Most businesses know Section 179 exists. Far fewer understand that whether they can actually claim it depends less on what they bought and more on how they financed it.

The lease structure you choose determines whether you qualify for the deduction at all. The lender you choose determines whether the deal closes in time to qualify. And the financing model you use determines how much cash you have to spend before capturing the benefit.

That’s the insight most Section 179 content misses. This isn’t purely a tax question. It’s a financing decision.

At Equipment Leases, we structure deals specifically to keep your tax options open. That means dollar-out capital leases that give you ownership treatment for tax purposes. It means 100% financing with no down payment required. And it means same-day credit decisions so a Q4 equipment acquisition doesn’t slip past December 31 because your lender was too slow.

In our experience, the clients who get the most out of Section 179 are the ones who plan the financing first, then confirm the tax strategy with their CPA. This blog walks you through exactly how to do that.

What Is Section 179, and Why Does It Matter for Equipment Buyers?

Most businesses depreciate equipment over its useful life. A piece of manufacturing equipment might have a 7-year depreciation schedule. A computer system might take 5 years. Under standard depreciation, you deduct a fraction of the cost each year until the asset is fully written off.

Section 179 changes that equation entirely.

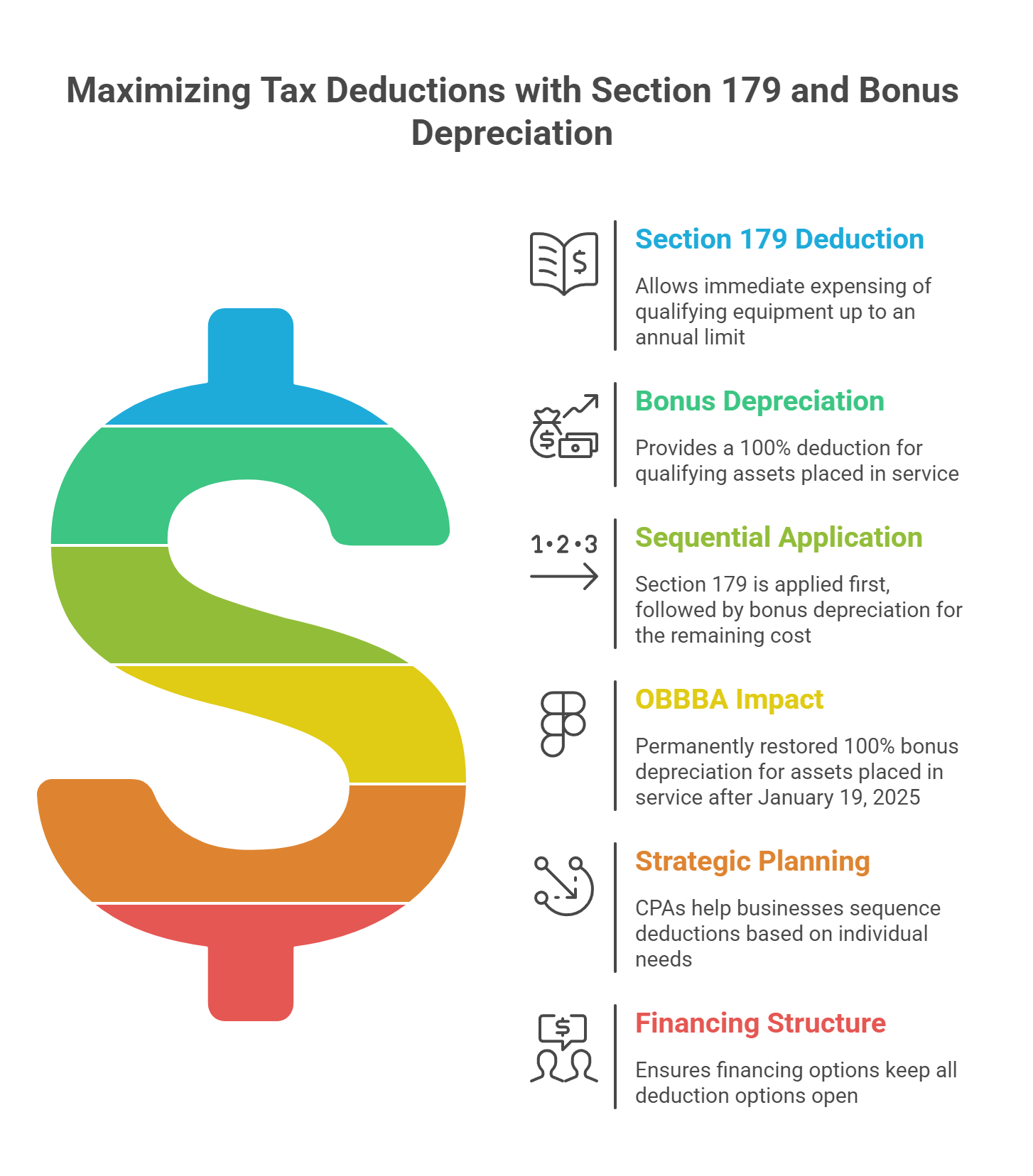

Under Section 179, qualifying businesses can deduct the full cost of eligible equipment in the year it’s placed in service, not spread across years. The equipment generates revenue from day one. The deduction follows immediately, not on a 5 or 7-year lag.

For a CFO managing cash flow and tax liability simultaneously, the difference is significant. A $500,000 equipment purchase deducted over 7 years returns modest annual relief. The same $500,000 deducted in year one is a meaningful reduction in current-year taxable income.

What qualifies

Section 179 applies to tangible personal property used in a U.S. trade or business. This includes most equipment, machinery, and technology assets placed in service during the tax year. Both new and used equipment can qualify, a point many business owners miss.

The equipment must be placed in service before December 31 of the tax year. Ordered, delivered, or approved is not enough. The asset must be installed and available for use.

Current limits

Under the One Big Beautiful Bill Act (OBBBA, signed July 4, 2025), the Section 179 deduction cap increased significantly. The current deduction limit is $2.5M, with phase-out beginning at $4M in total qualifying purchases and reaching full phase-out at $6.5M.

These figures reflect current law as of this writing. Section 179 limits are subject to legislative change and adjust periodically. Confirm current limits with your CPA before planning around a specific figure.

One important constraint

Section 179 cannot create a net operating loss. The deduction is capped at your business’s taxable income for the year. If your deduction exceeds taxable income, the excess carries forward to future tax years. This is an important planning variable — particularly for businesses in lower-income years or those coordinating Section 179 with bonus depreciation. Your CPA is the right person to work through that sequencing.

Section 179 is an election

Unlike bonus depreciation, Section 179 is not automatic. You elect to apply it, and you can apply it selectively to specific assets. This gives your tax advisor flexibility to optimize which purchases receive the deduction in a given year.

Can You Claim Section 179 on Financed or Leased Equipment?

Yes. But the answer depends entirely on how your financing is structured and most businesses don’t know to ask the question until after they’ve signed.

Here is the scenario that plays out more often than it should. A CFO finances $800,000 in manufacturing equipment. The deal closes in November. Equipment is installed before year-end. At tax time, their advisor tells them the lease structure they chose doesn’t qualify for Section 179. The deduction they were counting on isn’t available. The financing decision made two months earlier closed the door.

The good news: this is entirely avoidable. You just need to know which structure to ask for before you sign.

What the IRS actually looks at

The IRS doesn’t ask how much cash you put down. It asks one question: who owns the equipment for tax purposes?

If you are treated as the owner, Section 179 eligibility follows. If the lender retains ownership, it doesn’t. That determination is made by the lease structure, not the payment schedule.

The two structures, side by side

| Dollar-Out Capital Lease | FMV Operating Lease | |

|---|---|---|

| Who owns the equipment for tax purposes | You | The lender |

| On your balance sheet | Yes | No |

| End of term | You purchase for $1 | You purchase at fair market value or return the equipment |

| Monthly payments | Higher | Lower |

| Section 179 eligible | Yes, subject to IRS requirements | No |

| Lease payments deductible as expense | No | Yes |

| Bonus depreciation eligible | Yes | No |

What a dollar-out capital lease looks like in practice

You finance $800,000 in equipment. The lease is structured as a dollar-out capital lease. From day one, that equipment sits on your balance sheet as an asset. You make monthly payments over the lease term. At the end of term, you purchase the equipment for $1. We release the lien, and you own it outright, the same way a car loan works when the final payment clears.

Because you hold ownership for tax purposes from the start, the asset may qualify for a full Section 179 deduction in year one. Your CPA confirms the structure and calculates the deduction. The financing decision you made upfront is what made it possible.

What an FMV operating lease looks like in practice

Same $800,000 in equipment. This time, structured as an FMV operating lease. Your monthly payments are lower. The equipment stays off your balance sheet, which can be useful if you’re managing covenants with your existing bank. At the end of term, you have the option to purchase at fair market value or return the equipment.

The tax treatment is different. You deduct your lease payments as an ordinary business expense each year. Section 179 on the asset itself is not available because the lender, not you, holds ownership for tax purposes.

Neither structure is wrong. They serve different financial goals. The decision comes down to your balance sheet priorities, your tax strategy, and what your CPA recommends for your situation.

The placed-in-service requirement still applies

Whichever structure you choose, the equipment must be placed in service before December 31 of the tax year. A signed agreement doesn’t satisfy the requirement. The equipment must be installed and operational within the year you intend to claim the deduction. We’ll cover why your lender’s speed matters here in Section 5.

We’re a financing partner, not a tax advisor. Work with your CPA or tax advisor to confirm which lease structure fits your accounting and tax situation before you sign. That conversation is worth having before the equipment arrives, not after.

Finance 100% of the Equipment and Still Take the Full Deduction

Here is the combination most businesses never consider.

You need $600,000 in manufacturing equipment. Your bank wants 15% down; $90,000 out of pocket before the equipment arrives. That’s cash that could stay in operations, cover payroll through a slow quarter, or fund the next hire.

Now consider a different path. Finance 100% of the equipment through Equipment Leases. No down payment. The full $600,000 is financed as a dollar-out capital lease. The equipment is installed and operational before December 31. Because you hold ownership for tax purposes, the full cost may qualify for a Section 179 deduction in year one.

You preserved $90,000 in cash. You potentially deducted $600,000.

That is the combination. And it is available right now.

Why this works

Section 179 eligibility is determined by ownership treatment, not how much cash you spend. A business that finances 100% of an equipment purchase under a dollar-out capital lease is in the same tax position as one that pays cash, as far as the IRS is concerned.

Most lenders require a down payment. That means businesses are spending cash they don’t need to spend to access a deduction that doesn’t require it.

We offer 100% financing with no down payment. Equipment-only collateral. No blanket liens on your business, receivables, or other assets. The equipment stands on its own.

What the numbers can look like

The example below is illustrative. Actual tax outcomes depend on your business’s taxable income, effective tax rate, lease structure, and your CPA’s guidance. Use this as a framework for the conversation with your advisor, not as a projection.

| Example Scenario | |

|---|---|

| Equipment cost | $600,000 |

| Down payment required | $0 (100% financed) |

| Lease structure | Dollar-out capital lease |

| Potential Section 179 deduction | Up to $600,000 |

| Estimated tax savings at 25% effective rate | Up to $150,000 |

| Cash deployed to access the deduction | $0 |

Your first-year lease payments will be a fraction of that potential tax savings. The cash you preserve by financing 100% stays in your business.

What this means for your Q4 planning

The businesses that get the most value from this combination are the ones that plan it intentionally. That means choosing the right lease structure before signing. It means confirming eligibility with your CPA before year-end. And it means working with a lender who can move fast enough to place the equipment in service before December 31.

We provide same-day credit decisions for qualified applicants. LOIs for mid-ticket projects typically follow within 24 to 48 hours. The financing process does not have to be the bottleneck in your tax strategy.

Talk to your CPA about whether this combination fits your situation. Then talk to us about structuring the deal.

Section 179 Limits, Phase-Outs, and What Changes Under the OBBBA

Section 179 works well for most mid-market equipment acquisitions. But if your business is planning a large capital year, the deduction doesn’t behave the same way at every purchase level. Knowing where the thresholds sit helps you plan the right structure before you commit.

What happens when your purchases climb

Say your business acquires $5M in qualifying equipment this year. Under current law, Section 179 begins phasing out at $4M in total qualifying purchases, dollar for dollar above that threshold. At $5M, you’ve lost $1M of available deduction before your CPA runs a single number.

At $6.5M in total qualifying purchases, Section 179 phases out entirely.

This isn’t a reason to avoid Section 179. It’s a reason to understand it. Businesses approaching those thresholds shift more of their first-year deduction strategy to bonus depreciation, which has no dollar cap.

The order matters

When you use both deductions in the same year, Section 179 goes first. Bonus depreciation applies to any remaining eligible cost after Section 179 is maximized. Your CPA sequences them based on your taxable income, total purchase volume, and entity structure. Getting that order wrong or not planning for it, leaves deductions on the table.

Your state may treat this differently

A federal Section 179 deduction doesn’t automatically carry through to your state return. Some states conform to federal limits. Others don’t. If your business operates in a state that hasn’t adopted the current federal rules, your state tax liability may look very different from your federal picture.

This is a short conversation with your CPA that can prevent a significant surprise at filing.

One more variable for lower-income years

If your business is in a year with lower taxable income, Section 179 hits a ceiling, the deduction can’t exceed your business income, and excess carries forward. Bonus depreciation has no such restriction. It can generate a net operating loss, which carries forward to future years.

That distinction changes which tool leads your strategy depending on where your income lands. Your CPA determines the right sequencing for your situation.

All figures reflect current law as of this writing and are subject to legislative change. Confirm current limits with your CPA before executing.

Why the Year-End Deadline Makes Your Lender Choice a Tax Decision

Your financing partner and your tax strategy are not two separate conversations when you’re buying equipment in Q4. They are the same conversation.

Here is why.

To qualify for Section 179, your equipment must be placed in service before December 31. Not ordered. Not approved. Not sitting on the loading dock. Installed and operational. That requirement puts a hard deadline on every year-end acquisition and your lender controls a significant portion of the time between now and that date.

What a slow lender costs you

You start the financing process in early November. Your lender takes two weeks to review, another week for committee approval, ten days to prepare documents. Funding hits in late December. Your vendor needs two weeks for delivery and installation.

January 3rd. Your equipment is operational. Your Section 179 deduction is gone.

Your lease structure was right. Your timing was right. Your lender was too slow.

What our timeline looks like

- Complete our online application in about seven minutes

- Our team contacts you within 15 minutes

- $100,000–$500,000 projects: LOI typically within 24–48 hours

- Multi-million dollar projects: credit decision in two to three weeks

- After final documents are signed: funds wired within 24 hours

- A November start date gives you enough runway to receive, install, and place equipment in service before December 31

The planning recommendation

Build your lender’s timeline into your tax plan before you commit to an equipment purchase , not after. Confirm your vendor’s installation timeline before you sign anything. And work with your CPA around a realistic placed-in-service date, not an optimistic one.

A lender that can’t move within your window isn’t just slow. In a year-end acquisition, it’s a tax liability.

Section 179 and Bonus Depreciation: Using Both Tools in the Same Year

The question we hear most often: which one is better, Section 179 or bonus depreciation?

The more useful question: how do you use both in the same year?

They are not competing tools. They are sequential ones. Section 179 goes first. Bonus depreciation applies to any remaining eligible cost after Section 179 is maximized. Used together, they can eliminate most or all of your taxable equipment cost in year one.

How they differ

| Section 179 | Bonus Depreciation | |

| Annual dollar limit | Yes ($2.5M cap under current law) | No limit |

| Income limit | Capped at business taxable income | No income limit |

| Can create a net operating loss | No | Yes |

| Election required | Yes, per asset | Automatic (opt out if needed) |

| Asset class flexibility | Elect per asset or group | Applies to entire asset class |

| Applies to used equipment | Yes | Yes |

| Current rate | Up to 100% of eligible cost | 100% (permanently restored) |

Figures reflect current law as of this writing. Confirm limits and eligibility with your CPA before executing.

What changed under the OBBBA

Bonus depreciation had been phasing down since 2023. By 2025, it was scheduled to drop to 40%. The One Big Beautiful Bill Act, signed July 4, 2025, permanently restored 100% bonus depreciation for qualifying assets placed in service after January 19, 2025.

That phasedown schedule is no longer in effect. Both tools are now available at full strength simultaneously. For your business, that means the first-year deduction potential on a financed equipment purchase is as strong as it has been in years.

Our CEO, Buddy Zarbock, serves on the ELFA Political Action Committee and was part of the industry advocacy effort that helped advance the bonus depreciation restoration. This is a policy area we follow closely, because it directly affects how we structure deals for our clients.

The strategic question for your CPA

With both tools fully available, the planning conversation shifts from “which one can I use?” to “how do I sequence them to get the most out of this year’s purchases?”

The answer depends on your taxable income, total equipment spend, entity structure, and state tax treatment. That sequencing is your CPA’s job. Our job is to make sure your financing structure keeps all the options open.

For a detailed look at how bonus depreciation works with equipment financing, see our companion post: Bonus Depreciation and Equipment Financing: What Businesses Need to Know

How Equipment Leases Works Alongside Your Existing Bank Relationship

If you have a strong bank relationship, keep it. We’re not here to replace it.

Banks are excellent primary lenders. They’re also bound by exposure limits, covenant structures, and down payment requirements that have nothing to do with how creditworthy your business is. At some point, those constraints get in the way of a capital acquisition you’re ready to make. That’s the gap we fill.

Where we step in

- You’ve hit your bank’s exposure cap.

Your income supports the deal. Your bank’s regulators don’t allow more. We fund the additional equipment without touching your existing bank relationship or your covenants. - Your bank requires a down payment

Ten to twenty percent down means cash leaving your business before the equipment generates a dollar of revenue. We offer 100% financing, so your liquidity stays in place and your Section 179 strategy stays intact. - Your bank won’t cover the full project

Shipping, installation, vendor deposits, soft costs, banks frequently exclude these from equipment financing. We fund the complete project, including deposits to international vendors, so your team isn’t bridging the gap out of pocket. - You need to protect your balance sheet

An FMV operating lease keeps financed equipment off your books, preserving your borrowing capacity with your existing lender. If managing your covenant ratios is part of the plan, that structure gives you the equipment without the balance sheet impact.

The businesses that get the most out of working with us are the ones that bring us in alongside their bank, not instead of it. Your bank handles what it handles well. We handle what it can’t.

Ready to Finance Equipment with Your Tax Strategy in Mind?

You now have the framework. The lease structure that keeps the deduction available. The financing model that preserves your cash. The timeline that keeps December 31 in reach.

The next step is your CPA. Confirm the structure that fits your situation. Then bring us in to build the financing around it.

We offer dollar-out capital leases and FMV operating leases. We finance full projects, multiple vendors, staged builds, international deposits. And we move fast enough that your year-end plans don’t slip.

We’re on your team. Tell us what you’re building.

Equipment Leases, Inc. is a wholly owned subsidiary of Commercial Funding Partners, a direct lender that secured more than $100 million in equipment financing in 2024.