Finance leaders understand depreciation, deductions, and basic tax planning. What’s often missed are the tax and cash-flow advantages tied to how equipment leases are structured, not from oversight, but from oversimplified assumptions about leasing.

At Equipment Leases, Inc., we see this consistently. Outcomes are rarely driven by rate alone. They depend on structure: how the lease is written, when equipment is placed in service, how ancillary costs are treated, and how the transaction aligns with underwriting and tax requirements.

This guide reflects how equipment leases are actually evaluated, funded, and documented by a direct lender working with CFOs, credit teams, and tax advisors. It explains where leasing creates real tax advantages, where common assumptions fail, and how proper structuring can improve cash flow, tax efficiency, and return on investment.

The objective is to provide finance leaders with a practical framework for evaluating equipment leasing decisions.

Why Equipment Leasing Impacts Taxes, Cash Flow, and Control

For experienced finance leaders, equipment leasing is not a tactical workaround. It is a structuring decision that influences how capital moves through the business and how growth is managed over time.

Tax Timing, Not Just Tax Deductions

Leasing affects when costs are recognized, not just whether they are deductible.

- Lease structure determines whether costs are deducted as ongoing expenses or recovered through depreciation and interest.

- Timing matters for taxable income, forecasts, and covenant compliance.

- Identical equipment can produce very different tax outcomes based solely on structure and execution.

Cash Flow Alignment With Revenue

Leasing is often used to preserve liquidity and control cash timing.

- Costs are spread across predictable payments rather than concentrated upfront.

- Capital outflows can be aligned with when equipment begins producing revenue.

- Working capital stays available for operations, staffing, or additional growth.

This is especially important for businesses expanding capacity or replacing critical equipment under tight timelines.

Balance Sheet Flexibility and Control

Lease structure influences how much flexibility a company retains as it grows.

- Impacts balance sheet presentation and exposure to residual value risk.

- Can help avoid over-encumbrance or unnecessary covenant pressure.

- Preserves optionality as market conditions or growth plans change.

Why Structure Beats Standstill

Strong outcomes come from looking at the full picture, not isolated variables.

- Underwriting evaluates revenue trends, cash generation, equipment usefulness, and timing together.

- CFOs who apply the same “total story” mindset structure leases that support growth without creating downstream tax or credit friction.

- Discipline upfront reduces surprises later, at tax time and beyond.

When tax treatment, cash flow, and control are considered together, equipment leasing becomes a strategic tool rather than a reactive financing choice.

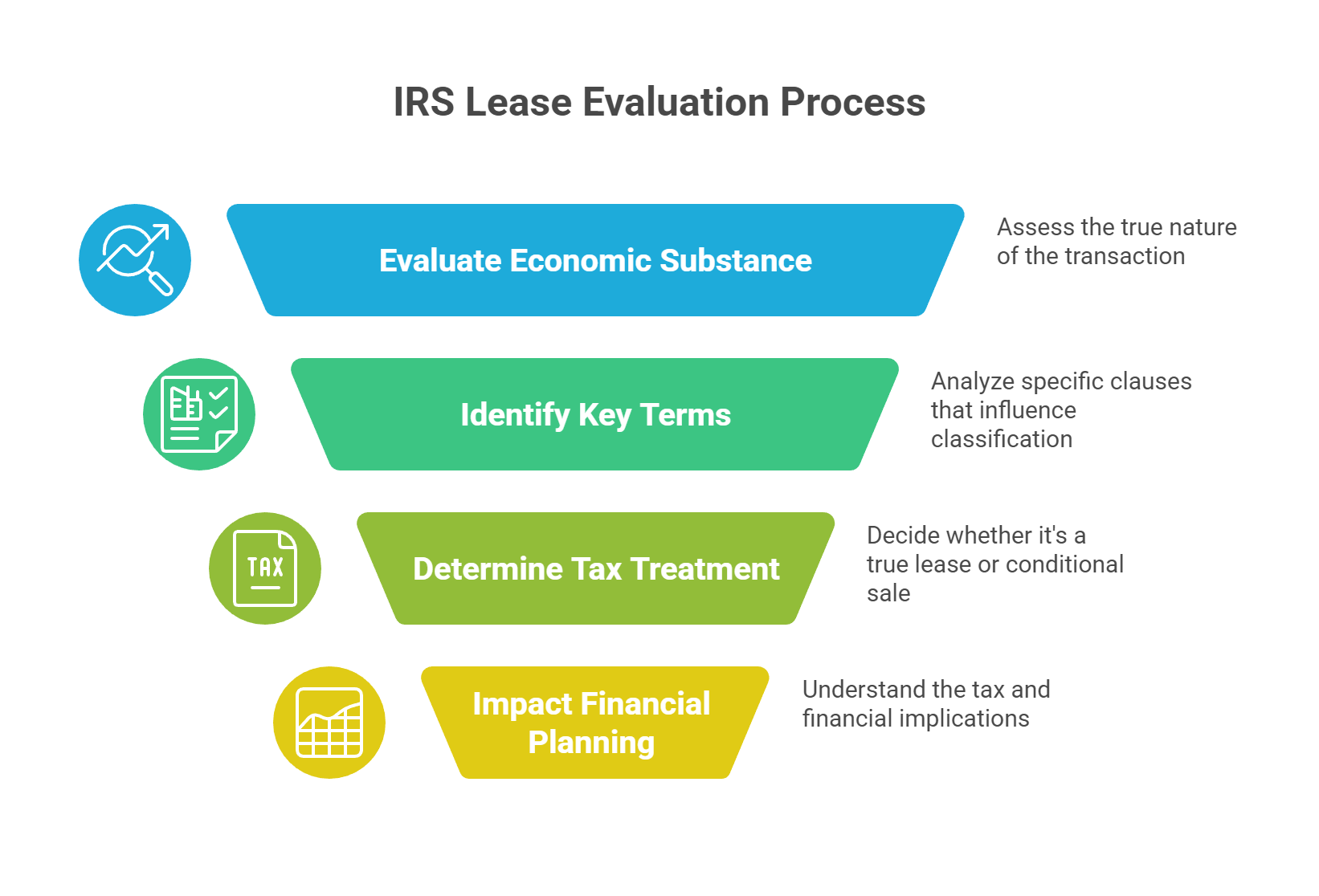

How the IRS Actually Evaluates Equipment Leases

True Lease vs Conditional Sale (The Distinction That Drives Tax Treatment)

One of the most persistent misconceptions in equipment finance is that the name on the contract, whether it says “lease” or “loan,” determines how the IRS treats the transaction for tax purposes. In practice, labels matter far less than economic substance and intent.

Substance Over Labels

The IRS evaluates whether an agreement functions as a true lease or, in substance, a conditional sale. This distinction is critical because it drives how costs are recovered for tax purposes.

- If a transaction qualifies as a true lease, lease payments are generally treated as rental expenses and deducted over time.

- If a transaction is recharacterized as a purchase, the business is treated as owning the equipment for tax purposes, shifting deductions to depreciation and interest.

The classification is based on how the agreement actually works, not how it is marketed.

What Can Trigger Recharacterization

Certain lease terms can cause the IRS to view an agreement as a purchase rather than a rental. Common examples include:

- Purchase options that make ownership virtually guaranteed

- Automatic or nominal-cost transfers of ownership at the end of the term

- Payment structures that effectively recover the full economic value of the equipment

The core issue is intent. A true lease transfers the right to use equipment for a period of time, not ownership of the asset itself.

Why Classification Matters

How a lease is classified directly affects your tax treatment and financial planning:

- True lease: Payments are typically deductible as operating expenses, supporting predictable cash flow and simplified expense treatment.

- Conditional sale: The equipment is capitalized and depreciated, and only the interest portion of payments is deductible.

From a CFO perspective, this distinction influences tax timing, reporting complexity, and long-term flexibility.

At Equipment Leases, Inc., we place a premium on clear documentation and disciplined structuring. This mirrors Traci Dolphin’s “total story” underwriting approach, where intent, economics, and execution all align. By structuring leases transparently and coordinating early with clients and their advisors, we help reduce ambiguity and support consistent tax treatment over the life of the equipment.

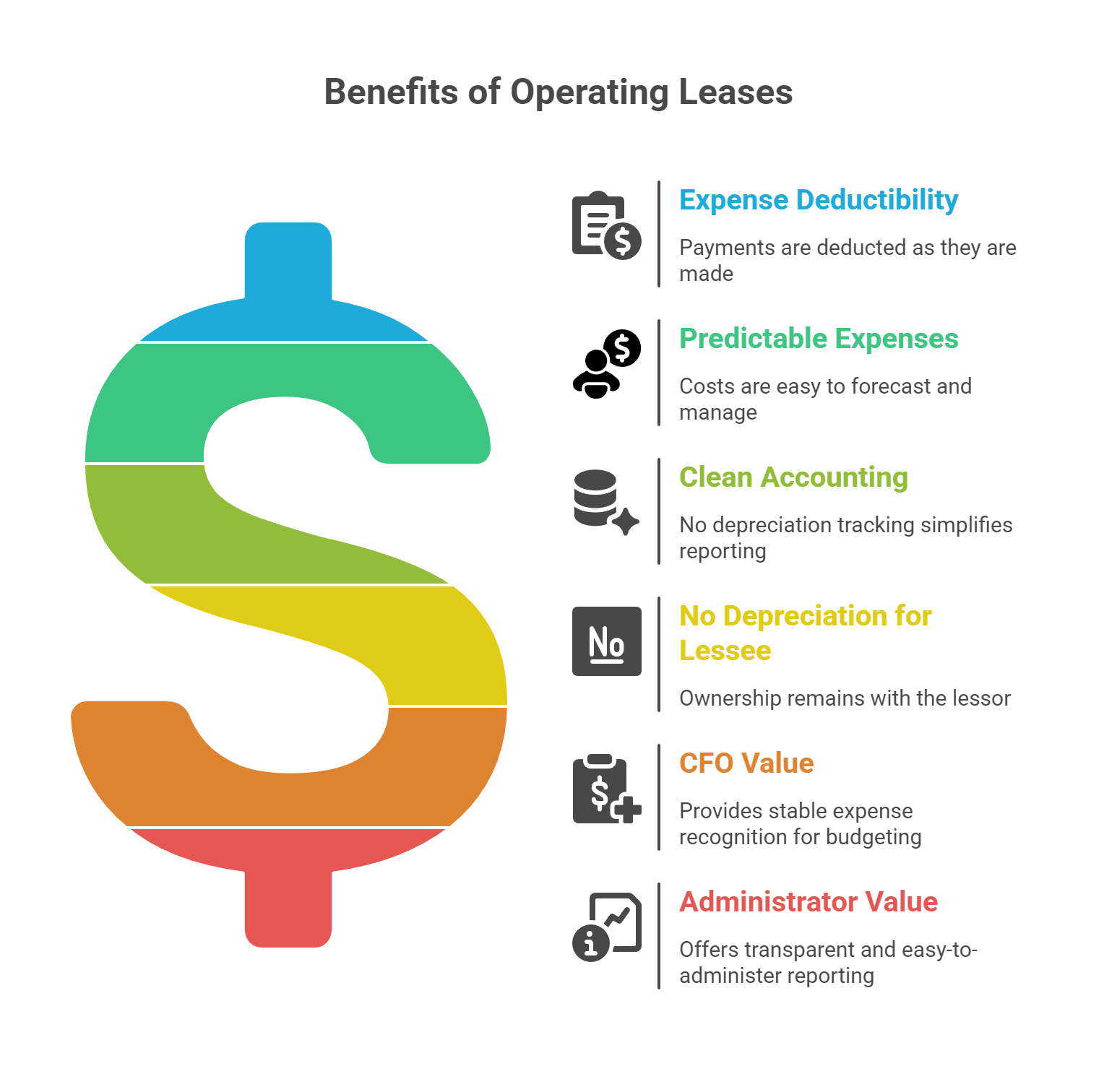

Operating Lease Tax Treatment (Predictability and Simplicity)

Operating leases remain the most widely used and frequently misunderstood financing structure in equipment acquisition. For finance leaders, the primary appeal of an operating lease is its simplicity. Lease payments are typically treated as deductible operating expenses, aligning directly with payment timing and cash flow.

Expense Deductibility and Timing

Unlike equipment purchases or ownership-oriented lease structures, operating leases generally allow companies to deduct payments as they are made. There is no requirement to capitalize the asset or maintain depreciation schedules.

This treatment creates two practical advantages:

- Predictable expenses: Deductions follow the payment schedule, making it easier to forecast costs, manage cash flow, and plan taxable income across periods.

- Clean accounting: With no asset to depreciate, reporting remains straightforward, which is especially valuable for medical administrators and organizations that prioritize clarity and consistency.

No Depreciation for the Lessee

In an operating lease, ownership of the equipment remains with the lessor, along with any associated depreciation. The lessee records lease payments as operating expenses only, with no depreciation entries required.

This structure reduces downstream complexity by:

- Eliminating depreciation tracking and adjustments

- Avoiding asset disposition or recapture considerations for the lessee

- Simplifying documentation and ongoing tax reporting

Why CFOs and Administrators Value This Structure

For CFOs managing forecasts, bank covenants, and year-end targets, the predictability of operating lease expenses is often more valuable than aggressive tax acceleration. Stable expense recognition supports disciplined budgeting and minimizes surprises.

Medical administrators and other leaders who prioritize audit-friendly reporting also favor operating leases for their transparency and ease of administration.

At Equipment Leases, Inc., we help clients structure operating leases with these outcomes in mind, ensuring each agreement aligns with tax treatment, cash-flow objectives, and real-world operational needs.

Finance Leases and Leases Structured for Ownership

Not all leases are designed to function as rentals. In many transactions, the intent is long-term control or eventual ownership of the equipment. When a lease is structured this way, the tax treatment begins to resemble a purchase, even though financing is still being used.

Understanding this distinction is critical, because ownership-oriented structures follow a very different tax path than operating leases.

How Ownership-Oriented Lease Tax Treatment Works

When a lease is treated as a purchase for tax purposes, the business is generally viewed as owning the equipment. Instead of deducting lease payments as operating expenses, costs are recovered through:

- Depreciation of the equipment over its applicable recovery period

- Interest expense deductions tied to the financing component of payments

This approach can create larger deductions earlier in the life of the asset, but it also introduces more complexity and requires careful coordination between the CFO, CPA, and lender.

Section 179 and Bonus Depreciation Considerations

Accelerated deductions such as Section 179 and bonus depreciation may be available in ownership-oriented lease structures, but eligibility is highly dependent on how the transaction is structured and on the taxpayer’s specific circumstances.

Key points CFOs should keep in mind:

- Not all leases qualify for Section 179 or bonus depreciation.

- Eligibility depends on ownership treatment, asset type, and current-year tax rules.

- Accelerated deductions can be valuable, but they are not universally beneficial and may create future tax planning trade-offs.

This is an area where assumptions often lead to disappointment. Responsible structuring focuses on alignment, not maximizing deductions at any cost.

Why “Placed in Service” Timing Matters

For ownership-oriented structures, when the equipment is placed in service is often more important than when a lease is approved, signed, or funded.

- Tax deductions generally begin when the equipment is available for its intended use.

- Delays in delivery, installation, or commissioning can shift deductions into a different tax year.

- Misunderstanding this timing can create unexpected gaps between financing and tax treatment.

From an underwriting perspective, this timing is evaluated carefully, especially in complex projects involving installation, progress funding, or multi-stage builds.

Section 179 and Bonus Depreciation, Where Leasing Fits and Where It Doesn’t

Section 179 and bonus depreciation are often the first topics raised when tax benefits of equipment financing come up. When used appropriately, accelerated deductions can be powerful. When applied without structure, they can just as easily create misalignment or future tax friction.

Leasing alone does not create eligibility. The way the transaction is structured, and how the business is treated for tax purposes, determines whether these deductions apply.

When Accelerated Deductions May Apply

Section 179 and bonus depreciation are generally tied to ownership treatment for tax purposes. In certain ownership-oriented lease structures, a business may be able to take advantage of accelerated deductions if it otherwise meets eligibility requirements.

That determination depends on several factors, including:

- Whether the lease is treated as a purchase for tax purposes

- The type of equipment involved and how it is used

- The taxpayer’s broader financial and tax situation

- Current-year rules and limitations

Because these variables change, eligibility must be evaluated in context, not assumed.

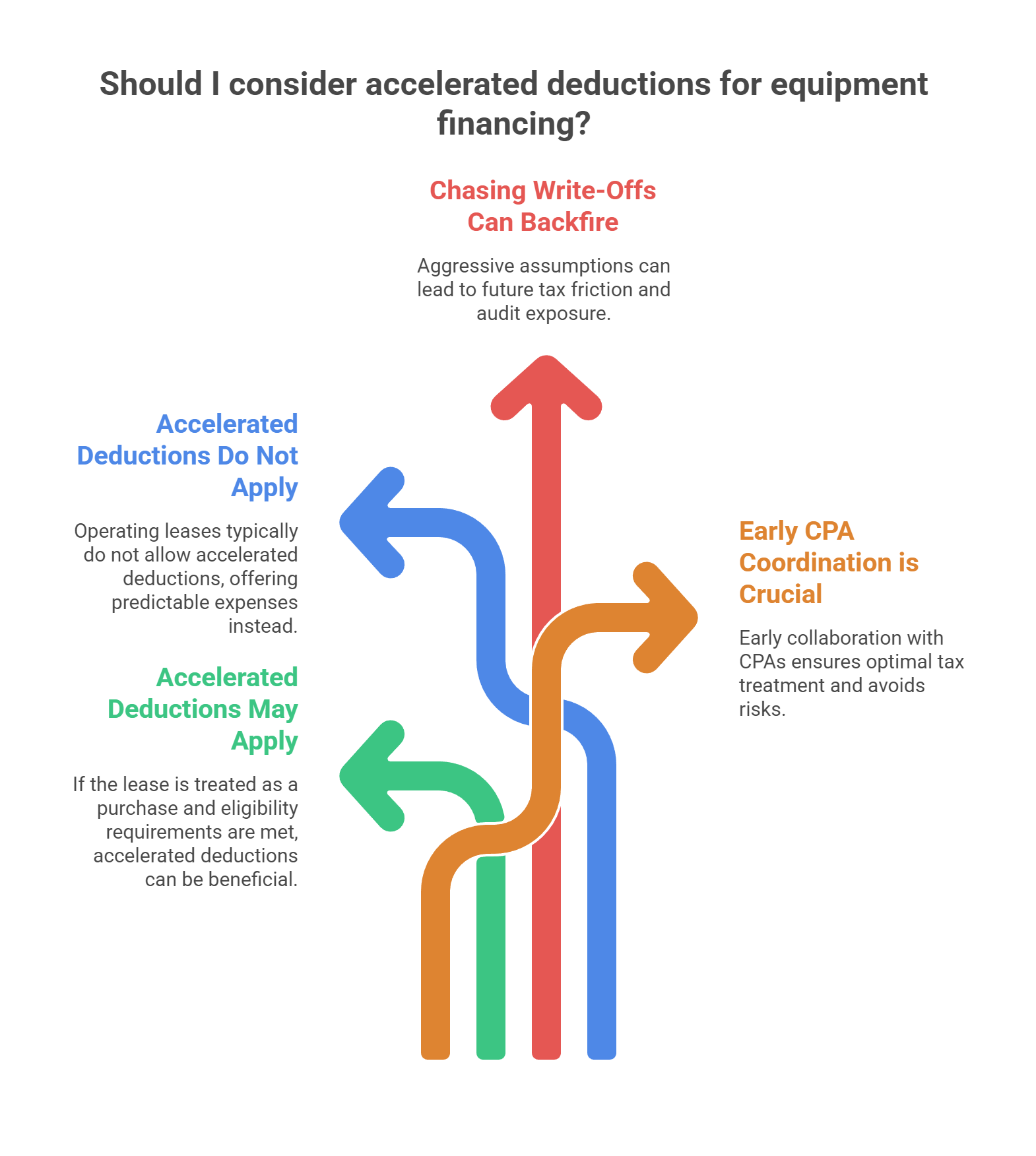

Where Leasing Does Not Fit

Operating leases that qualify as true leases for tax purposes typically do not allow the lessee to claim Section 179 or bonus depreciation. In those cases, the tax benefit comes from predictable expense deductions over time, not from accelerated write-offs.

Confusion often arises when businesses expect operating lease simplicity and ownership-based tax benefits at the same time. Those outcomes rarely co-exist without creating risk.

Why Chasing Write-Offs Can Backfire

Accelerated deductions can improve near-term tax results, but they are not universally beneficial.

- Front-loading deductions may increase taxable income in future periods.

- Aggressive assumptions can create audit exposure if structure and intent are misaligned.

- Tax-driven decisions that ignore cash flow or covenant impact can introduce operational stress.

The Importance of Early CPA Coordination

This is where disciplined coordination matters. Lenders structure the transaction, but CPAs determine tax treatment. The strongest outcomes occur when those conversations happen early.

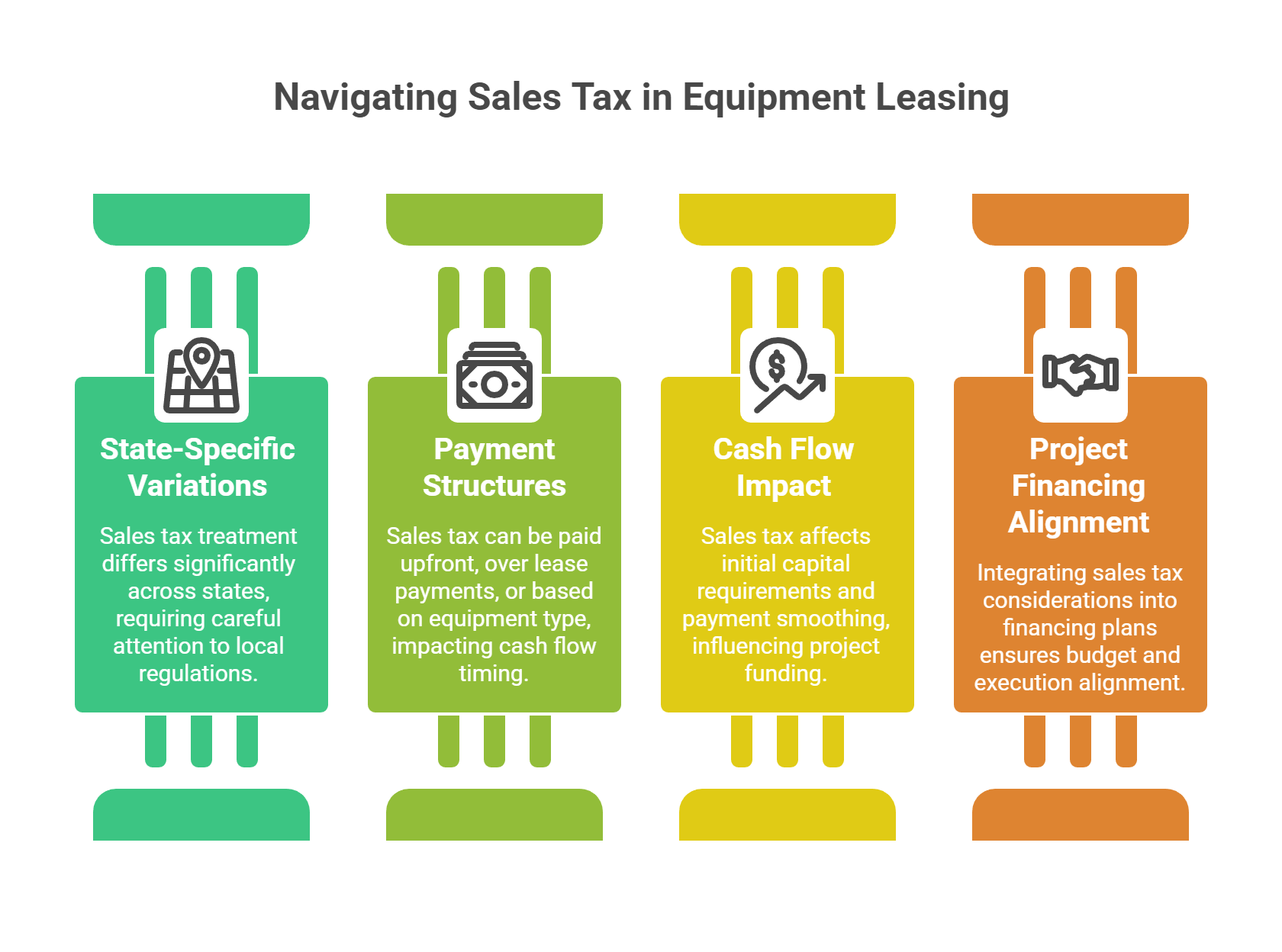

Sales Tax Treatment in Equipment Leasing

Sales tax is one of the most common sources of surprise in equipment transactions. It often receives less attention than income tax treatment, yet it can have a meaningful impact on project budgets and cash flow if it is not addressed early.

The most important thing to understand is that sales tax treatment varies by state. There is no single rule that applies across all jurisdictions, and assumptions made too late in the process can create unnecessary friction.

How Sales Tax Is Typically Handled

Depending on the state and the structure of the lease, sales tax may be:

- Due upfront at the time of acquisition

- Applied to each lease payment over the term

- Assessed differently based on equipment type or usage

Each approach affects cash timing in a different way. Even when the total tax expense is similar, the timing of those payments can materially change how a project is funded and managed.

Why Cash Timing Matters

Sales tax is not just a compliance issue. It is a cash-flow consideration.

- Upfront sales tax increases initial capital requirements.

- Tax spread over payments smooths cash outflows but may increase total payment amounts.

- Late clarity can force last-minute adjustments to budgets or financing structures.

For operations leaders managing installation timelines or multi-vendor projects, these timing differences can influence execution just as much as the equipment cost itself.

Aligning Sales Tax With Project Financing

Because sales tax interacts directly with funding needs, it should be considered alongside the full project scope. Equipment cost, installation, shipping, and other soft costs all factor into how a transaction is structured.

At Equipment Leases, Inc., we encourage early discussion around sales tax treatment as part of the overall financing plan. Addressing it upfront helps align cash flow, avoid surprises, and ensure the structure supports both budget expectations and execution timelines.

Common Tax and Structuring Mistakes We See

Most tax and financing issues in equipment leasing do not come from aggressive intent. They come from assumptions made early that are never revisited. Addressing these mistakes upfront reduces risk, shortens timelines, and prevents rework later in the process.

Assuming All Lease Payments Are Deductible

One of the most common misconceptions is that every lease automatically produces deductible payments. In reality, deductibility depends on how the lease is classified for tax purposes.

- Operating leases and ownership-oriented leases are treated very differently.

- The name on the agreement does not control tax treatment.

- Misclassification can force adjustments after the fact.

Clarifying intent and structure early avoids this issue.

Ignoring Placed-in-Service Timing

Another frequent mistake is focusing on approval or funding dates rather than when the equipment is actually placed in service.

- Tax treatment generally begins when equipment is available for its intended use.

- Delays in delivery, installation, or commissioning can shift deductions into a different period.

- This matters most in year-end transactions and multi-phase projects.

Ignoring this timing can create gaps between financing expectations and tax reality.

Structuring Leases That Conflict With Tax Intent

Problems arise when lease terms are not aligned with the desired tax outcome.

- Agreements designed for simplicity may unintentionally resemble ownership.

- Ownership-oriented structures may be paired with expectations better suited to operating leases.

- Inconsistent intent creates ambiguity and downstream questions.

Structure should support intent, not undermine it.

Weak Documentation and Late CPA Involvement

Documentation and coordination matter more than many businesses expect.

- Incomplete or inconsistent records slow approvals and complicate tax reporting.

- Bringing a CPA in late limits options and increases the likelihood of revisions.

- Early alignment reduces friction and improves outcomes.

This emphasis on preparation reflects Traci Dolphin’s underwriting approach, where clarity and consistency support both funding and long-term success.

The common thread across these issues is timing. CFOs who address structure, documentation, and intent early remove friction before it appears. That discipline reflects Steve Hansen’s philosophy that the best deals are built through preparation, not correction.

When Leasing Supports Tax Strategy, and When It Doesn’t

Leasing is commonly favored when predictability and liquidity matter more than maximizing near-term deductions.

- Cash preservation: Leasing spreads costs over time, keeping working capital available for operations or growth.

- Expense predictability: Operating lease structures provide stable, forecastable expenses that align with revenue generation.

- Flexibility: Leasing can reduce long-term commitment and preserve optionality as business conditions change.

For companies managing growth, covenants, or multi-year planning, these characteristics often outweigh the appeal of accelerated tax deductions.

In certain situations, ownership treatment can be more effective from a tax perspective.

- Businesses with strong cash flow may benefit from depreciation and interest deductions.

- Accelerated deductions may align with specific tax planning objectives.

- Long-term equipment use can justify ownership-based structures.

These scenarios require careful coordination, as the benefits depend on eligibility, timing, and the company’s broader tax position.

There is no single correct answer across all situations. The outcome depends on:

- How the lease or financing is structured

- When the equipment is placed in service

- How the investment fits into growth plans and capital strategy

The most effective tax strategies are built around alignment. When structure, timing, and business objectives support one another, leasing or ownership can be used intentionally, without creating surprises later.

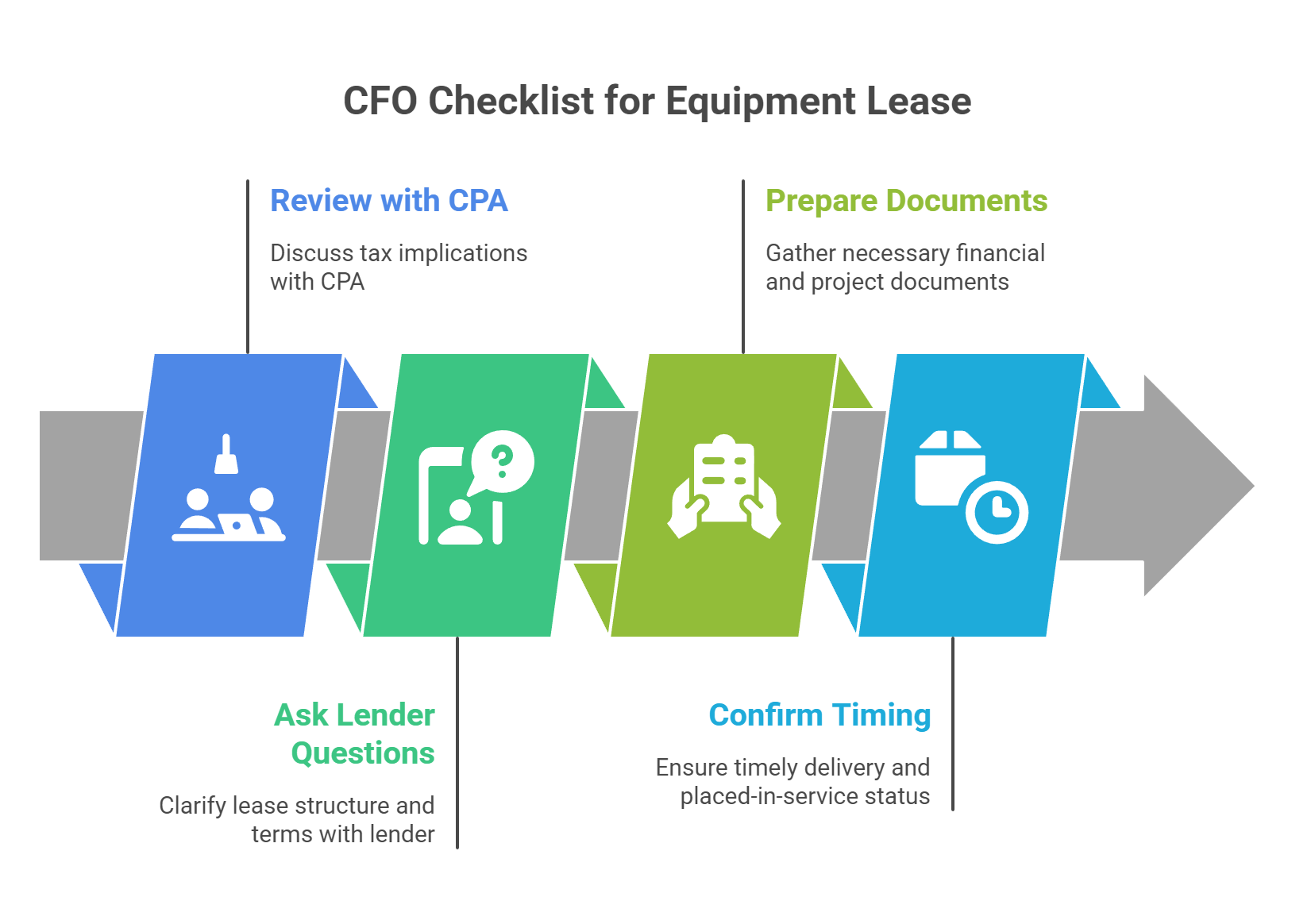

A CFO Checklist Before Signing an Equipment Lease

Transforming insight into results starts with asking the right questions and preparing the right documentation.

Here’s a practical checklist, based on our real-world underwriting experience, to help CFOs maximize both tax and operational benefits before finalizing any equipment lease.

Questions to Review With Your CPA

- How will this lease be classified for tax purposes based on its structure?

- Does the structure support our desired tax treatment, or are there conflicts?

- If ownership treatment applies, when will depreciation or other deductions begin?

- Are there state or industry-specific considerations that affect tax treatment?

- How does this transaction fit into our broader tax planning for the year?

Early CPA involvement helps confirm assumptions before terms are finalized.

Questions to Ask Your Lender

- How is this lease structured from an underwriting and documentation standpoint?

- Does the structure align with our tax and cash-flow objectives?

- How are soft costs such as installation, shipping, or software handled?=

- What assumptions are being made about delivery and placed-in-service timing?

- Are there flexibility options if timelines or project scope change?

Clear lender communication reduces rework and surprises later.

Documents to Prepare in Advance

Having documentation ready accelerates both underwriting and tax coordination.

- Recent financial statements and supporting schedules

- Equipment quotes, vendor contracts, and project timelines

- Installation or commissioning plans, if applicable

- Any existing covenant or financing constraints

Preparation supports faster approvals and cleaner execution.

Timing Considerations to Confirm Early

Timing affects both funding and tax treatment.

- When will the equipment be delivered and ready for use?

- Are there dependencies that could delay placed-in-service status?

- Does the transaction need to close within a specific tax year?

- How do progress payments or phased installations affect timing?

This checklist mirrors the intake and underwriting discipline used at Equipment Leases, Inc.. When these questions are addressed early, transactions move faster, assumptions hold, and outcomes are more predictable.

How We Help Structure Equipment Leases With Tax and Cash Flow in Mind

At Equipment Leases, Inc., our role is to help finance leaders translate strategy into execution. We are not here to sell a one-size-fits-all solution or promise specific tax outcomes. We structure equipment leases so they align with how businesses actually operate, fund projects, and plan for growth.

A Direct Lender Perspective

Because we underwrite and fund transactions directly through our relationship with Commercial Funding Partners, we see the full lifecycle of a deal. That perspective matters. It allows us to evaluate structure, timing, and documentation together, rather than in isolation. Decisions are made with an understanding of how they affect cash flow, tax treatment, and long-term flexibility.

Aligning 100% Project Financing With Real Needs

Many equipment projects involve more than the asset itself. Installation, shipping, software, and other soft costs often determine whether a project moves forward smoothly or stalls. When appropriate, we structure financing to cover the full scope of the project, aligning payments with execution and revenue generation rather than forcing upfront cash outlays.

Coordinating Early With CPAs and Advisors

Tax treatment is determined by facts and circumstances, not assumptions. We encourage early coordination between the CFO, the CPA, and our credit team so structure and intent remain aligned. This collaboration reduces rework, avoids surprises, and supports consistent outcomes after the deal closes.

Equipment-Only Collateral and Progress Funding

When a transaction calls for it, we structure leases around equipment-only collateral, avoiding unnecessary encumbrances on the broader business. For complex or phased projects, progress funding can be used to align payments with build or installation milestones, supporting cash flow without disrupting operations.

Our approach is intentionally disciplined and partner-focused. We aim to be a reliable resource throughout the process, helping clients structure equipment leases that support tax planning, preserve liquidity, and execute cleanly in the real world.

Ready to Explore Your Options?

Every organization’s needs are unique, and the right lease structure can make a significant difference in both tax outcomes and cash flow. If you’d like to sanity-check how these strategies might apply to your situation, or if you want to walk through structure options with your CPA, we’re here to help.

Let’s connect:

- Request a Quote for a tailored financing solution

- Contact Us to discuss your project or get your questions answered

We’re happy to serve as a resource and partner as you plan your next equipment investment.