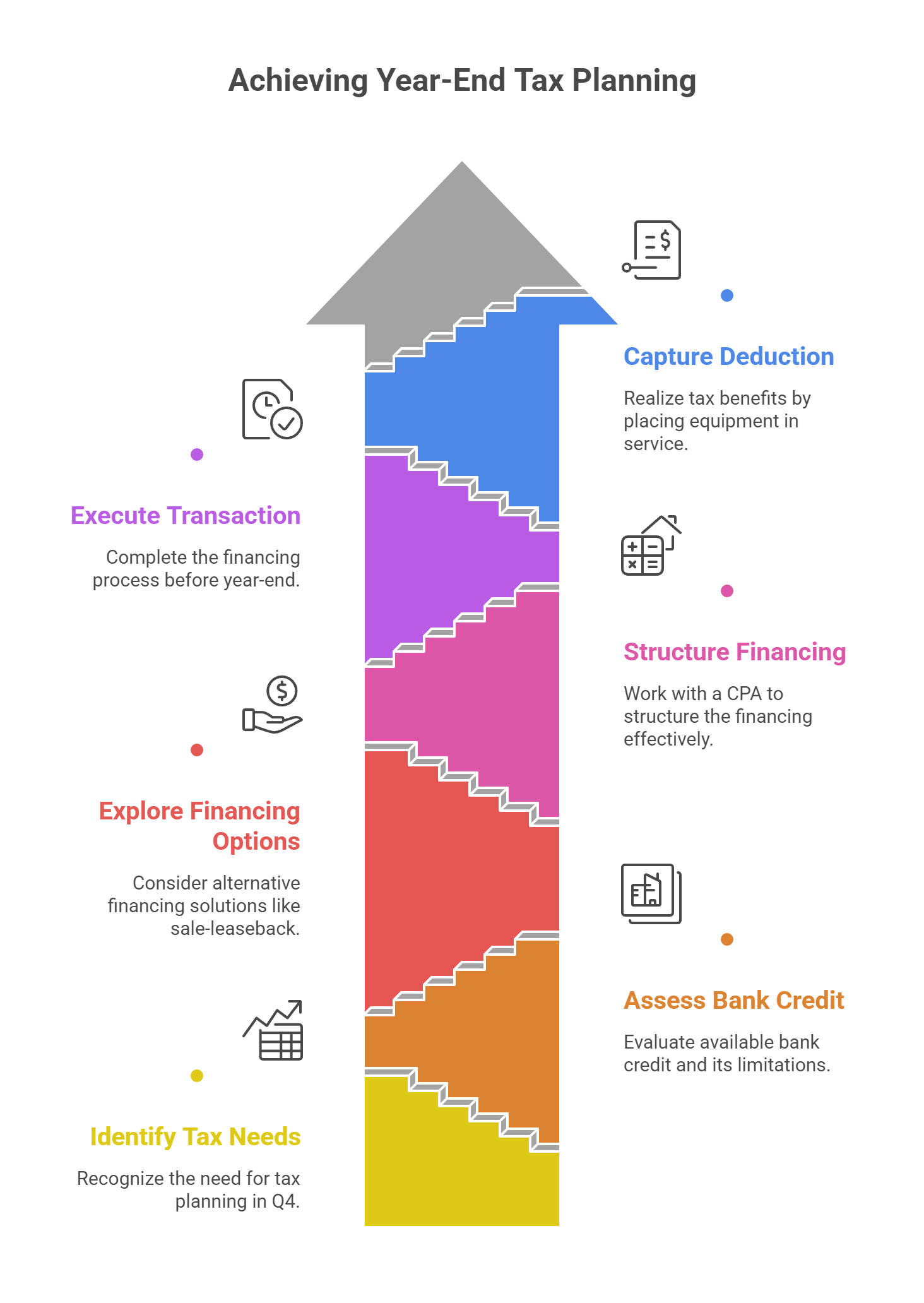

Year-End Action Timeline

| Month | Action |

|---|---|

| October | Begin conversations with your CPA about current-year taxable income and target deduction amount. |

| Early November | Identify equipment, confirm vendor lead times, and initiate financing conversations. |

| Mid-November | Submit financing application. We return same-day credit decisions for most mid-ticket transactions. |

| Late November | Receive letter of intent (24-48 hours for transactions in the $100K-$500K range). Confirm delivery and installation schedule with vendor. |

| Early December | Execute lease documents. Coordinate delivery and installation. |

| Mid-December | Equipment placed in service. Confirm operational status with your team and document for IRS purposes. |

| December 31 | Hard deadline. Equipment must be operational. Documentation should be complete. |

Finance leaders who begin this process in October or early November protect their options. Those who wait until mid-December frequently run out of runway, not because financing is unavailable, but because the equipment cannot physically arrive in time.

For additional guidance on the process, review our equipment financing FAQs.

Master Lease Structures for Businesses Planning Multiple Acquisitions

A master lease agreement establishes the financing framework once. Adding new equipment schedules under that agreement requires minimal new documentation. For businesses planning multiple equipment acquisitions across Q4 or anticipating capital needs that extend into Q1, this structure eliminates the administrative friction of restarting the financing process for each transaction.

Traci has described the practical benefit directly: once a master lease is in place, adding equipment is straightforward. The credit relationship is already established, the documentation framework is in place, and new schedules can be activated quickly. That speed matters when December deadlines are compressing the timeline.

Master leases are particularly suited to manufacturers, contractors, and healthcare operators running parallel capital projects with overlapping fiscal-year timing. A company acquiring three pieces of equipment across October, November, and December can manage all three under a single structure rather than three separate financing conversations.

This is not just administrative convenience. Efficient structuring now protects your ability to move fast on future acquisitions without reopening the credit process and risking a placed-in-service deadline on each new item.

When Bank Credit Reaches Its Limit

Many companies arrive in Q4 with compelling tax-planning needs and limited bank credit available. Bank exposure caps and covenant structures do not flex for year-end opportunities, regardless of how strong the underlying business case may be.

We operate as a complementary financing source to banks. Equipment is the sole collateral. There are no liens placed on receivables, no impact on existing bank credit agreements, and no disruption to your primary banking relationship. Buddy’s perspective on this is direct: “We help them expand upon what their bank services are.” The bank remains the primary relationship. We handle the equipment.

This is not a fallback position. It is a structure designed specifically for growing businesses that have outpaced their primary lender’s capacity at a given point in time. A manufacturer with $9M in funded equipment upgrades, a contractor managing a multi-phase build, a healthcare operator financing imaging systems across two locations: none of these are credit failures. They are businesses that have grown faster than their bank credit lines.

For businesses in this position, our equipment sale-leaseback option may also provide year-end liquidity that does not depend on new credit approvals. A sale-leaseback on existing owned equipment converts a fixed asset into operating capital while keeping the equipment in service.

Review our full financing programs to identify the structure that fits your Q4 position.

Bring Your CPA. We Handle the Rest.

Traci describes our role clearly: we are not tax consultants. We always refer clients to their accounting specialist. Our job is to structure the financing so that when the CPA confirms the timing and the structure, we are ready to move immediately.

That division of responsibility is not a limitation. It is how year-end deals actually get done. The CPA models the tax outcome. We close the financing. The equipment gets placed in service before December 31. The deduction is captured.

We have structured transactions across manufacturing, construction, medical, food processing, and energy sectors. Deals have ranged from application-only transactions under $250K to $9M equipment upgrades that repositioned a Florida manufacturer to win major new production contracts. The credit experience on our team spans 34 years. The execution timeline, same-day credit decisions, and 24-48 hour letters of intent are built specifically for situations where the calendar is a factor.

The window is real. The structure matters. The timing is not flexible.

Connect with our team today. Same-day credit decisions. 24-48-hour letters of intent. Let’s make sure your December 31 deadline is covered.

For more details, see our equipment financing FAQs and financing programs.