Equipment leasing is not about finding cheaper payments. It is about using your capital more intelligently.

When structured correctly, leasing helps you preserve liquidity, align equipment costs with revenue, and manage after-tax cash flow without slowing growth. The impact comes from the structure of the lease, not from marketing claims or generic tax language.

Most leasing decisions are not driven by approval. They are driven by timing and control. Capital allocation mistakes rarely show up at signing. They appear later, when cash is constrained and opportunities require liquidity.

A well-structured lease helps reduce that risk by preserving cash while the equipment generates value over time.

Leasing Is Not About Spending Less, It’s About Using Capital Better

Once the decision shifts from ownership to capital strategy, the focus becomes how each dollar is deployed.

Leasing allows you to:

- Direct capital toward higher-return uses

- Avoid locking cash into equipment on day one

- Prioritize cash deployment over ownership timing

This approach supports flexibility during expansion. When demand accelerates or conditions change, retaining liquidity provides options that a fully funded cash purchase does not.

Structured this way, leasing becomes a tool for maintaining control as the business scales, rather than a transactional financing choice.

Matching Equipment Costs to Revenue Generation

Most equipment generates revenue over time, not on day one. How those costs are timed affects both visibility and planning accuracy.

Leasing aligns equipment expense with the useful life of the asset, rather than front-loading the financial impact at purchase. This approach helps avoid early cash flow distortion, especially during ramp-up periods.

Key planning advantages include:

- Expenses that track alongside revenue generation

- More accurate forecasting and budgeting

- Clearer measurement of true return on investment

Front-loaded purchases can mask performance in the early months, even when the equipment is doing exactly what it should. Leasing produces cleaner operating visibility, allowing finance teams to evaluate results as the asset contributes over time.

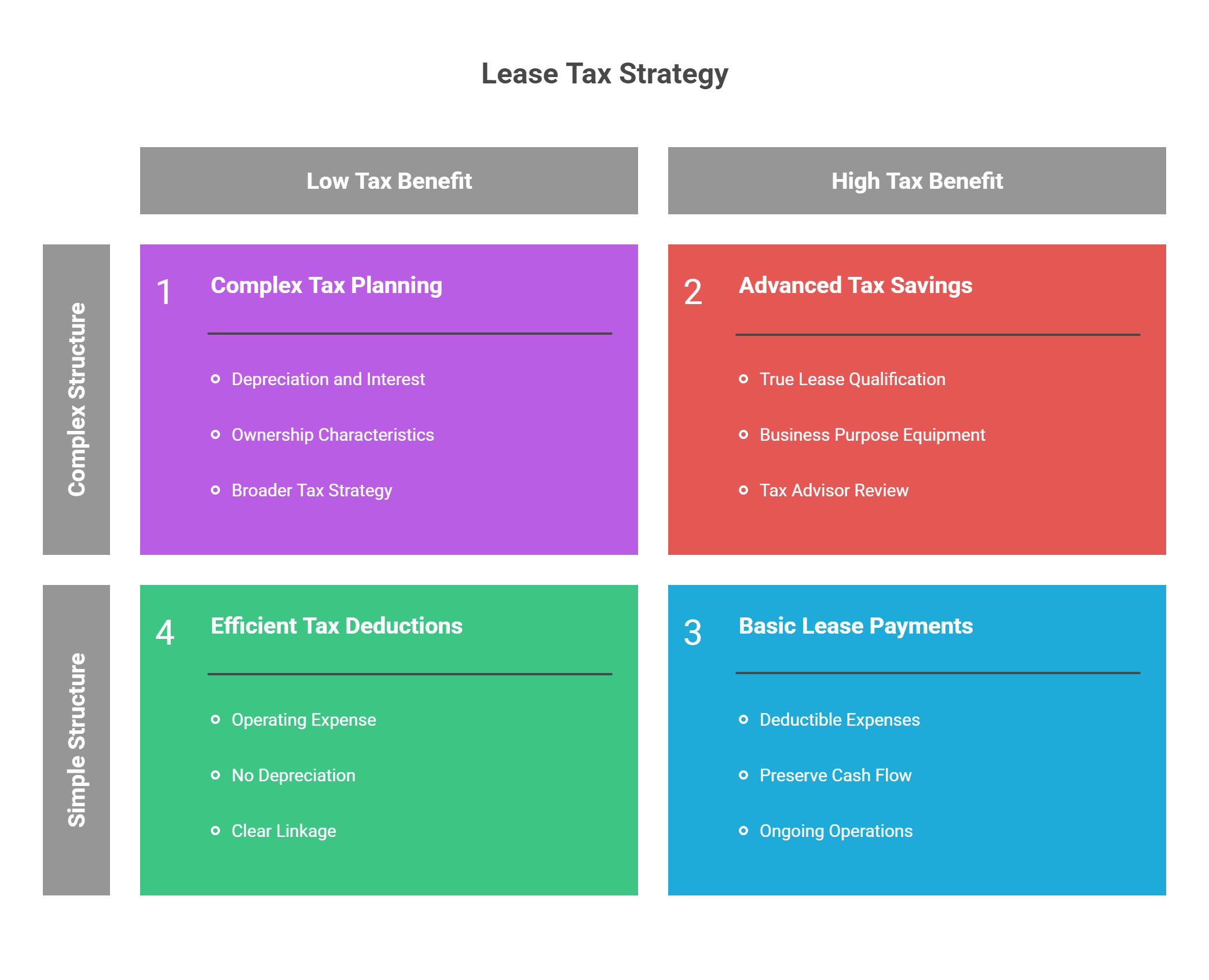

Tax Efficiency of Equipment Leasing, What CFOs Should Know

Operating Lease Deductions

In a properly structured operating lease, lease payments may be deductible as ordinary business expenses. This can reduce taxable income while preserving cash that would otherwise be deployed upfront.

For many CFOs, operating leases also simplify planning:

- Payments are treated as ongoing operating expenses

- No depreciation schedules to manage

- Clear linkage between expense timing and operations

Two factors determine deductibility:

- The lease must qualify as a true lease, not a conditional sale

- The equipment must be used for qualified business purposes

Structure and documentation matter. Deductibility is not automatic and should always be reviewed with your tax advisor.

Depreciation and Structure Flexibility

Some lease structures are treated differently for tax purposes. In certain cases, depreciation and interest expense may apply instead of payment deductibility. This can be advantageous depending on timing, profitability, and broader tax strategy.

Key considerations include:

- Selecting structure based on tax objectives, not just monthly payment

- Understanding how ownership characteristics affect treatment

- Coordinating lease terms with your CPA before execution

The right structure varies by company, asset type, and planning horizon. There is no universal “best” option.

Compliance and Planning Context

Tax treatment and accounting treatment are not the same. A lease may be classified one way for accounting purposes and another for tax purposes. Clear separation of those concepts helps avoid confusion and supports cleaner reporting.

This information is not tax advice. Final tax treatment should always be confirmed with your CPA. Equipment leasing works best when the lender, finance team, and tax advisor are aligned on structure from the start.

Leasing vs Buying Equipment, Cash Flow and Tax Comparison

When you compare leasing to buying, the real question is how each option affects your cash and flexibility, not just the total price of the equipment.

A cash purchase typically means:

- Cash leaves the business immediately

- Tax benefits are spread over long depreciation schedules

- Once capital is deployed, flexibility is limited

This can be appropriate in some cases, but it concentrates both cash outlay and risk at the start of the project.

Leasing changes the timing of both cash flow and tax impact:

- Cash stays available for operations and growth

- Payments may be deductible over time, depending on structure

- End-of-term options allow you to reassess ownership later

From a finance leadership perspective, leasing is not about paying less overall. It is about preserving liquidity and controlling timing. Cash retained in the business can support expansion, absorb variability, or be deployed where returns are higher while the equipment generates value.

The right choice depends on your growth plans, cash priorities, and tax strategy. Leasing gives you another way to balance those factors without forcing an upfront capital commitment.

Soft Costs That Quietly Drain Cash Flow

Equipment projects rarely fail because of the purchase price. They fail because supporting costs are underestimated or unfunded.

Beyond the equipment itself, projects often include:

- Installation and setup

- Shipping and logistics

- Software and integration

- Warranties and service plans

- Training and onboarding

When these costs are paid out of pocket, they create unexpected cash drains that can delay deployment or force reactive financing. Leasing can bundle many of these expenses into a single structure, spreading costs over time instead of concentrating them upfront.

Bundling soft costs improves visibility. Finance teams see the true, all-in project cost from the start, which makes ROI easier to evaluate and manage. It also reduces execution risk during installation and ramp-up.

In practice, timelines are more often stalled by cash gaps than by interest rates. Addressing soft costs upfront is one of the most effective ways to keep projects moving and cash flow stable.

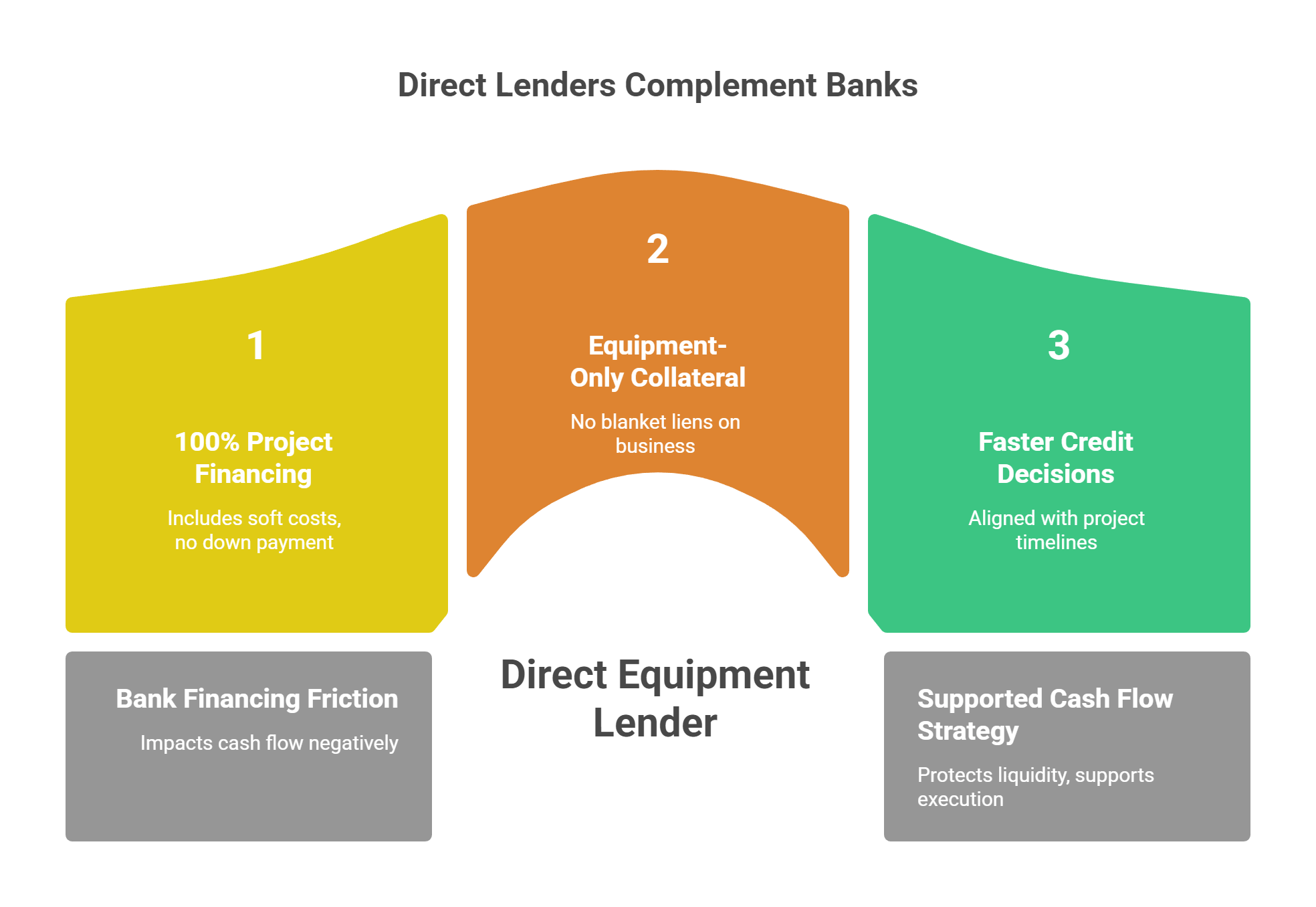

Why Banks Often Undermine Cash Flow Strategy

Traditional banks play an important role, but their structures are not always designed around how equipment projects actually unfold.

In many cases, bank financing introduces friction that impacts cash flow:

- Down payment requirements that pull cash out of the business upfront

- Soft cost exclusions that leave installation, software, or training unfunded

- Long approval timelines that delay deployment and push out ROI

- Rigid structures that do not align with operational realities

These limitations are not a reflection of credit quality. They are a function of how banks are regulated and how their products are built.

This is where a direct equipment lender operates differently:

- 100% project financing, including many soft costs

- Equipment-only collateral, without blanket liens on the business

- Faster credit decisions aligned with project timelines

The goal is not to replace the bank. It is to complement existing banking relationships by structuring equipment financing in a way that protects liquidity and supports execution. When capital structure matches how projects are delivered, cash flow strategy holds together instead of breaking under administrative constraints.

CFO Use Cases Where Leasing Excels

Leasing is not a universal solution, but it is particularly effective in specific situations where timing, liquidity, and flexibility matter.

Common use cases include:

- High-growth capacity expansion, where cash is better deployed across multiple initiatives

- Bank exposure limits, even when the business is otherwise strong and profitable

- Capital-intensive operations that require ongoing equipment investment

- Acquisition-driven strategies, where preserving liquidity supports deal execution

- Year-end or fiscal planning, when timing deductions and cash use is critical

In these scenarios, leasing supports growth without forcing an upfront capital commitment.

From an execution standpoint, leasing is often a sequencing decision, not a replacement for bank financing or ownership. It allows companies to deploy equipment now, preserve cash during critical phases, and revisit ownership later when the balance sheet and operating environment are better aligned.

A CFO Decision Framework for Leasing vs Buying

Use this checklist to evaluate whether leasing or buying better supports your capital strategy.

Equipment Economics

- Does the equipment generate revenue gradually over time rather than immediately?

- Will the asset take time to ramp before reaching full utilization?

Liquidity & Cash Priorities

- Is preserving cash more valuable than owning the asset on day one?

- Would keeping cash available support growth, acquisitions, or risk management?

Forecasting & Planning

- Would fixed, predictable payments improve cash flow visibility?

- Does spreading cost over time simplify budgeting and forecasting?

Tax & Structure Considerations

- Does the lease structure improve after-tax cash flow for your situation?

- Have you reviewed the structure with your CPA to confirm tax treatment?

If multiple boxes are checked, leasing may align better with your objectives. The purpose of this checklist is not to prescribe an answer, but to ensure the financing decision supports liquidity, control, and long-term planning.

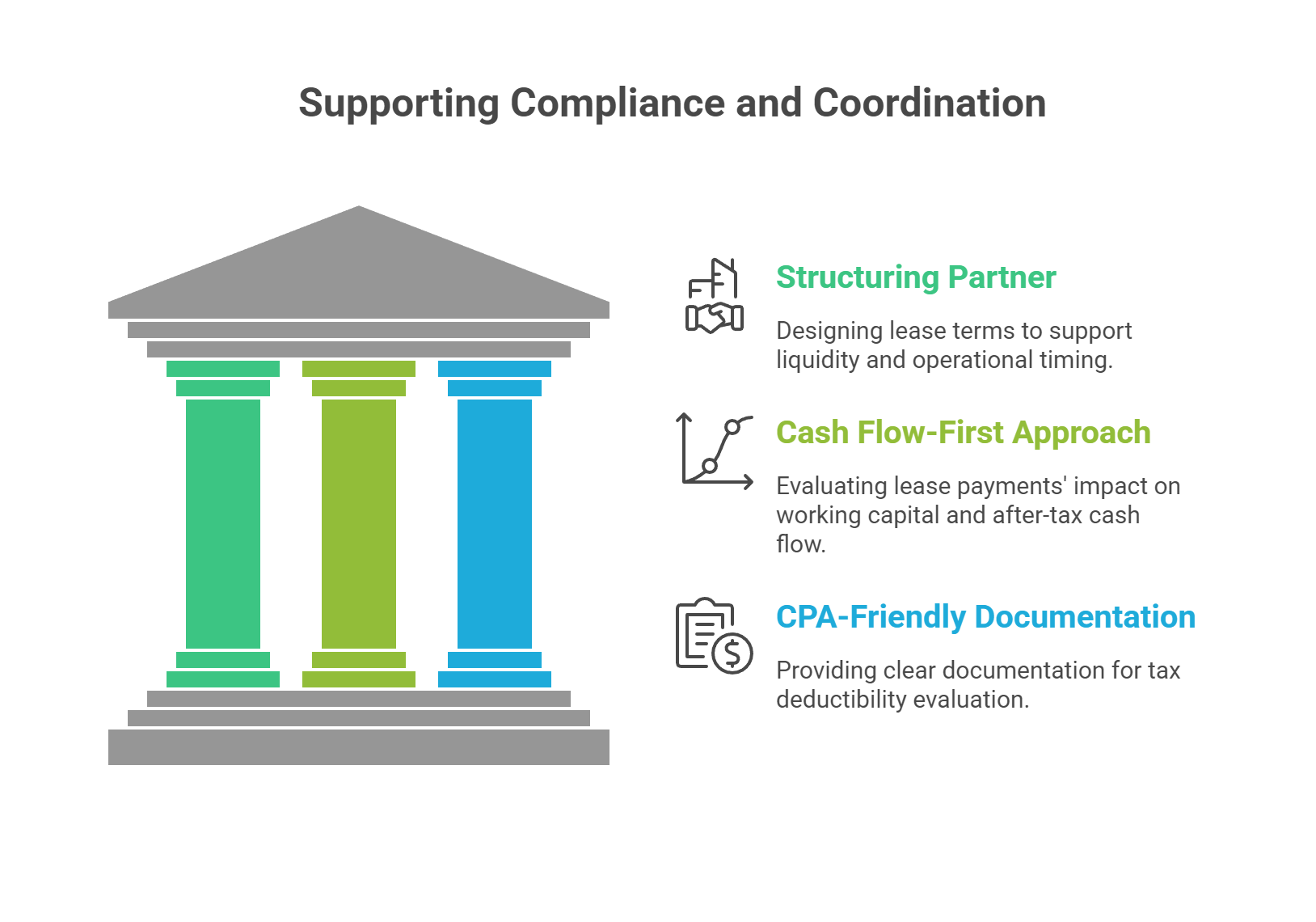

How Equipment Leases Supports Compliance and Advisor Coordination

At Equipment Leases, we view equipment financing as part of a broader capital and tax planning conversation, not a standalone transaction.

We do not provide tax advice, and we always encourage clients to review lease structures with their CPA. Our role is to structure financing in a way that makes that review clear and efficient, while supporting cash flow and long-term planning.

Here’s how Equipment Leases helps:

- We act as a structuring partner, designing lease terms that support liquidity and operational timing

- We take a cash flow-first approach, helping clients evaluate how lease payments affect working capital and after-tax cash flow

- We provide CPA-friendly documentation, making it easier to evaluate whether lease payments are tax-deductible and how operating lease tax deduction rules may apply

By aligning lease structure with business use and planning objectives, we help improve equipment leasing tax efficiency without introducing compliance risk.

The best results occur when Equipment Leases, your finance team, and your CPA are aligned from the start, ensuring the financing structure supports growth while meeting tax and reporting requirements.

Ready to Explore a Smarter Equipment Financing Structure?

If you are considering an equipment purchase, the right structure can make a meaningful difference in cash flow, liquidity, and tax efficiency.

At Equipment Leases, we help CFOs and finance teams evaluate options with clarity. Our process is designed to support informed decisions, not rushed ones.

Let’s connect:

- Request a Quote to review tailored financing options

- Contact Us to discuss your project or get questions answered

Whether you are planning an expansion, managing exposure limits, or evaluating year-end strategies, we can help you model options that align with your capital priorities and support long-term growth.