Most bankers suppress the referral instinct. That is the wrong move.

When a client’s equipment needs sit outside what the bank can comfortably structure, the right introduction is not a concession. It is relationship management executed well. A client whose project gets funded stays a client. One who gets a slow “no” or a partial approval starts looking for someone who can say “yes.”

Bank referral equipment leasing is not a fallback for problem credits. It is a tool that relationship-focused bankers use to protect the clients they have worked hard to keep.

Here is how it works, what it protects for you, and what it takes to make the introduction.

Exposure Limits Are Structural. The Referral Is the Solution.

Every bank has a limit on the amount of credit it can extend to a single borrower. That is not a policy gap or a failure of judgment. It is a regulatory and risk management reality that every commercial lender operates within.

The problem is that your best clients keep growing. A manufacturer doing $40 million a year, creditworthy, expanding capacity, buying a new production line, that is exactly the kind of client you want to keep. They may still hit your exposure cap. When they do, the bank’s options narrow fast. A partial approval stalls their project. A decline strains a relationship you have spent years building.

We step in to finance the equipment without touching your existing credit position. Your client gets funded. Your relationship stays intact. The exposure problem is resolved, not ignored.

This is the structure that works: bank-complementary, not competitive.

Your Lien Position Stays Exactly Where It Is

Most bankers want this question answered before anything else: what happens to their security position when they refer a client to us?

Nothing changes.

We File on the Equipment. Nothing Else

We file a UCC-1 on the specific equipment we are financing, and only that equipment. Your existing liens on receivables, inventory, real property, and any other business assets stay exactly where they are. No blanket lien. No cross-collateralization. No covenant complications.

When the Lease Ends, We Step Back

When the client reaches end of term and takes ownership of the equipment, we release the UCC filing. Your position throughout that entire period is untouched.

We Fill the CAPEX Gap. You Keep What You Have.

Banks typically finance equipment at a percentage of cost. That leaves a funding gap the client has to cover out of pocket or piece together from other sources. We finance 100% of the project, including the costs most banks do not touch. The client’s full equipment needs get funded. Your lien position on everything else stays exactly as it was.

You keep what you have. We fill what you cannot.

Structures Banks Often Can’t Offer — Available Through Referral

Most banks are built for straightforward equipment loans. That works for many transactions. It does not work for all of them.

When a client needs a structure that fits their accounting preferences, balance sheet position, or tax strategy, a referral to us opens options your product set cannot. You are not just solving a credit gap. You are giving your client access to tools the bank was never set up to provide.

Three Structures. Each is Built for a Different Business Need.

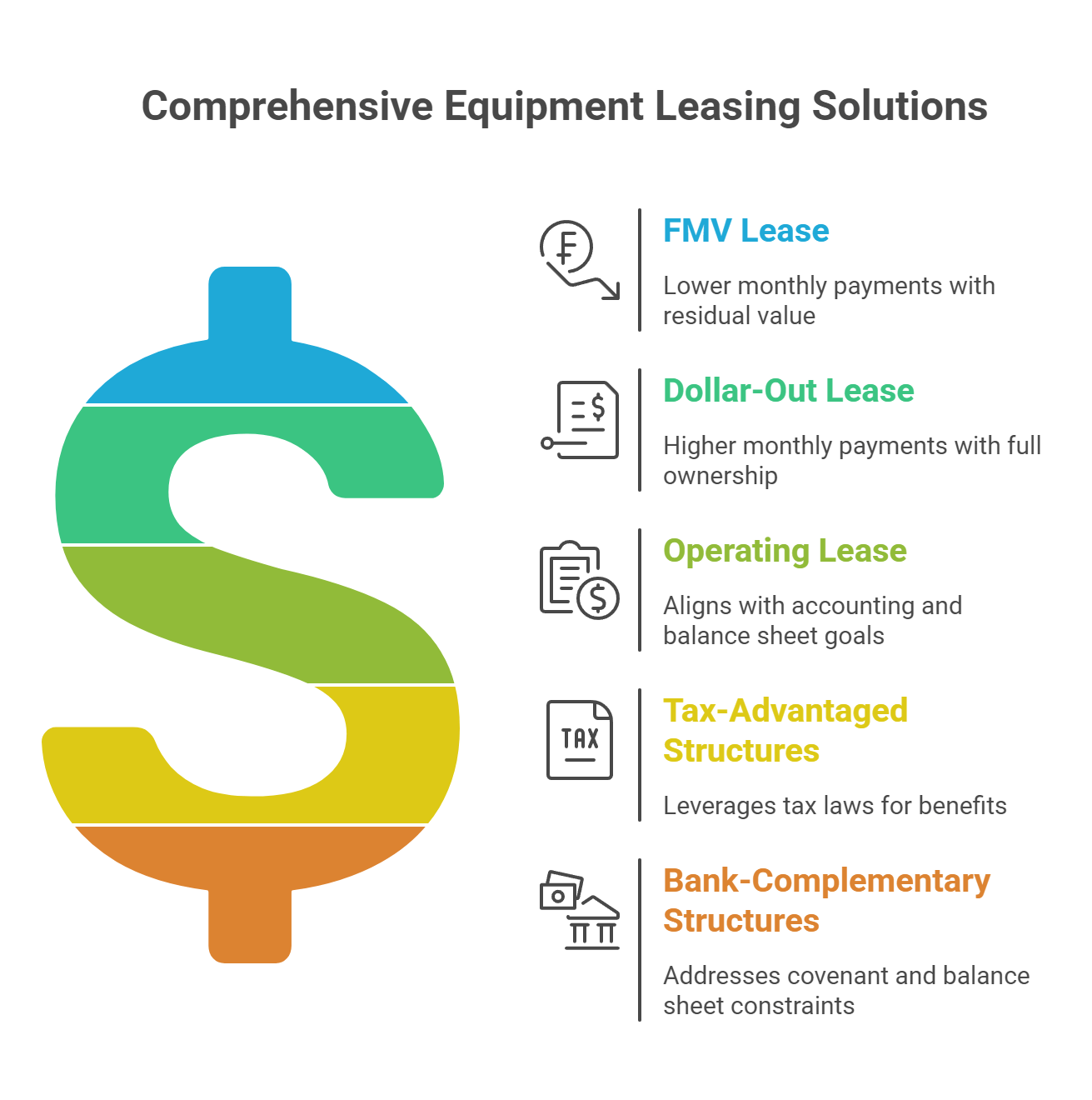

FMV lease

Lower monthly payments throughout the term, with a residual at the end of the term based on the equipment’s fair market value. A good fit for clients who want to preserve cash flow and keep their options open.

Dollar-out lease

Higher monthly payments, with full ownership transfer at the end for a nominal amount. Built for clients who want to own the equipment outright when the lease concludes.

Operating lease

Structured to align with a client’s accounting and balance sheet goals. Often, the right fit for businesses is managing leverage ratios or approaching a line of credit renewal.

Tax-Advantaged Structures Are Also Available

We structure tax leases that enable clients to take advantage of current tax law, including bonus depreciation. The right structure depends on the client’s situation. We always direct them to their CPA or tax advisor to confirm what works for their business.

More Than a Credit Solution

A referral to Equipment Leases gives your client bank-complementary structures that address covenant constraints and balance sheet goals your loan products were not designed to solve. That is a capability you can extend through us, without building it yourself.

The Banker Gets Credit for the Speed

One of the most compelling reasons banks refer clients to equipment leasing is speed. Not just because fast funding helps the client. Because the banker who made the introduction gets credit for the outcome.

Your client remembers who kept their project moving.

Our Credit Committee Is Built for Fast Decisions

Our finance committee has three or four senior members, depending on the transaction’s level. That structure is intentional. Fewer decision-makers means faster decisions, and faster decisions mean your client is not waiting weeks for a credit committee that meets once a month.

When a borrower is prepared and the deal is clean, we can move the same day.

What the Timeline Looks Like

- Contact within 15 minutes of a submitted inquiry

- LOI within 24 to 48 hours for standard transactions

- 10 days to two weeks for most deals from start to funded

- Two to three weeks for complex multi-million dollar projects

- Funds wired within 24 hours of final documentation

Six Months Faster Than an SBA Loan

If your client is weighing an SBA loan, we are typically six months faster. Any difference in rate is more than recovered in the first month through time saved and avoided opportunity costs. That is not a minor distinction for a business waiting on a production line or a critical piece of equipment.

The Introduction Reflects Well on You

When you refer a client to Equipment Leases and their project moves from inquiry to funded in two weeks, they do not forget who made the call. Speed is a reputational asset for the banker, not just a capability of ours.

The Equipment Your Bank Wasn’t Built to Underwrite

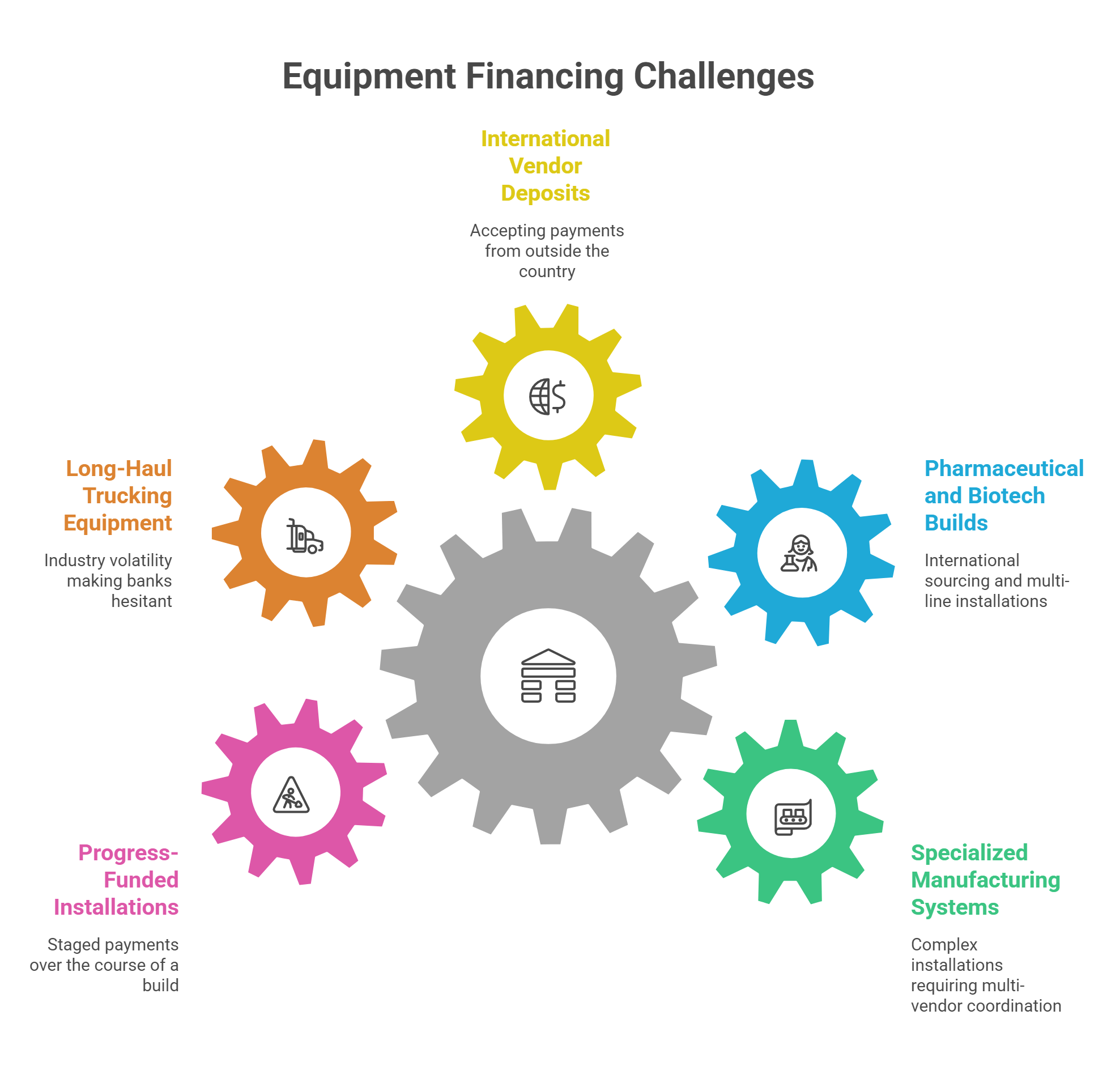

Not every referral comes down to exposure limits. Sometimes the issue is the equipment itself.

Banks operate within underwriting frameworks built for standard transactions. Certain equipment categories fall outside those frameworks. Not because the client is a problem. Because the bank’s credit guidelines were never designed to evaluate them. Knowing when to refer is part of what makes a relationship banker valuable to their clients.

Categories That Come to Us from Banks Regularly

- Specialized manufacturing systems with multi-vendor coordination, long installation cycles, and milestone-based disbursements

- Pharmaceutical and biotech builds involving complex, multi-line installations sourced from manufacturers in Germany, Switzerland, and other international markets

- International vendor deposits, including payments in euros. Most banks do not accept deposits from outside the country. We do.

- Long-haul trucking equipment, where industry volatility puts most banks on the sidelines

- Progress-funded installations where the client needs deposits and staged vendor payments made directly to suppliers over the course of a build

These are transactions where the client is creditworthy and the project makes sense. The bank’s framework just was not built for them. That is where we come in.

100% Project Financing — Including What Banks Typically Leave Unfunded

Most banks finance equipment at a percentage of the cost. Ten to twenty percent down is standard. Soft costs, including installation, shipping, software, and warranties, often fall outside the loan entirely.

That gap lands on the client. For a business, managing cash flow carefully can be the difference between a project moving forward and one stalling.

We Cover the Full Scope

When we fund a deal, we cover:

- Equipment purchase price

- Installation and commissioning

- Shipping and delivery

- Software and integration

- Warranties and service agreements

- Vendor deposits and milestone payments are made directly to suppliers throughout the build

The client does not come out of pocket for any of it.

Progress Funding for Long-Cycle Builds

When equipment has to be built before it ships, we manage the deposit and milestone payment schedule directly with the vendor. A client should not have to put a $2 million deposit out of pocket while a six-month build is still in progress. We handle those payments as the project advances.

Equipment leasing for bank clients through Equipment Leases means your client receives full project funding. Not 80% of it. The referral closes the gap entirely; nothing is left for the client to piece together on their own.

For more details on how these structures work in practice, see our equipment financing FAQs.

The Referral Protects the Relationship at Every Step

The concern most bankers carry into a referral decision is not about the structure. It is about the client. What happens to the relationship once Equipment Leases is involved?

We answer this directly.

We Do Not Compete for What You Have

We are not looking to become the client’s primary lender, deposit institution, or line-of-credit provider. We do not pitch competing banking products to referred clients. The equipment transaction is the scope of our involvement. Nothing more.

You Stay Informed on Your Terms

Some referring bankers want updates throughout underwriting. Others want a single confirmation upon deal closure. We follow your lead. We do not generate unnecessary contact points or make moves that undermine your standing with the client.

Confidentiality from the First Conversation

We treat every referral with discretion. NDAs available from the first conversation.

A Track Record Worth Referring To

A banker’s reputation is only as good as the partners they recommend. Before you make an introduction, here is what stands behind one to Equipment Leases.

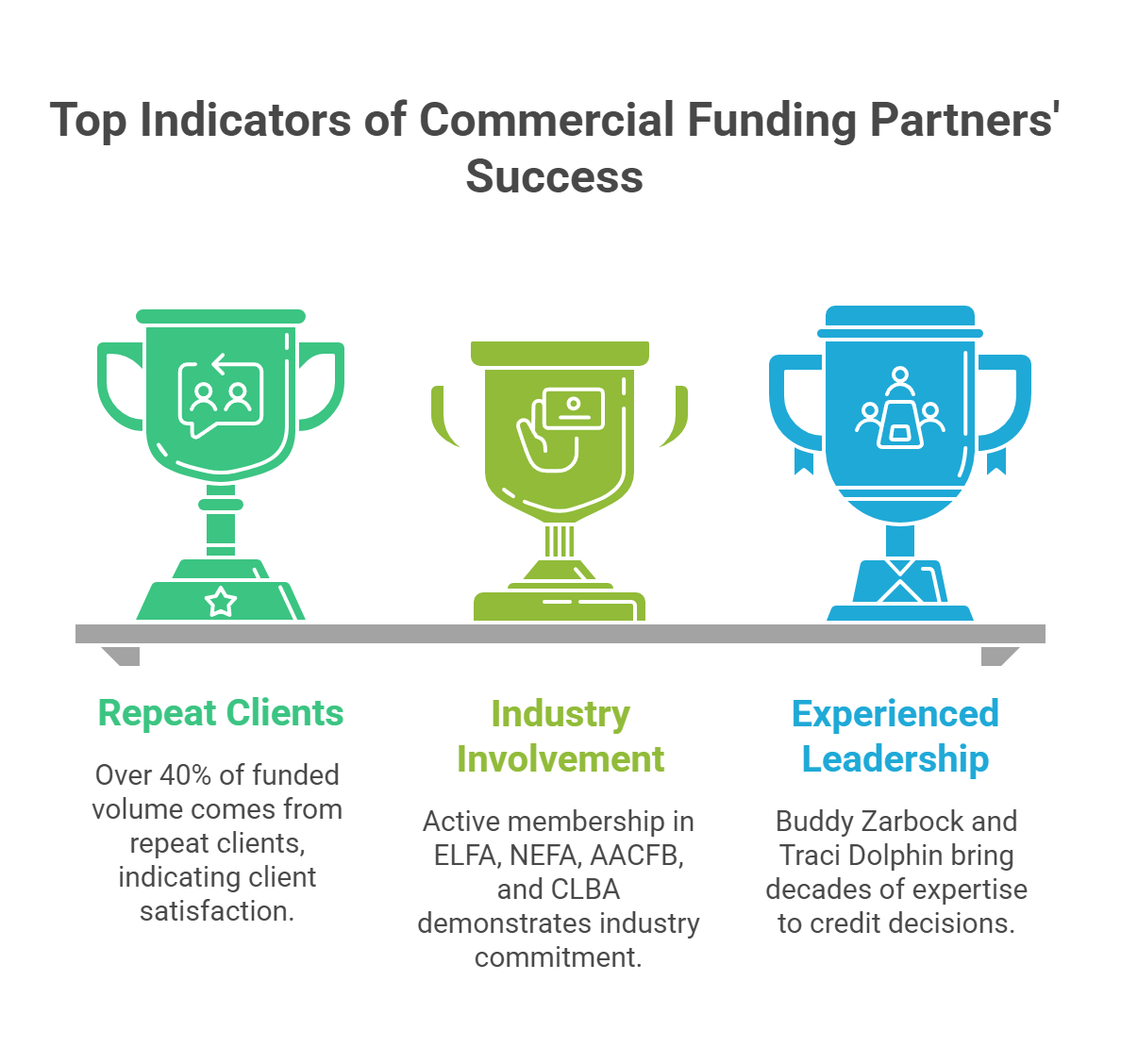

Commercial Funding Partners, the direct lender behind Equipment Leases, was founded in 2012. We are active members of ELFA, NEFA, AACFB, and CLBA. BBB accredited.

More than 40% of our funded volume comes from repeat clients. Clients come back because the experience delivered. That is the most useful indicator we can offer a banker considering whether to make an introduction.

- Buddy Zarbock founded Commercial Funding Partners in 2012 and has spent more than 20 years in commercial finance. He is the recipient of the AACFB President’s Award, served four years as chair of the AACFB Education Committee, and is active on ELFA’s Independent Lessor Steering Committee and Political Action Committee.

- Traci Dolphin leads all credit decisions as Chief Credit Officer. She brings 34 years of credit and finance experience to every deal, has been recognized as one of the Top Women in Leasing, and oversees a credit committee that has funded transactions from $250K to $100M+.

A Florida manufacturer received $9M in equipment financing to upgrade their full operation and win new production contracts. A masonry firm unlocked $8M through a sale-leaseback to fund the acquisition of a competitor. These are the outcomes referred clients come back from.

When a banker refers a client to Equipment Leases, they are making an introduction to a firm with a documented record of funding deals responsibly and returning clients in better shape than they arrived.

How to Make the Introduction — Five Minutes, 15-Minute Response

Making the first introduction does not require a complex referral agreement. It takes five minutes.

Complete the Lender Referral Quote Request Form

Submit the client’s name, a brief description of their equipment need, and the funding requirement through our Lender Referral Quote Request Form. That is all we need to get started.

What Happens Next

- We contact the borrower within 15 minutes of submission

- The client completes a seven-minute online application

- We handle underwriting, documentation, vendor coordination, and funding from that point forward

- You stay informed at whatever level you prefer

We take it from there. You do not need to manage the process or stay in the middle of it.