If you have spent any time researching equipment financing structures, you have probably run into a frustrating mix of terms that seem to mean the same thing but do not. The terminology is genuinely inconsistent across lenders, accountants, and the IRS, and choosing the wrong structure without understanding the differences can have real consequences for your business.

At Equipment Leases, we work with two primary structures: the dollar-out capital lease and the FMV operating lease. This post explains both in plain language. It compares them across the dimensions that matter most to CFOs and finance leaders, and helps you identify which set of priorities points toward which structure, so you can have a more productive conversation with your CPA and your financing partner.

The tax information in this post is for general educational purposes only and does not constitute tax, legal, or financial advice. Every business situation is unique. Always consult a qualified CPA or tax advisor before making equipment financing or tax planning decisions.

First, a Word on Terminology

Before comparing structures, it helps to understand why the terminology around equipment leases is so inconsistent in the first place.

“Tax lease” is not an accounting term. It is an IRS concept. It refers to whether the lessor or the lessee is treated as the tax owner of the equipment. That determination drives who claims depreciation and how payments are deducted. “Operating lease” and “capital lease,” on the other hand, are accounting classifications governed by GAAP.

These two systems use different tests and can produce different classifications for the same transaction. An operating lease is generally treated as a true lease for IRS purposes. The reverse is not always guaranteed. This is a common source of confusion, and it is worth naming directly before going further.

Layered on top of that, individual lenders use their own terminology. At Equipment Leases, we use two plain-language terms:

- Dollar-out capital lease: The lessee makes fixed payments over the lease term and acquires the equipment for $1 at the end. Ownership transfers automatically.

- FMV operating lease: The lessee makes lower payments over the lease term and, at the end, chooses to purchase the equipment at its then-current fair market value, renew the lease, or return the equipment.

Everything that follows uses these two terms. If your CPA or another lender uses different language for the same structures, the framework here still applies.

For answers to foundational questions about how equipment financing works, our equipment financing FAQs covers the basics.

What Is a Dollar-Out Capital Lease?

A dollar-out capital lease is a financing structure built around full ownership. The lessee makes fixed payments over the lease term and acquires the equipment for a nominal $1 payment at the end. Because ownership transfers at the end, the IRS treats this structure as a financed purchase rather than a true rental. For tax purposes, the lessee is treated as the owner of the equipment from the outset.

For a CFO, that distinction has four practical consequences.

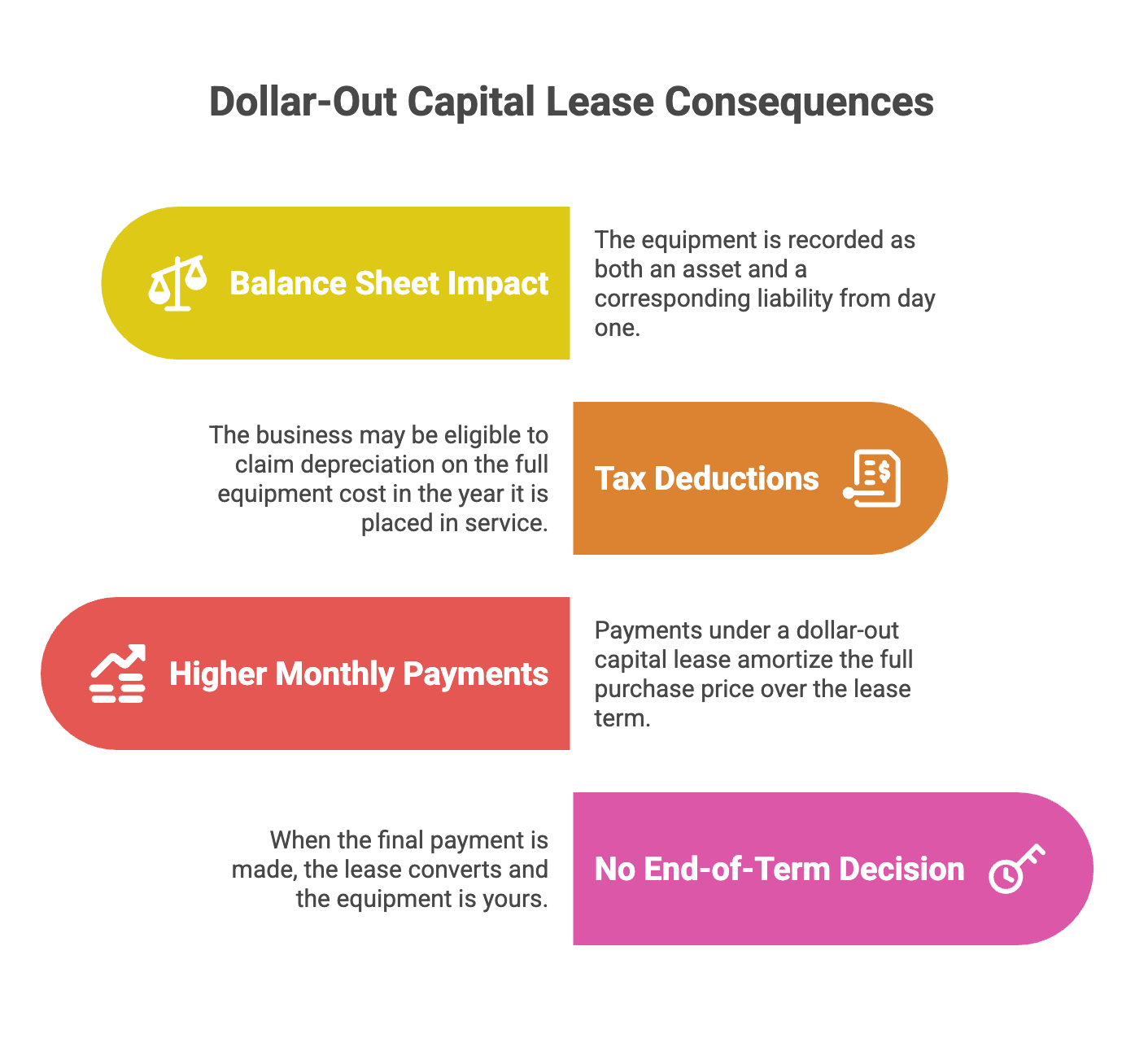

- The asset goes on your balance sheet

The equipment is recorded as both an asset and a corresponding liability from day one, similar to a loan. This affects your debt ratios and may implicate existing bank covenants depending on your credit facility terms. - You may qualify for significant first-year tax deductions

Because the IRS treats you as the owner, the business may be eligible to claim depreciation on the full equipment cost in the year it is placed in service. That includes potential Section 179 expense and bonus depreciation, subject to IRS limits and your specific tax situation. Your CPA determines eligibility. - Monthly payments are higher

Payments under a dollar-out capital lease amortize the full purchase price over the lease term. That is why they run higher than the equivalent FMV operating lease payment on the same asset. - There is no end-of-term decision

When the final payment is made, the lease converts and the equipment is yours. Traci Dolphin, President, Equipment Leases, Inc., describes it directly: “We never collect the dollar and then it just converts and they’re finished.”

What Is an FMV Operating Lease?

An FMV operating lease is a financing structure built around flexibility and lower monthly cost. The lessee makes payments over the lease term and, at the end, chooses to purchase the equipment at its then-current fair market value, renew the lease, or return the equipment.

Because ownership does not automatically transfer, the IRS treats this as a true rental. The lessor retains tax ownership and claims depreciation.

That structure shapes the economics in four ways.

- Monthly payments are lower

Payments reflect the equipment’s expected depreciation over the lease term, not its full purchase price. The lessor recovers the remaining residual value at term end, which keeps the lessee’s payments lower throughout. - Lease payments are typically deductible as operating expenses

The lessee deducts payments as ordinary business expenses, producing a predictable, recurring deduction spread across the lease term. - Section 179 and bonus depreciation are generally not available

Because the lessee does not hold tax ownership, the large first-year deductions accessible through a dollar-out capital lease do not typically apply here. We cover this distinction in depth in the tax section below. - End-of-term flexibility is a built-in feature, not an afterthought

When the lease concludes, the lessee can buy the equipment at fair market value, renew under new terms, or walk away.

As Traci Dolphin explains, some clients choose this structure to keep payments lower while new equipment ramps up revenue, with a clear decision point at the end rather than an automatic ownership commitment.

Dollar-Out vs. FMV Operating Lease: Side-by-Side

Use this as your quick reference across the dimensions that matter most. Keep your specific situation in mind as you read it. The column that makes sense on paper can shift once your CPA weighs in on your tax position or your bank flags where your covenant headroom actually sits.

| Feature | Dollar-Out Capital Lease | FMV Operating Lease |

|---|---|---|

| Ownership at Term End | Automatic for $1; no decision required | Your choice: buy at fair market value, renew, or return |

| Monthly Payments | Higher; amortizes the full equipment cost | Lower; reflects depreciation over the lease term only |

| Tax Treatment | Treated as a financed purchase; depreciation, Section 179, and bonus depreciation may apply (consult your CPA) | Payments typically deductible as operating expenses; Section 179 generally not available (consult your CPA) |

| Balance Sheet | Asset and liability recorded from day one | Depends on your applicable accounting framework |

| End of Term | Nothing to decide; ownership converts automatically | Walk away, buy, or extend |

| Works Best When | Ownership is the goal, the balance sheet has room, and your CPA confirms first-year deduction eligibility | Payments need to stay lean, covenants are a factor, or you want options when the term ends |

Two CFOs can look at this table and land in completely different places.

One is acquiring a manufacturing equipment financing line that will anchor production for the next decade. Ownership matters. The balance sheet has room. The CPA has flagged a significant tax liability this year that Section 179 could offset. That CFO needs to have the dollar-out capital lease conversation.

The other is financing diagnostic equipment for a medical equipment leasing practice that refreshes technology every four years. Lower payments preserve cash while the equipment generates revenue. The bank relationship has covenant constraints. Walking away at term end is a feature. That CFO’s answer is the FMV operating lease.

Same table. Different answers.

Always consult a qualified CPA or tax advisor before making equipment financing or tax planning decisions.

How Lease Structure Affects Your Tax Position

Before we go further, let’s correct a misconception that comes up often: not all lease payments are deductible in the same way. The type of lease you sign determines the type of deduction available to you. That distinction has real consequences for your tax planning, and it is worth getting clear on before you finalize anything.

Dollar-Out Capital Lease: Own the Equipment, Own the Deduction

Because this structure is treated as a financed purchase, two deduction provisions open up:

- Section 179: Deduct the full cost of qualifying equipment in the year it is placed in service, up to IRS annual limits

- Bonus depreciation: Take a significant additional first-year deduction on qualifying assets

Both are subject to eligibility requirements and your specific tax situation. Your CPA determines what applies and how much.

What we can tell you is this: the window for bonus depreciation is currently wide open. The provision has been restored to 100%, and it did not happen by accident. Buddy Zarbock, Founder & CEO, Commercial Funding Partners, sits on the ELFA Political Action Committee and has met with members of Congress annually to advocate for exactly this kind of tax policy.

In his own words: “Our political action work in Washington, D.C., helped advocate for business-friendly policies like the continuation of bonus depreciation. I’m proud to have been part of that effort.”

That is not background information. That is a lender who understands the tax environment around your financing decision at the policy level, not just the product level.

FMV Operating Lease: Payments Are the Deduction

The mechanics are different here, and that is not a disadvantage. It is a different tool for a different situation.

Because the lessor retains tax ownership:

- You do not claim depreciation on the asset

- Lease payments are typically deductible as ordinary business expenses

- Lease payments are typically deductible as ordinary business expenses Deductions are spread predictably across the lease term

- Section 179 and bonus depreciation are generally off the table

For businesses whose tax position makes a consistent, recurring deduction more valuable than a large first-year write-off, this structure often delivers the better outcome. For a deeper look at how lease structure interacts with your broader tax strategy, see our guide to the tax benefits of equipment financing for CFOs.

Your Accounting and Your Taxes Are Not the Same Conversation

How a lease appears on your financial statements under ASC 842 and how the IRS taxes it are governed by entirely different rules. The same transaction can be classified one way for reporting purposes and another way at tax time.

Your CPA owns that analysis. Our job is to make sure the structure you choose does not close off tax options before that conversation takes place.

The Right Answer Depends on Your Situation Right Now

There is no universally superior structure from a tax standpoint. The right choice comes down to your taxable income this year, your existing depreciation schedule, and your forward-looking tax strategy. That is a conversation for you and your CPA. We structure around whatever they recommend.

How Lease Structure Affects Your Balance Sheet and Bank Covenants

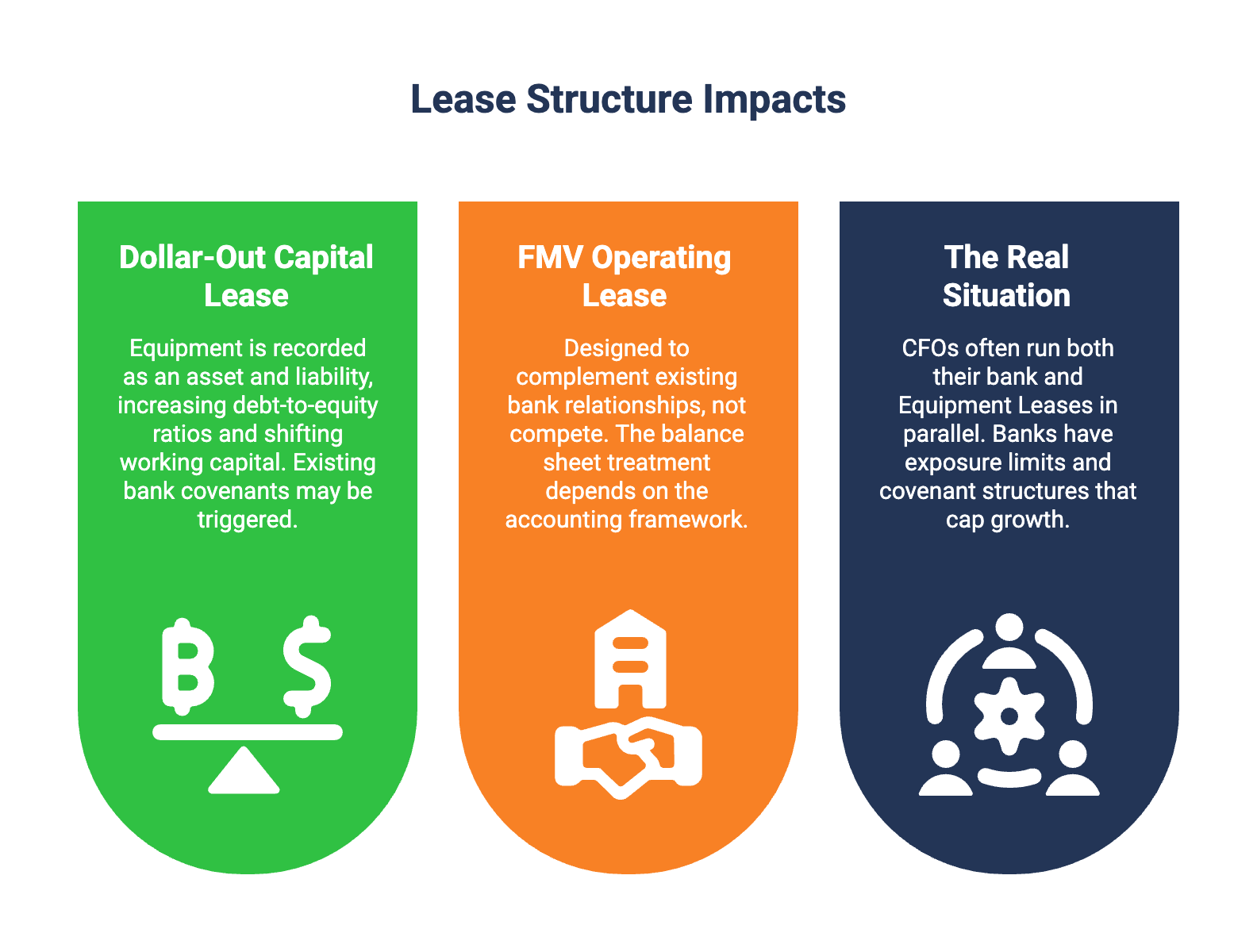

For CFOs managing an active primary bank relationship, the balance sheet impact of your lease structure is not a footnote. It is often the deciding factor.

Dollar-Out Capital Lease: It Goes on the Books

From day one, the equipment is recorded as both an asset and a corresponding liability. The downstream effects:

- Debt-to-equity ratios increase

- Working capital calculations shift

- Existing bank covenants may be triggered depending on your credit facility terms

If your balance sheet has room and your priorities are ownership and depreciation, this is typically manageable. The liability is real, but so is the asset backing it. For companies already operating close to their covenant thresholds, a new liability on top of an existing credit facility is a conversation your bank needs to have before structure is finalized. Not after.

FMV Operating Lease: Designed to Work Alongside Your Bank

The balance sheet treatment of an FMV operating lease depends on your applicable accounting framework.

What is not in dispute is the strategic intent behind this structure. The FMV operating lease is explicitly designed to complement your existing bank relationship, not compete with it. Buddy Zarbock describes how this plays out: “We do operating leases and tax structures allowing clients to take advantage of the current tax laws, and we help them expand upon what their bank can offer.”

Equipment Leases is not a bank replacement. We work alongside your bank, stepping in where its capacity ends. For businesses looking to unlock equity from existing assets as part of their broader capital strategy, an equipment sale-leaseback may also be worth exploring alongside these lease structures.

The Real Situation Most CFOs Are In

Many of the CFOs we work with are not choosing between their bank and Equipment Leases. They are running both in parallel.

Their bank handles deposits, operating lines, and conventional credit. It is a valued relationship. But banks have exposure limits. They have covenant structures that cap growth regardless of how well the company is performing. And they often cannot move at the speed an equipment acquisition requires.

The number one problem EQL solves is restrictive bank covenants. The number two problem is bank exposure limits that cap growth regardless of profitability. The FMV operating lease is designed to address both, without touching the bank relationship you have spent years building.

What Happens at the End of the Lease?

One of the most common questions we hear from CFOs before they sign: what am I actually committing to at the end of this? The answer depends entirely on which structure you choose.

Dollar-Out Capital Lease: Nothing Left to Decide

When the final payment is made, the lease converts. We release the UCC lien and the equipment belongs to your company outright. No residual calculation. No negotiation. No buyout decision.

That simplicity reflects something intentional. We are not in the business of recovering and remarketing used equipment. Client ownership is the goal of nearly every transaction we structure.

FMV Operating Lease: The Decision Stays Yours

At term end, you choose your path based on where your business stands at that moment, not where you thought it would be when you signed. That is what makes this structure particularly well-suited for industries where technology moves fast.

Medical imaging systems become obsolete. Automation platforms get replaced by newer generations. Energy infrastructure evolves. For CFOs in those environments, the ability to buy, renew, or walk away at term end, with full information and no obligation, is not a minor feature. It is the reason they chose this structure in the first place.

Which Structure Fits Your Business?

There is no universal answer. The right structure aligns with your tax position, your balance sheet capacity, and your cash flow priorities. It also depends on what you want to happen when the lease ends.

Here is a practical framework for working through it.

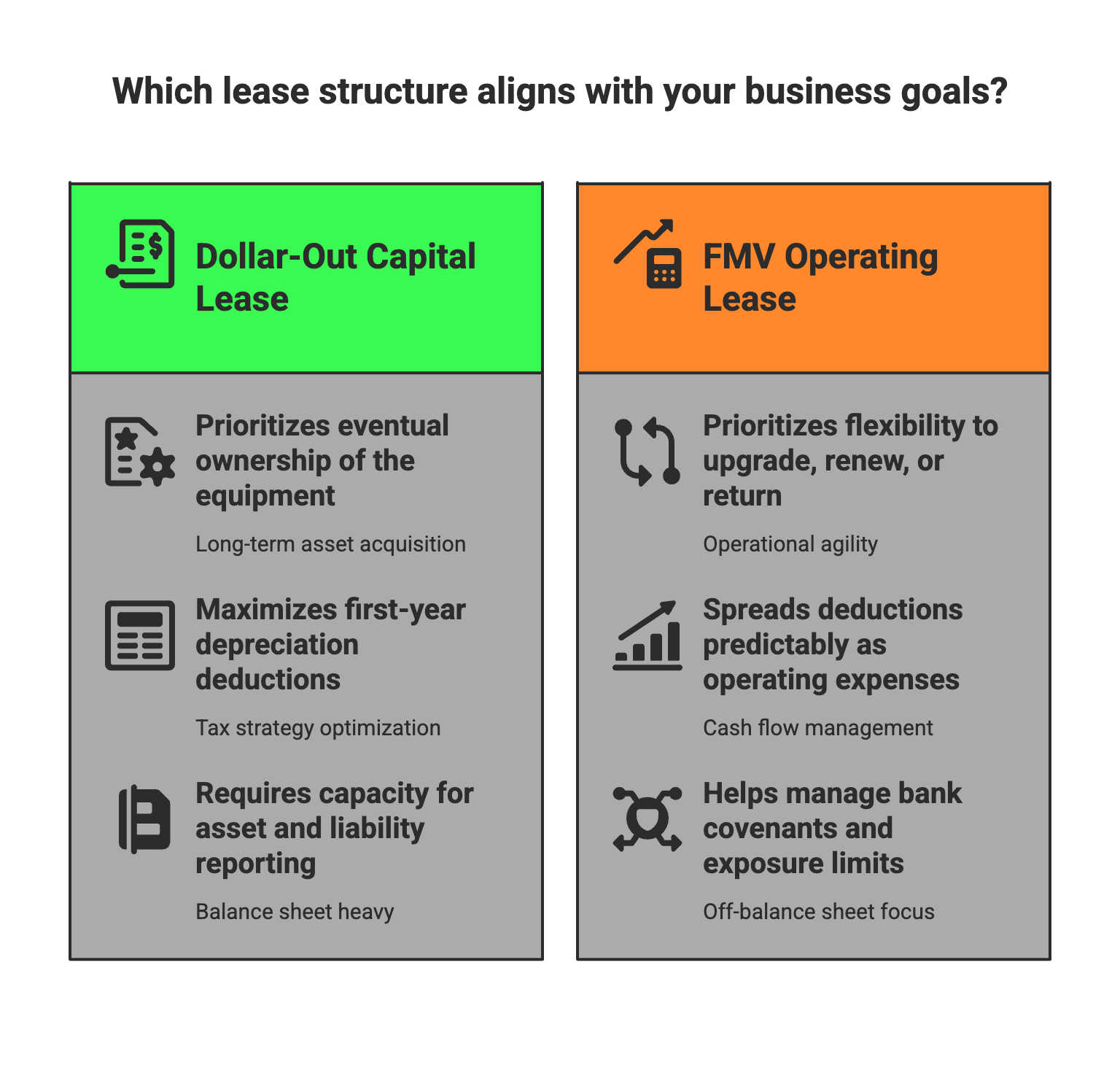

Choose a Dollar-Out Capital Lease If:

- Eventual ownership of the equipment is the primary goal

- Your CPA has confirmed eligibility for first-year depreciation deductions and you want to maximize them

- Your balance sheet can accommodate the asset and corresponding liability

- The equipment is long-lived and central to how your business operates

Choose an FMV Operating Lease If:

- You are managing bank covenants or approaching exposure limits with your primary lender

- Lower monthly payments matter while the equipment ramps up revenue

- You want deductions spread predictably across the lease term as operating expenses

- You value the ability to upgrade, renew, or return at term end

Before You Decide Either Way

Bring your CPA into the conversation before structure is finalized. Bring your bank relationship into view as well. The variables that determine the right answer sit at the intersection of tax strategy, balance sheet capacity, and covenant position. None of those live in isolation.

Our credit team has structured transactions from $250,000 to $100 million-plus across industries nationwide, from manufacturing and medical to energy and construction.

Traci Dolphin, who brings 34 years of credit and finance experience to every transaction, leads that process. We work alongside your advisors, not around them. The goal is to identify the right structure for your situation and execute it cleanly, from credit decision through funding.

When you are ready to start that conversation, we are the first call.

Equipment Financing Programs & Leaseback Solutions

How Equipment Leases Structures the Conversation

Many lenders start with a product and work backward to fit the client. We start with the client’s situation. Structure follows from there.

Buddy Zarbock, Founder & CEO, Commercial Funding Partners, describes the philosophy plainly: “We use the tax and accounting rules of the day to allow our clients to use those to the best of their ability.”

That orientation shapes how client relationships develop. Many clients begin with a single schedule and return for additional financing as their business grows, with each successive schedule structured on stronger terms than the last. Clients have completed 20 or more schedules with us.

Not a transaction. A financing partnership that improves as you grow.

Ready to Structure the Right Lease?

If you are evaluating an equipment acquisition and want to understand which structure best serves your tax position, balance sheet, and long-term capital strategy, the conversation starts with your goals, not a product form.

Bring your CPA. We handle the rest.

Get a custom lease quote or learn more about Equipment Leases, Inc. before you reach out.