Most content on private equity equipment financing reads like a benefits list. Capital preservation. Balance sheet flexibility. Scalability. These are real outcomes, but they describe what equipment financing does, not how it works within a PE capital structure.

At close, the model leaves a gap in the credit structure. Equipment financing fills it without touching equity. The liens sit outside the core collateral pool, leaving covenants intact. Sponsors use it at entry, during growth, and again at exit.

We work with private equity sponsors, deal teams, and portfolio company finance leaders on equipment financing that sits alongside existing senior credit facilities without conflict, amendment, or cap table interaction. The structural case for that approach follows.

The Credit Facility Was Not Designed to Fund the Equipment

When a PE sponsor closes a platform acquisition or add-on, the senior credit facility has a specific job:

- Working capital, maintaining liquidity through integration and transition

- Integration costs, such as systems, headcount, and operational consolidation

- Future deal capacity, preserving dry powder for add-ons and follow-on investments

That is what the underwriting model was built around, and that is what the facility is sized to protect.

The CAPEX required to actually operate the portfolio company, such as production line upgrades, automation systems, facility equipment, and specialized machinery, was rarely part of that conversation. It is not an oversight. It is how the transaction was structured.

The consequence is predictable. Post-close, the portfolio company has a funded credit facility and an unfunded equipment need. Using that liquidity for capital expenditures:

- Compresses working capital

- Works against what the facility was designed to preserve

- Can create an exposure limit pressure that constrains financial flexibility going forward

Equipment financing addresses a gap that was built into the structure from the start. It funds what the credit facility was not designed to fund, operates independently of the senior facility, and does not require an amendment to the credit facility or the senior lender’s involvement.

The two structures do not compete. They serve different purposes, and they are designed to stay that way.

Equipment Financing Sits Entirely Outside the Equity Structure

This is the question PE sponsors ask first, even if they do not ask it directly.

Will this create a problem with the cap table?

It will not.

EQL’s security interest attaches only to the financed equipment. Receivables, real property, inventory, and all other business assets are untouched. There are no warrants. No equity kickers. No interaction with preferred stock terms, governance agreements, or liquidation preferences.

Equipment financing from EQL is an asset-backed obligation at the portfolio company level. It is evaluated on the equipment being financed and the portfolio company’s ability to service the obligation. It does not ripple up to the fund. It does not interact with the capital structure the sponsor has engineered.

That distinction matters for non-dilutive CAPEX in a private equity context. Sponsors can finance significant equipment needs without triggering an equity event, complicating a future recapitalization, or creating any downstream effect on fund-level economics.

The structure is contained. The lien is specific. The cap table stays exactly as it was.

No Blanket Lien. No Covenant Trigger. No Lender Conflict.

Most financial covenants are written around a company’s broader asset base and debt obligations. A blanket lien from a new lender changes that picture. Ours does not.

Because our collateral is limited to the specific equipment being financed, we sit outside the scope of most existing covenant structures. We are not adding a claim on assets that the senior lender has already accounted for. We are not increasing leverage in a way that affects coverage ratios tied to enterprise-level debt. The portfolio company’s covenant compliance position does not change when we come in.

There is no lender conflict to manage. No conversation to have with the senior lender. No amendment process to run in parallel with the equipment deal.

Sponsors bring us in, we handle the CAPEX, and the existing lending relationship continues without interruption. That is a bank-complementary structure working exactly as it should.

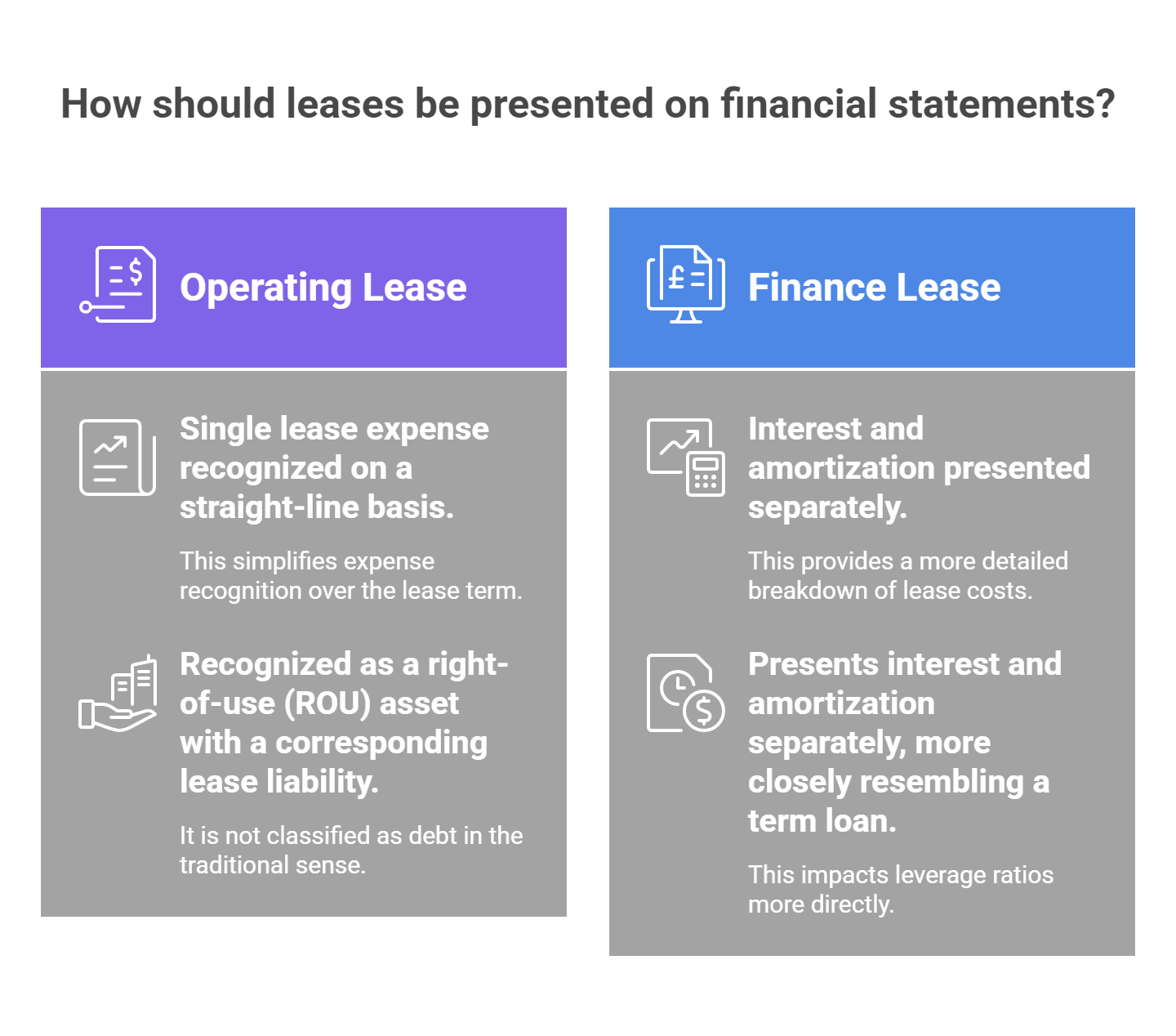

How Operating Leases Appear on the Balance Sheet

For sponsors managing leverage ratios ahead of a recapitalization or exit, the lease structure is not just an equipment question. It is a financial reporting question.

Under current accounting standards, an operating lease is recognized on the balance sheet as a right-of-use (ROU) asset with a corresponding lease liability. It is not classified as debt in the traditional sense. The income statement reflects a single lease expense recognized on a straight-line basis over the term. A finance lease, by contrast, presents interest and amortization separately, more closely resembling a term loan in its financial statement impact.

For sponsors who are actively managing reported leverage, that distinction in presentation matters. The structure of the lease affects how the obligation is presented across financial statements, which, in turn, affects how leverage is interpreted by future lenders, buyers, or investors evaluating the portfolio company.

We structure both operating and capital leases. During the structuring conversation, we work directly with the portfolio company’s finance team to understand their accounting preferences and investor reporting requirements, and we align the lease type accordingly.

This section provides structural context only and is not accounting or tax advice. How a specific lease is classified and reported depends on the facts of each transaction and the applicable accounting guidance. Sponsors should consult their CFO, auditor, or accounting advisors for guidance specific to their situation. That is our standard practice, and we will say the same thing directly if the question comes up in our conversation.

Speed is a Structural Advantage in the Post-Close Window

Our credit committee has three to four senior members. Decisions are made by people with direct authority, not routed through layers of institutional review.

When a deal comes in with a complete financial package, here is how our timeline works:

- Initial indication, mid-market transaction: 24 to 48 hours

- Full underwriting, complex or multi-vendor builds: 10 days to two weeks

- Larger transactions ($50M to $60M range): Three to four weeks

Those are not aspirational timelines. They reflect how our process is structured and what we communicate at the start of every engagement.

If a deal has a hard deadline, such as an acquisition close, a vendor delivery window, a production ramp commitment, we give a direct answer on timing in the first conversation. Not at the end of the process. Sponsors working against a fixed schedule need to know whether we can meet it before committing time on both sides, and we respect that.

Progress Funding for Staged Builds and Multi-Vendor Projects

Most post-close equipment needs are not simple purchase orders. They are staged builds with multi-vendor installations, automation rollouts, and facility-wide infrastructure upgrades, where deposits and milestone invoices arrive over months before a single asset is operational.

We manage those payments directly. Our progress funding structure covers:

- Vendor deposits are paid at the outset of the project, before equipment is built or shipped

- Milestone invoices are disbursed as each project phase is completed, aligned to the actual build progress

- International vendor payments, including deposits in euros for equipment sourced from European suppliers, which most banks will not handle

Disbursements follow the project, not a single funding event.

For sponsor-backed companies running complex, multi-phase capital builds, that structure keeps cash reserves intact, vendor relationships on schedule, and the finance team out of the business of manually tracking deposits across multiple vendors and currencies.

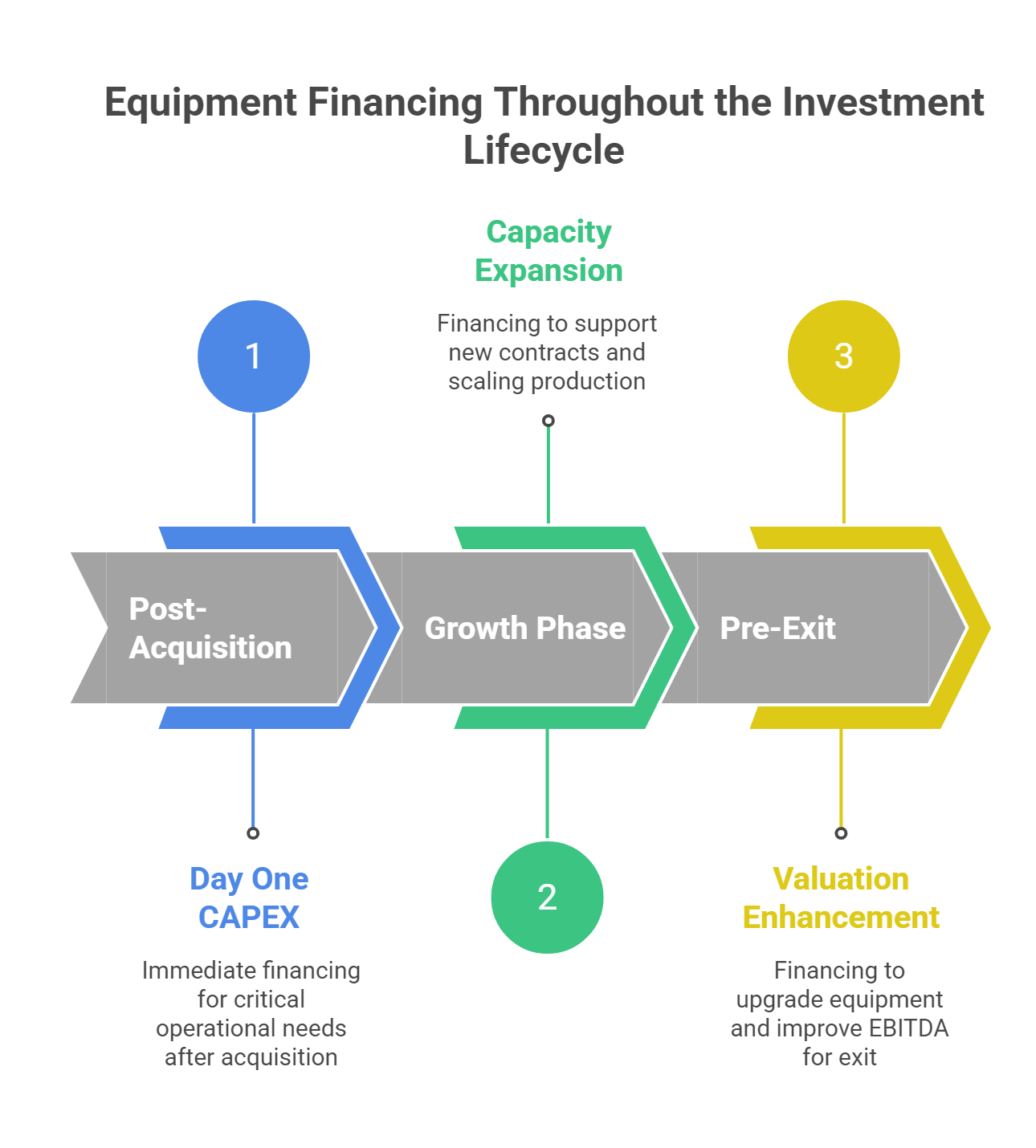

Equipment Financing at Every Stage of the Investment Lifecycle

Most equipment financing conversations start with a specific need, a piece of equipment, a production line, or a facility upgrade. For sponsors managing a portfolio company through a full ownership cycle, the need rarely stops there.

The CAPEX requirement follows the company through every stage of the investment. We structure accordingly.

Post-Acquisition

Day One is the highest-pressure moment for equipment financing. The credit structure has just closed, the operational CAPEX need is immediate, and the portfolio company has no runway to wait on a bank committee or facility amendment.

This is where we are built to move. With a complete financial package and a clear project scope, we engage quickly and give a direct answer on timing from the first conversation.

Growth Phase

Winning new contracts and expanding capacity creates its own financing pressure. Sponsors need to deploy capital fast without triggering an equity event or revisiting a credit structure that is already working.

Equipment financing scales with the portfolio company’s growth. Each financing schedule builds on the last, and terms improve as the relationship and the company’s financial profile develop. We want to be the first call, not just for the post-close CAPEX, but for every capacity expansion that follows.

Pre-Exit

In the 12 to 24 months before a planned exit, operational efficiency becomes part of the valuation story. Modern, well-maintained equipment supports stronger EBITDA margins, cleaner operations, and a more compelling presentation to buyers.

We structure financing at this stage with the exit timeline in mind, not a one-size-fits-all term sheet, but a structure calibrated to where the company is in its ownership cycle.

Sale-Leaseback: Converting Existing Equipment Into Working Capital

Not every capital needs new equipment. Sometimes, the capital a sponsor needs is already sitting in the portfolio company’s yard.

When a portfolio company owns productive equipment outright, that equity is illiquid. The assets are generating operational value but no financial value. A sale-leaseback changes that. We purchase the equipment and lease it back to the company, converting embedded equity into immediate working capital while the company retains full use of every asset. Not a single production shift is disrupted.

That capital can be directed toward whatever the sponsor needs it for:

- An add-on acquisition that the current credit structure cannot absorb

- Debt paydown ahead of a recapitalization

- A strategic initiative that requires liquidity, the business cannot otherwise generate quickly

For sponsors managing portfolio companies approaching bank exposure limits or looking to optimize capital structure ahead of a transaction, a sale-leaseback is often the most direct path to liquidity from assets already in place.

In one recent engagement, a middle-market PE firm needed to fund $7.5M in production equipment across three facilities following a platform acquisition. We structured asset-specific leasing solutions that isolated equipment financing from senior debt, preserved equity for future add-ons, and matched payment schedules to production ramp-up timelines. Production capacity accelerated within 90 days of funding.

Sale-leaseback works in reverse, starting with what the portfolio company already owns. To learn more about how we structure these transactions, visit our Equipment Sale-Leaseback page.

Confidentiality Is a Baseline, Not a Courtesy

Discretion is not optional in PE transactions. It is a baseline operational expectation, and we treat it that way.

NDAs are available at the outset of any engagement. We work through the deal team or directly with the portfolio company’s finance leadership, whichever the sponsor prefers. Deal information does not move beyond the parties who need it. We do not generate unnecessary contact points or create paperwork trails that add complexity to the transaction.

Sponsors who work with us stay focused on running the business and executing the investment thesis. Equipment financing is handled quietly and professionally.

That is what we mean when we say clients can quietly enjoy their deal.

Work With a CAPEX Execution Partner Built for PE Transactions

Whether the need is immediate post-close CAPEX, a staged multi-vendor build, a sale-leaseback, or equipment financing ahead of a planned exit, we structure around the specific phase of the investment cycle.

Equipment-only collateral. Bank-complementary structure. Initial indications within 24 to 48 hours for mid-market transactions.

Two ways to start the conversation:

Active portfolio need: Submit the portfolio company, equipment required, and timeline for a candid assessment of fit, structure, and speed.

Standing partnership: If your portfolio has recurring CAPEX needs and you want a dedicated execution partner in place before the next deal closes, let’s discuss how we’ll work together.

For a full overview of how we work with PE sponsors and portfolio companies, visit our Private Equity Equipment Financing page.