At Equipment Leases, Inc., we see this decision as a capital allocation question, not a pricing debate. The structure you choose affects liquidity, execution speed, and how much flexibility the business retains after the equipment is installed.

There is no universally correct answer. Paying cash can make sense in certain situations. Financing can be the more disciplined choice in others. What matters is aligning the structure with growth plans, timelines, and risk tolerance.

This question most often surfaces when projects are time-sensitive or when traditional banks move slowly. In practice, companies rarely regret preserving liquidity when growth is involved. They do regret decisions that restrict flexibility once the project is underway.

The Real Question Is Not Cost. It Is Control.

Interest rates and purchase price are easy to compare. Control is harder to measure, but it is what determines whether an equipment investment actually performs as planned.

Paying cash controls interest expense, but it reduces flexibility

- Capital leaves the business immediately.

- That cash is no longer available to absorb delays or unexpected needs.

- If timelines shift, the structure cannot adjust.

Financing prioritizes liquidity and execution

- Cash stays available for working capital and follow-on costs.

- Payments align more closely with when the equipment begins generating revenue.

- The business retains options as the project moves from install to operation.

Control matters most when equipment is revenue-generating.When equipment supports new capacity, new contracts, or operational scale, time-to-revenue often outweighs modest differences in financing cost.

Preserving liquidity reduces hidden risk. Upfront cash depletion can turn minor disruptions into material problems. Control means maintaining the ability to respond, adjust, and move forward without constraint.

Equipment Financing vs Cash Purchase at a Glance

Equipment projects rarely unfold exactly as planned. Installation delays, vendor timing, and scope changes are common. Structures that preserve liquidity and flexibility tend to reduce friction as the project moves from purchase to operation.

| Decision Factor | Paying Cash | Equipment Financing |

| Upfront cash impact | Full purchase price paid immediately, reducing available working capital | Minimal or no upfront cash, preserving liquidity |

| Speed to deploy | Fast if cash is readily available and vendors require no deposits | Often faster for complex projects, especially when deposits or staged payments are required |

| Flexibility during installation | Limited once cash is committed | Higher flexibility if timelines, vendors, or scope change |

| Risk isolation | Business absorbs all execution and timing risk upfront | Risk is spread over time and aligned with performance |

| Balance sheet impact | Reduces cash, no payment obligation | Creates a structured obligation, often limited to the equipment itself |

| Tax and accounting treatment | Depreciation over time, subject to tax rules | Lease payments or financing expense, structure-dependent and CPA-advised |

This table provides a high-level view. The right choice depends on how the equipment supports revenue, growth, and ongoing operations.

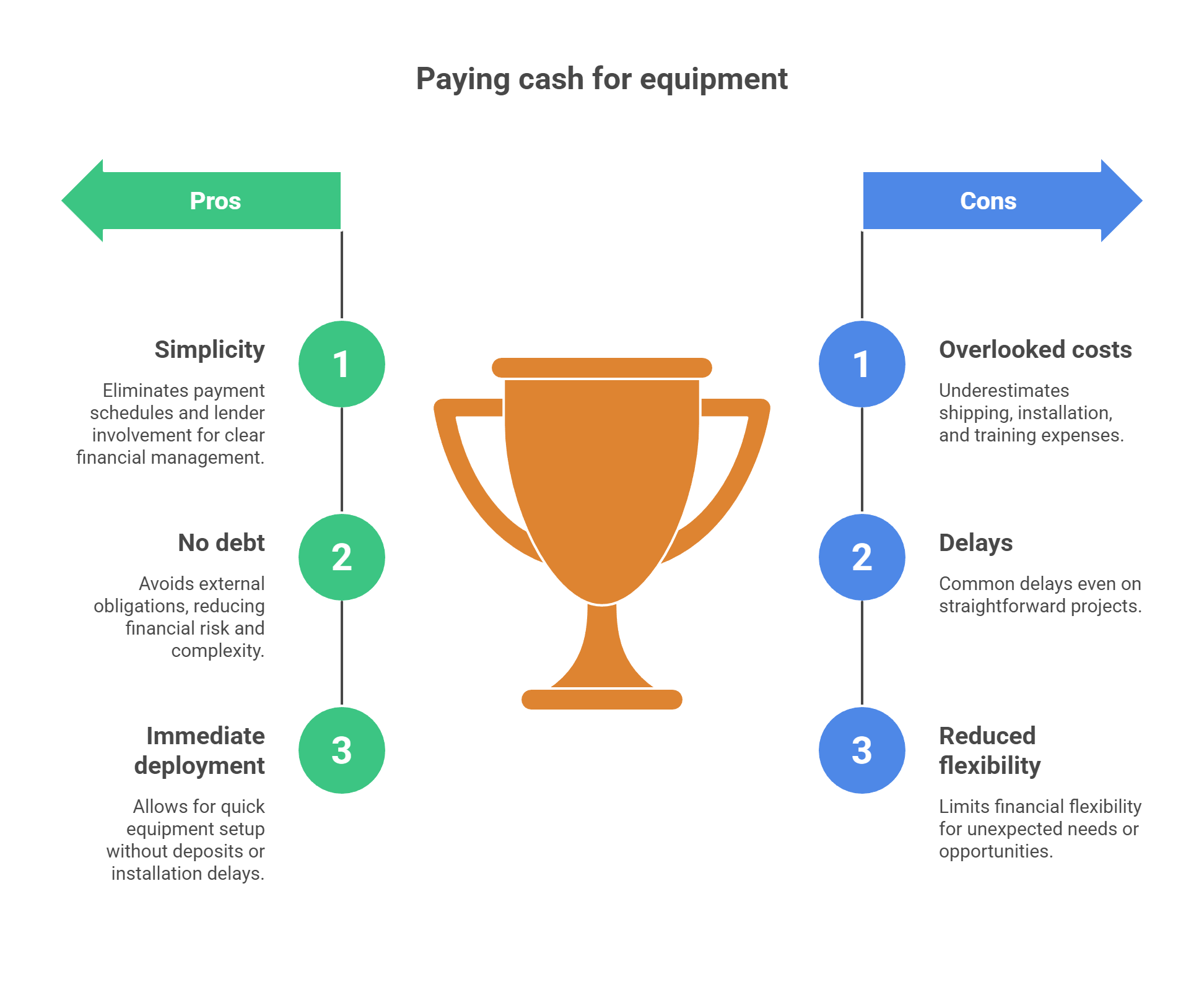

When Paying Cash for Equipment Makes Sense

Paying cash is not a mistake by default. In the right circumstances, it can be a clean and effective way to acquire equipment. The key is understanding when cash truly supports the business, and when it quietly creates constraints.

Paying cash may make sense when:

- The business has excess liquidity and no near-term growth or capital needs competing for that cash.

- The equipment is non-critical, such as a routine replacement that does not affect revenue or capacity.

- Deployment is immediate, with no deposits, staged payments, or installation risk.

- There is a strong preference to eliminate all external obligations, even at the cost of reduced flexibility.

In these scenarios, simplicity can be valuable. Cash eliminates payment schedules and lender involvement, and for some organizations that clarity is worth the tradeoff.

Where cash buyers often run into trouble

In practice, many cash purchases underestimate the full cost of execution. Shipping, installation, training, software, and downtime during changeover are often overlooked. Delays are common, even on straightforward projects. When cash is fully committed upfront, those surprises must be absorbed elsewhere in the business.

Cash works best when the project is truly contained, the timeline is short, and liquidity remains strong even after the purchase. Outside of those conditions, paying cash can introduce more risk than it appears to remove.

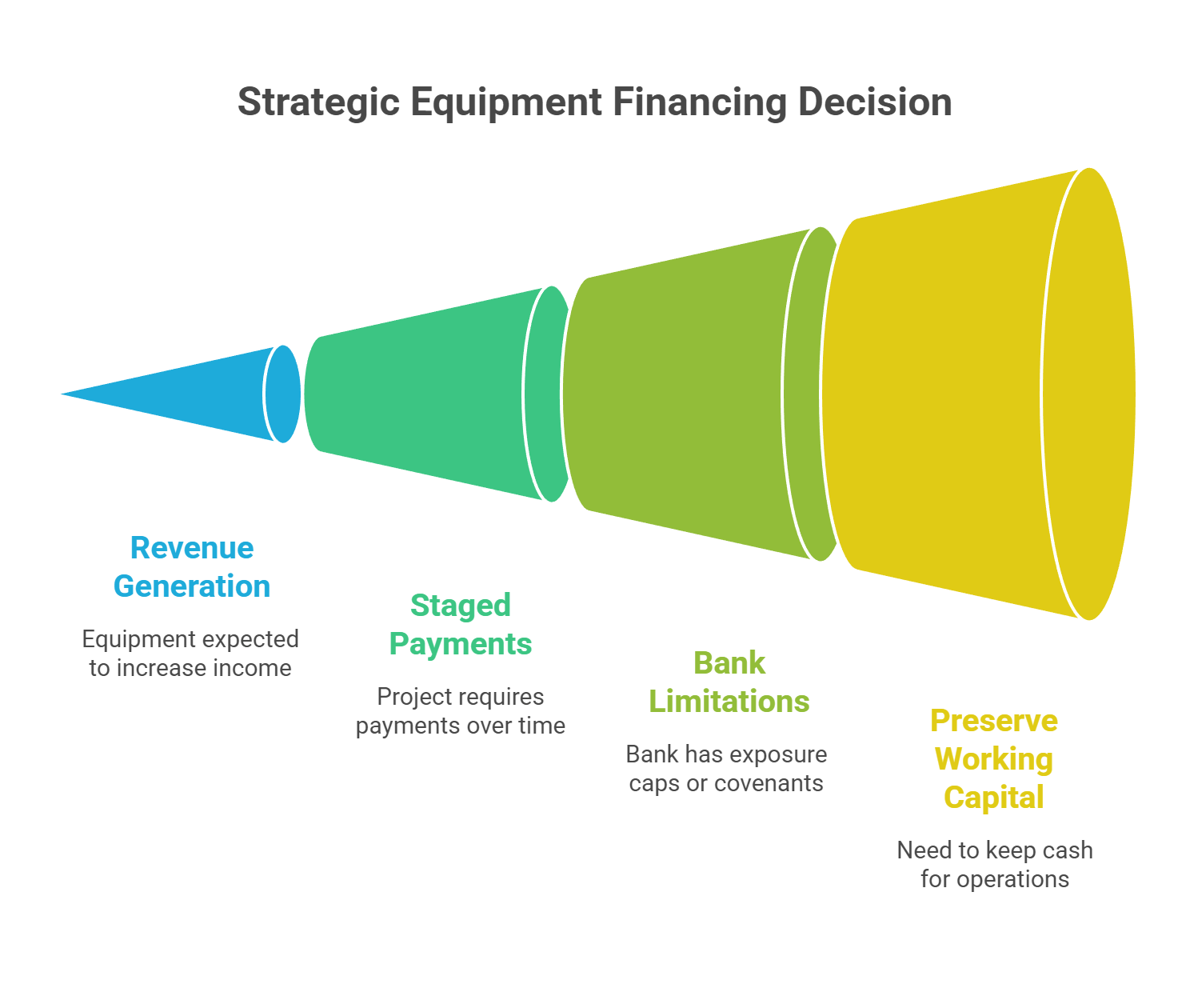

When Equipment Financing Is the More Strategic Choice

For many businesses, financing is not a fallback. It is the more controlled and practical way to fund growth.

Equipment financing is often the right choice when:

- The equipment will generate revenue or expand capacity, such as a new production line, medical system, or energy upgrade.

- The project requires deposits or staged payments, and cash is needed over time rather than all at once.

- Your bank is limited by exposure caps or covenants, even though the business is performing well.

- You want to preserve working capital for operations, payroll, inventory, or other growth priorities.

In these situations, financing allows you to move forward without draining cash before the equipment is productive. Payments are structured around how the project unfolds, from installation through ramp-up.

Why financing can be the conservative option

When financing covers the full project, including deposits, installation, and other soft costs, you avoid committing large amounts of cash upfront. That reduces pressure on the business while the equipment is still being delivered or installed.

Financing also helps isolate risk. Instead of tying up capital across the business, the obligation is connected to the equipment itself. For growth-oriented companies, this approach often provides more stability, not less.

At its core, financing is about control. It gives you the ability to execute on opportunity while keeping options open as conditions change.

The Hidden Costs of Paying Cash

Paying cash often looks clean on paper. What it hides are second-order costs that only show up once the project is underway.

Opportunity cost

When a large amount of cash is committed upfront, that capital is no longer available for other needs. If a new contract appears, inventory requirements increase, or operating costs spike, the business may be forced to delay action or seek capital under less favorable conditions.

Reduced flexibility during delays

Equipment projects rarely move exactly on schedule. Installation issues, vendor delays, or scope changes are common. When cash is fully committed at purchase, there is little room to adjust without disrupting other parts of the business.

Limited ability to respond to the unexpected

Cash-heavy purchases reduce margin for error. A temporary downturn, a customer delay, or an operational surprise can quickly turn a comfortable position into a constrained one. What initially felt conservative can become restrictive.

Vendor leverage and timeline risk

Cash does not always improve leverage with vendors, especially on complex builds. Deposits may still be required, timelines can slip, and final payments may be due before the equipment is productive. The business absorbs that timing risk entirely.

In real-world projects, cash-constrained companies are the ones most likely to pause installations, delay go-live dates, or postpone follow-on investments. These outcomes are rarely part of the original comparison, but they are often the most costly.

The hidden cost of paying cash is not the money spent. It is the flexibility lost when conditions change.

Tax and Accounting Considerations

Taxes and accounting play an important role in any equipment purchase, but they should be evaluated after the structure decision is made. In practice, tax treatment rarely changes whether a project is viable. Structure, liquidity, and execution come first.

At a high level, here is how the treatments differ:

- Paying cash generally means the equipment is capitalized and depreciated over time under current tax rules.

- Financing or leasing may allow payments to be expensed or treated differently, depending on the agreement’s structure.

Provisions such as Section 179 and bonus depreciation can accelerate deductions in certain situations. Eligibility, limits, and timing vary by year and asset type, which is why these provisions should be carefully evaluated rather than assumed.

Accounting treatment also matters Modern accounting standards require many lease obligations to be reflected on the balance sheet. The presentation depends on the structure of the agreement and internal accounting policy. Financing does not automatically mean “off balance sheet,” and cash purchases do not eliminate reporting considerations.

Why structure comes first Tax benefits rarely rescue a poorly structured deal. A project that drains liquidity, introduces timing risk, or limits flexibility can create operational strain that outweighs any tax advantage.

The most effective approach is to determine the structure that best supports cash flow, timelines, and risk management, then review the tax and accounting implications with your CPA or advisor. This keeps the decision grounded in how the business operates, not just how it is reported.

Real-World Scenarios CFOs Face

The choice between paying cash and financing rarely happens in a vacuum. It shows up inside real operating decisions, with real timelines and consequences.

These scenarios reflect how structure choices tend to play out in practice.

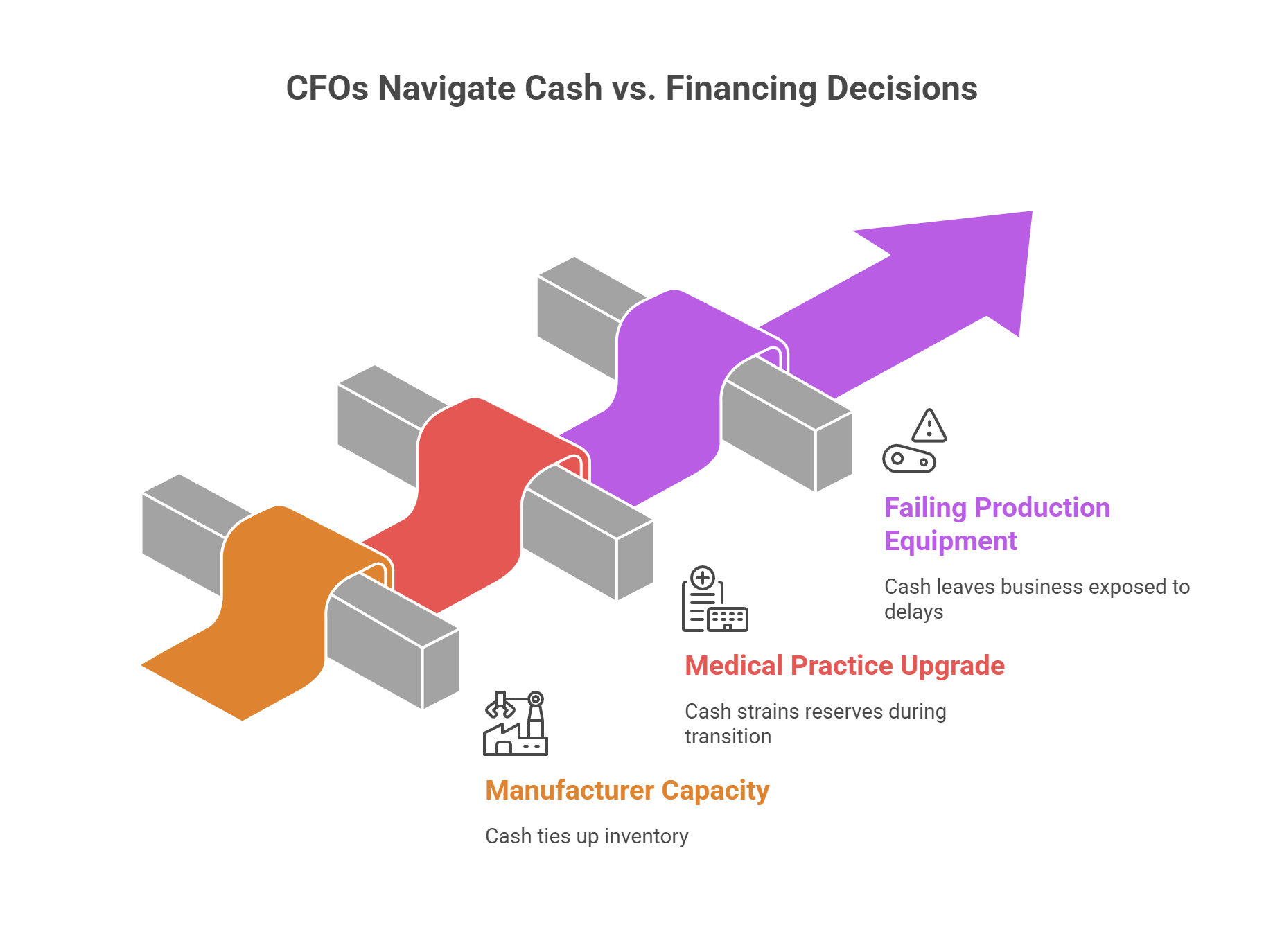

A manufacturer adding capacity under a new contract

A manufacturer wins a multi-year contract that requires additional production capacity. Paying cash would fund the equipment outright, but it would also tie up capital needed for inventory, staffing, and ramp-up costs.

Financing allows the company to install the new line, meet contract timelines, and align payments with revenue as production comes online. In this case, preserving liquidity supports execution, not leverage.

A medical practice upgrading diagnostic equipment

A practice needs to replace or upgrade diagnostic systems to maintain standards of care and throughput. Paying cash may appear simple, but it can strain reserves during installation, training, and transition.

Financing spreads the cost over time, keeps cash available for operating needs, and reduces disruption during the changeover. Structure supports continuity, not just acquisition.

An operations team replacing failing production equipment

A critical piece of equipment fails unexpectedly. Speed matters more than optimization. Paying cash can solve the immediate purchase, but it may leave the business exposed if installation takes longer than expected or other issues arise.

Financing preserves flexibility during a period of operational stress, allowing the team to focus on uptime rather than cash constraints.

Across these scenarios, the pattern is consistent. Structure changes outcomes. The right choice supports timelines, absorbs friction, and protects the business while the equipment does its job.

A CFO Checklist Before Choosing Cash or Financing

Before deciding whether to pay cash or finance equipment, it helps to step through a short, disciplined checklist. These questions surface issues that rarely appear in simple cost comparisons but often determine how smoothly a project executes.

- Liquidity impact

- How much cash will leave the business at closing?

- After the purchase, will reserves still support operations, payroll, inventory, and contingencies?

- Does preserving cash create strategic flexibility over the next 6 to 18 months?

- Time-to-revenue

- When will the equipment be installed, operational, and generating revenue or savings?

- Are payments aligned with that timeline, or is cash committed well before value is realized?

- Vendor payment requirements

- Are deposits, progress payments, or milestone payments required?

- Do installation, shipping, software, or training costs extend beyond the base purchase price?

- How will delays affect cash flow if payment is due before go-live?

- Bank exposure and covenants

- Will a cash purchase affect bank ratios, covenants, or borrowing capacity?

- Is existing credit capacity better preserved for working capital or other priorities?

- Documentation readiness

- Are financial statements current, accurate, and organized?

- Is there clear visibility into cash flow, project scope, and vendor contracts?

What underwriters look for

Underwriters focus on clarity and preparedness. Clean financials, defined project scope, and realistic timelines reduce friction and speed decisions. Ambiguity, missing documents, or last-minute changes slow everything down, regardless of whether cash or financing is used.

Why preparedness matters

Well-prepared companies move faster and retain more control. When information is ready, options stay open and decisions remain proactive rather than reactive.

This checklist is not about choosing a side. It is about choosing a structure that supports execution, protects liquidity, and aligns with how the business actually operates.

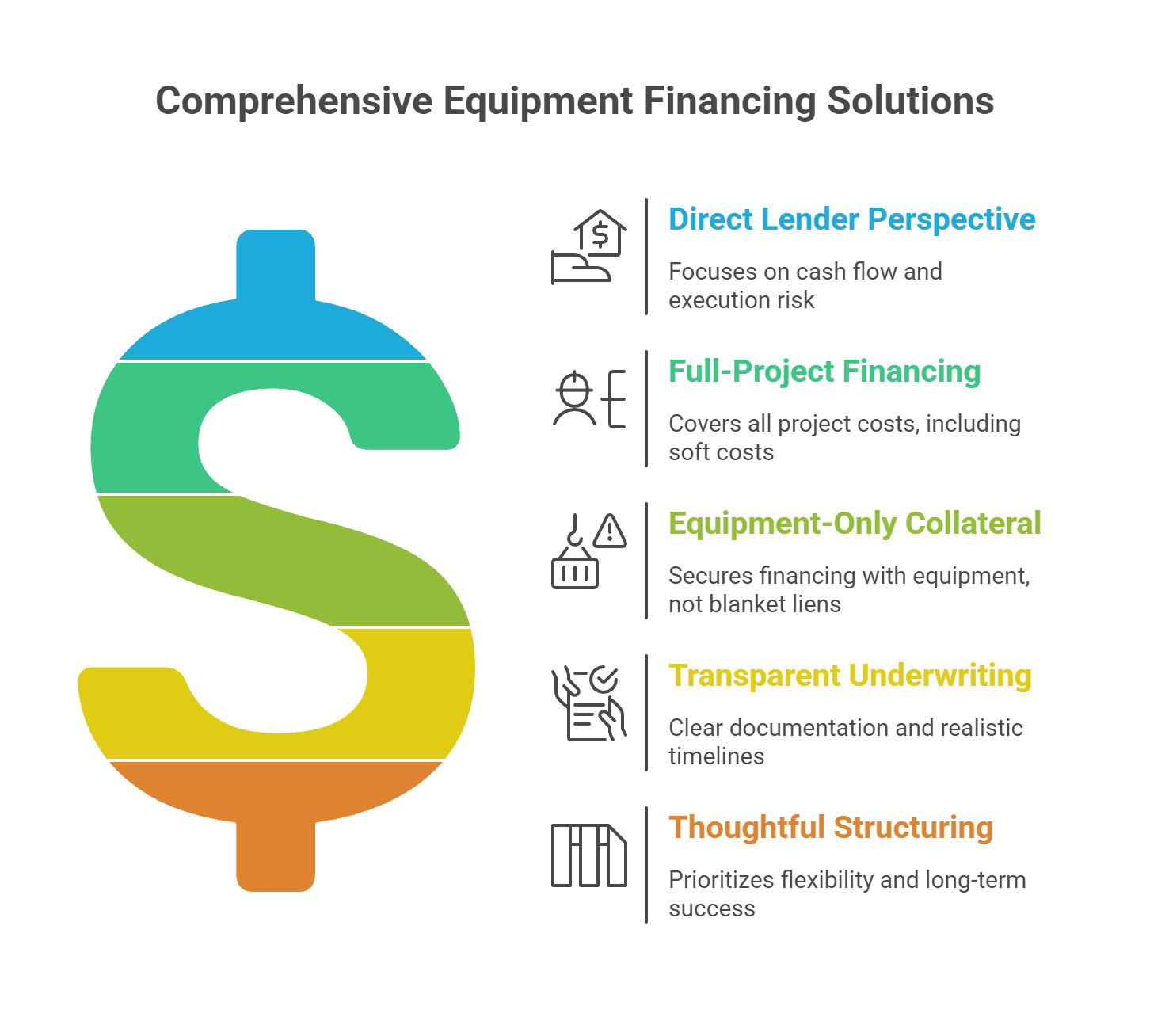

How We Help Companies Structure Equipment Financing Thoughtfully

When companies explore financing, they are not just looking for capital. They are looking for clarity, predictability, and a structure that supports how the project will actually unfold.

That is where Equipment Leases, Inc. focuses its role.

A direct lender perspective

We operate with a direct lender mindset. Projects are evaluated based on cash flow, timelines, and execution risk, not just the equipment itself. This allows structures to reflect how the business operates in the real world and supports faster, more informed decisions.

Full-project financing

Many equipment purchases involve more than a single invoice. Deposits, installation, shipping, software, and other soft costs are often part of the project. We help structure financing around the full scope, so cash is preserved and surprises are minimized as the project progresses.

Equipment-only collateral

Financing is typically secured by the equipment itself, rather than blanket liens across the business. This helps isolate risk, protect working capital, and complement existing bank relationships rather than complicate them.

Transparent underwriting and timelines

Clear documentation requirements and realistic timelines are established upfront. This transparency reduces friction, keeps expectations aligned, and helps projects move forward without unnecessary delays.

Why structure matters more than speed alone

Fast approvals are valuable, but only when the structure holds up under real operating conditions. Equipment Leases, Inc. prioritizes thoughtful structuring so companies maintain flexibility during installation, adapt to change, and retain control from purchase through operation.

The goal is not simply to fund a transaction. It is to support execution in a way that protects the business and sets the project up for long-term success.

Next Steps

Choosing between paying cash and financing equipment is rarely a one-size-fits-all decision. The right approach depends on timelines, liquidity, and how the project fits into broader operating and growth plans.

If you are weighing options, the most productive next step is a structured conversation.

Let’s connect:

- Request a Quote for a tailored financing solution

- Contact Us to discuss your project or get your questions answered

- Learn how our lender referral program works.

Walking through the project details, payment requirements, and cash flow implications often brings clarity quickly and helps avoid surprises later.