The headline cost of a major equipment purchase is rarely the whole story. Finance leaders must determine the investment return after taxes, financing costs, and capital deployment trade-off. This determines your actual return.

The tax benefits of leasing vs. buying equipment are not uniform. They depend on your company tax position and cash flow objectives. Equipment leasing changes the after-tax ROI equation through specific, measurable mechanisms.

The Right Framework: Why After-Tax ROI Is the Only Number That Matters

Gross cost comparisons ignore the variables that drive outcomes. These include tax treatment, opportunity cost of capital, and the time value of money. Comparing a monthly lease payment to a loan payment is often the wrong starting point.

After-tax ROI accounts for equipment costs net of deductions. It also considers what preserved capital earns elsewhere. This framework helps you evaluate the cost of waiting for deferred output.

The two primary options are the dollar-out capital lease and the FMV operating lease. We direct every client to their CPA or tax advisor before finalizing any structure. The right answer depends on numbers only they can see.

For a closer look at how lease structures affect tax outcomes, see our guide to equipment lease tax benefits for CFOs.

The Capital You Don’t Spend Can Generate a Higher Return Elsewhere

When a company buys equipment outright, that capital is tied up. It cannot be redeployed into payroll or growth investments. These investments might deliver a higher return per dollar than a static asset.

Most lenders finance the equipment. We finance the project. This means covering the asset, shipping, installation, and warranties so you stay liquid.

Manufacturers adding production lines need capital in reserve. So do contractors and healthcare providers. Equipment financing keeps productive cash available rather than locked into a single purchase.

Retained capital stays available for uses that may generate returns above the financing cost. That is the foundational ROI argument for leasing, and it holds before a single tax deduction is considered.

The Dollar-Out Capital Lease: Ownership, Depreciation, and Tax Efficiency

A dollar-out capital lease is treated as a financed purchase for tax purposes. Ownership transfers to the lessee for $1 at the end of the term. This allows the business to claim depreciation or Section 179 expensing.

For finance leaders managing taxable income, this is a tool for liquidity. It provides predictable payments to protect cash flow. It also creates first year tax deductions to lower net costs.

The combination of tax benefits and ownership fits companies with consistent taxable income. This is a capital efficient way to acquire equipment without an initial cash outlay. Ownership is automatic after the final payment.

Section 179 and Bonus Depreciation: What CFOs Need to Know

Section 179 lets businesses deduct the price of qualifying equipment in the year it is placed in service. This is subject to applicable IRS limits. We invite you to contact us to discuss how these limits align with your current acquisition plans.

100% bonus depreciation was restored through the One Big Beautiful Bill Act, Public Law 119-21, signed July 4, 2025. For a dollar-out capital lease, the lessee may be eligible for both deductions. This is subject to IRS classification and CPA guidance.

Buddy Zarbock, Founder & CEO, Commercial Funding Partners, was active in D.C. with the ELFA PAC to protect these provisions. This legislative work helps ensure clients have access to specific tax tools. Buddy remains engaged in protecting these corporate tax programs.

Fixed Payments, Full Ownership, No Residual

The dollar-out structure has a higher monthly payment than an FMV lease. This is because it leads to full ownership. Since the $1 transfer is automatic, there are no residual fees or purchase negotiations.

For sectors like manufacturing or energy, this matches financing to the life of the machine. The CFO gets predictable cash and a clear ownership timeline. This combination is difficult to replicate through outright purchase without deploying substantially more capital upfront.

The FMV Operating Lease: Lower Payments, Deductible Expenses, and Balance Sheet Flexibility

An FMV operating lease is structured as a true lease. The business makes lower monthly payments throughout the term. At the end, you can purchase at fair market value, renew, or return the asset.

Lease payments are typically deductible as business operating expenses. This means a predictable annual deduction. It aligns with actual payments made without depreciation schedules to track.

Traci Dolphin, President, Equipment Leases, Inc., brings 34 years of finance experience to these decisions. Traci notes that some clients prefer lower payments while new equipment ramps up. Others prefer the path to ownership through dollar-out structures.

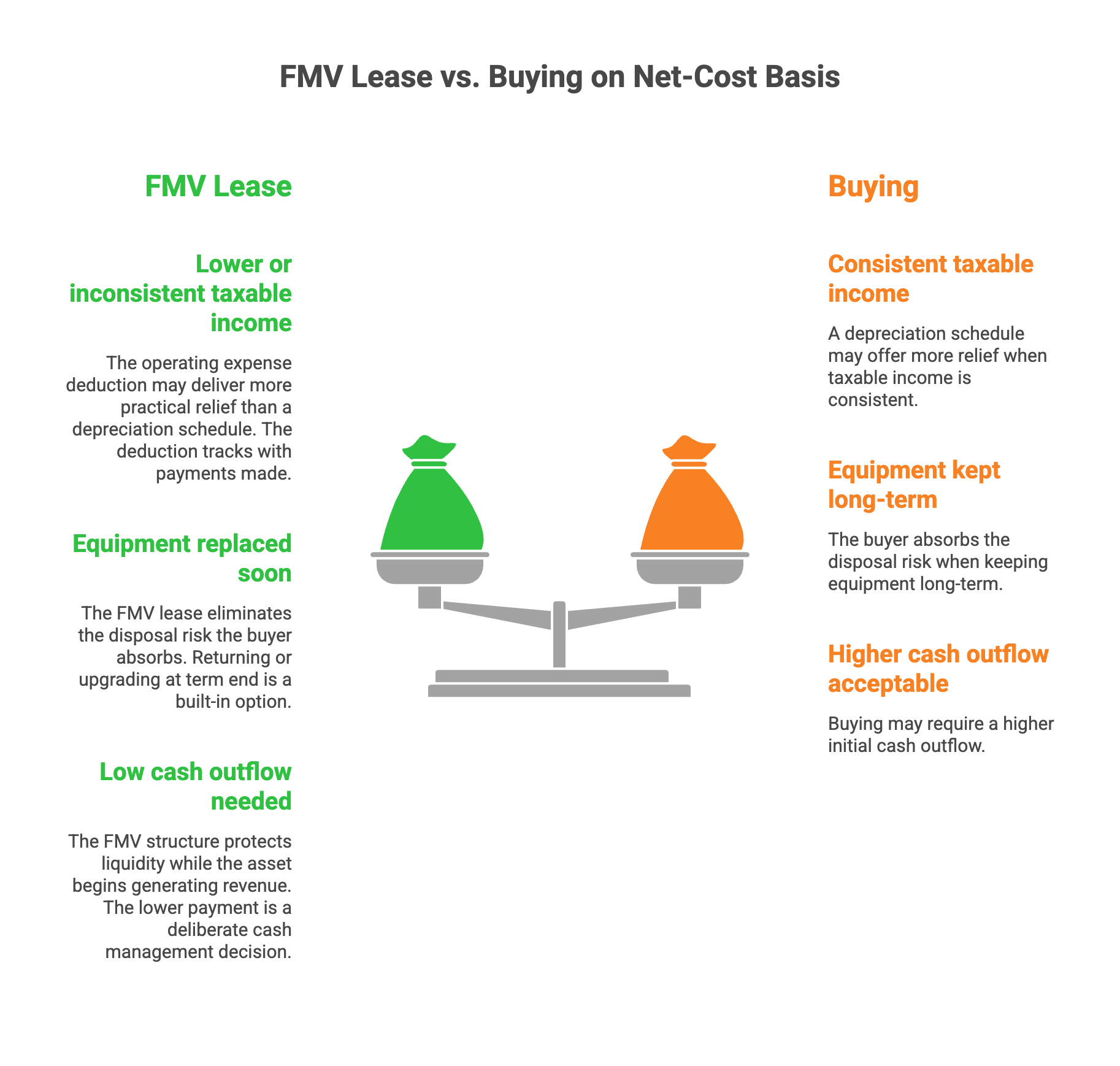

When an FMV Lease Outperforms Buying on a Net-Cost Basis

The tax benefits of leasing are not uniform. Three scenarios favor the FMV operating lease on a net-cost basis.

- Taxable income is lower or inconsistent. The operating expense deduction may deliver more practical relief than a depreciation schedule. The deduction tracks with payments made.

- The equipment will be replaced soon. The FMV lease eliminates the disposal risk the buyer absorbs. Returning or upgrading at term end is a built-in option.

- The business needs low cash outflow. The FMV structure protects liquidity while the asset begins generating revenue. The lower payment is a deliberate cash management decision.

A lease vs. buy equipment cost analysis that accounts for these scenarios reaches a better conclusion than a rate comparison. True lease accounting requires a review to ensure proper tax categorization.

Balance Sheet Management and Bank Covenant Protection

The accounting treatment of FMV operating leases differs from capital leases. This may affect financial ratios or covenant headroom. Contact our experts to discuss how to structure a lease for balance sheet purposes.

Our lien structure does not change regardless of lease type. The financed asset is the sole collateral. We place no blanket liens on receivables or inventory. This preserves your existing credit lines and protects your bank relationship.

Sale-Leaseback: The ROI That Is Already Sitting in Your Equipment Yard

A sale-leaseback allows a business to sell existing equipment and lease it back. Full use of the equipment continues without interruption. The business receives an immediate cash injection.

A masonry company with $9 million in equipment unlocked $8 million in capital this way. They used the funds to acquire a competitor. They executed a strategic move they could not have funded otherwise.

The question for CFOs is what existing equipment returns while sitting on the balance sheet. Often the answer is nothing. A sale-leaseback converts idle equity into deployed capital.

Explore our equipment sale-leaseback programs for structure details and eligibility.

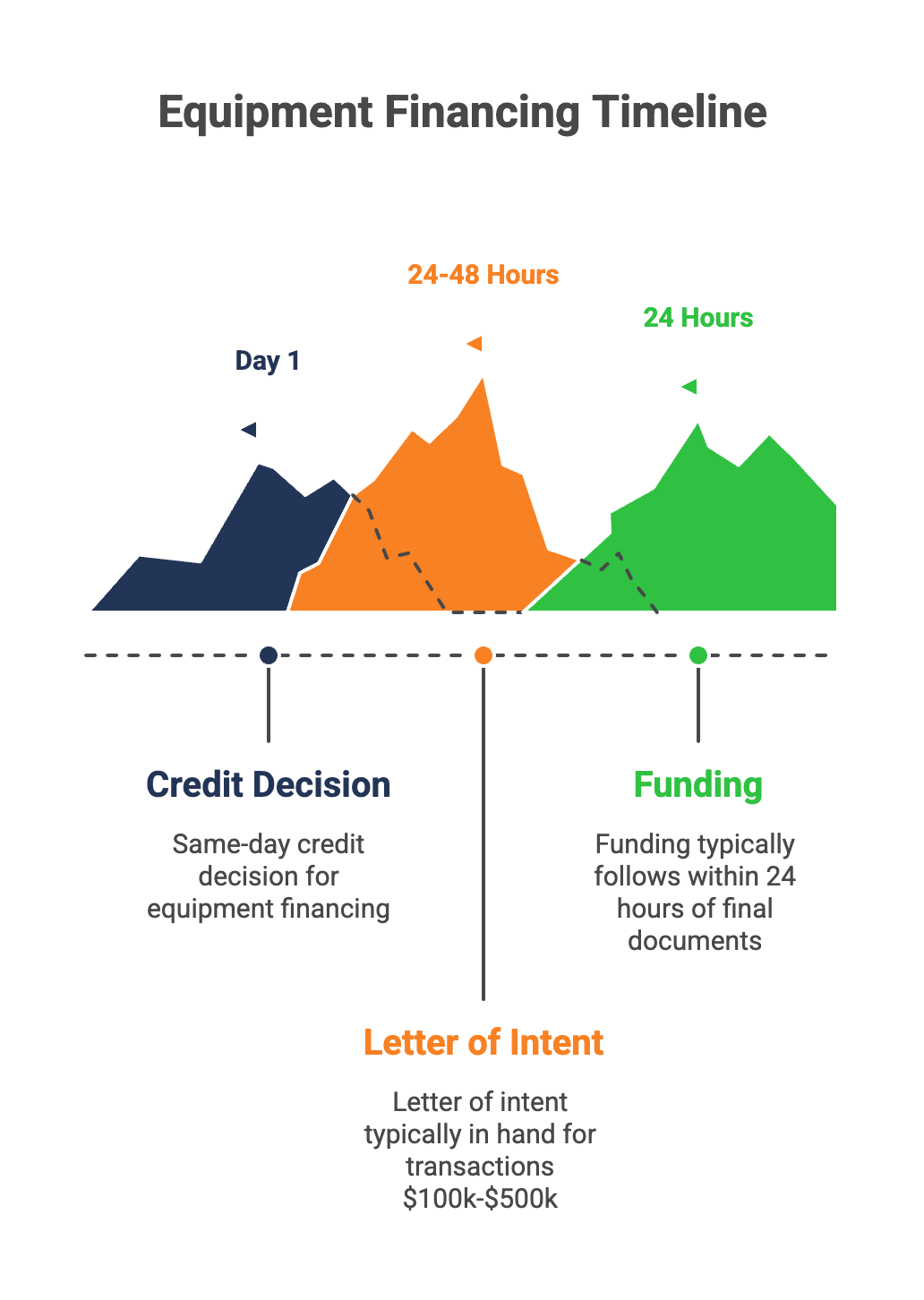

Speed Is a Financial Variable: How Fast Financing Compresses Your ROI Timeline

Delay has a real dollar value. New equipment not yet deployed is not generating output or revenue. Every month between a decision and funding matters.

When evaluating equipment financing, cash flow management extends beyond monthly payment size. Manufacturers adding production lines cannot absorb that gap. Slow financing extends your ROI timeline while fast financing compresses it.

We deliver same-day credit decisions. For transactions between $100,000 and $500,000, a letter of intent is typically in hand within 24 to 48 hours. Funding typically follows within 24 hours of final documents.

Buddy frames the rate comparison directly. A small rate difference is recovered in the first month of operation. This holds when financing moves months faster than a bank or SBA timeline.

Bank-Complementary Structuring: Protecting Your Total Cost of Capital

We operate as a bank-complementary source. For CFOs funding a project, this helps protect existing credit lines. Covenant headroom remains intact because we use an equipment-only lien approach.

Most lease vs. buy equipment cost analyses do not account for this. They should. The financed asset is the sole collateral. We do not use blanket liens on receivables or other assets.

Buddy describes the model directly. We help clients expand beyond what their bank provides, not replace it. The CFO walks away with equipment funded and working capital intact.

Protecting that financing cost structure is itself a measurable ROI input. That requires a partner who understands both sides of the balance sheet, not just the equipment.

The Expertise Behind Every Lease Structure

Traci brings prior mortgage and commercial underwriting experience to equipment finance. Her practice of directing clients to their CPA is not a formality. It reflects a commitment to the complete financial picture.

Buddy participated in Washington advocacy with the ELFA PAC to preserve tax provisions. That engagement keeps us current on regulatory developments. This affects the after-tax return on investment for every client we serve.

Together, they have structured transactions from $250,000 to $100 million across manufacturing, medical, construction, energy, and pharmaceutical sectors. Seventy percent of our leases are repeat business. Our credit committee is small, senior, and built for speed.

Meet the Equipment Leases team.

Structure Your Lease for Maximum After-Tax Return

The financing structure you choose will shape the return you realize. This is true for new acquisitions and for capital tied up in assets you already own. We help you evaluate the best path forward.

We work with finance leaders across every major U.S. industry to improve after-tax outcomes. Our 100% equipment financing strategy covers hard and soft costs. This keeps tax structure at the center of the decision.

Bring your CPA or tax advisor to the conversation and we will handle the financing. We move at the speed your business requires.

Apply Now for Equipment Financing | Explore Financing Programs