Yes, you can claim bonus depreciation on financed equipment. Under the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, 100% bonus depreciation is back for qualifying assets placed in service after January 19, 2025.

But the quick answer isn’t the complete answer.

The structure of your financing determines whether your business captures the deduction, or whether your lender does. For a company investing $1 million in equipment, getting that structure right can represent $210,000 in first-year tax savings at a 21% corporate rate. Your CPA can confirm what that means for your specific situation.

Bonus Depreciation Is Back — Here’s Where Things Stand

If you’ve seen content suggesting bonus depreciation was headed toward zero, that information is out of date.

Before the One Big Beautiful Bill Act, businesses were looking at a phase-down schedule: 60% in 2024, 40% in 2025, and a full sunset by 2027.

The OBBBA changed that. Signed July 4, 2025, it permanently restored 100% bonus depreciation for qualifying property placed in service after January 19, 2025.

The OBBBA also raised Section 179 limits. The deduction cap increased to $2.5 million, with phase-out beginning at $4 million in total qualifying purchases.

A few things to confirm with your CPA before you proceed:

- Qualifying assets include new or used equipment that is new to your business, with a useful life of 20 years or less, placed in service during the tax year

- IRS rules require Section 179 to be applied first, with bonus depreciation applied to the remaining basis

- Eligibility depends on your asset type, entity structure, and specific tax situation

The policy environment is favorable right now. The more important question is how your financing structure affects whether you actually capture the benefit and that’s where most businesses need a clearer picture.

Your Financing Structure Determines Who Gets the Deduction

Here’s the rule most financing conversations skip. To claim bonus depreciation, your business must be treated as the owner of the equipment for tax purposes. The structure of your financing determines whether that’s you or your lender.

Three structures. Three different outcomes.

Dollar-Out Capital Lease

Your business is treated as the owner from day one. Payments are higher than an FMV lease, but when the term ends, the equipment is yours for a dollar. Because ownership transfers to you, the full equipment cost may be eligible for bonus depreciation and Section 179.

If maximizing your first-year deduction is the priority, this is typically the right starting point. Confirm the treatment with your CPA before you proceed.

Operating Lease

The lender retains ownership throughout the lease term. At the end, you can either purchase the equipment at its fair market value, return it, or renew. Because your business is the lessee, not the owner, you cannot claim depreciation. The lender claims it.

The tradeoff: your monthly payments are lower, and lease payments may be fully deductible as a business expense. Some lenders pass their depreciation benefit through in the form of reduced payments. This structure is often the right fit for companies prioritizing lower monthly costs, off-balance-sheet treatment, or payment flexibility over a first-year deduction.

Loan / Direct Financing

A direct loan gives your business full ownership from day one, thereby maximizing depreciation eligibility. For companies with the cash position to support a down payment and a clear preference for asset ownership, this is a straightforward path to the full deduction.

The right structure depends on your tax situation, balance sheet goals, and cash position. Your CPA and your financing partner should be working through that decision together, not in separate conversations.

Equipment Leases offers all three structures. We help you identify the right fit alongside your tax advisor, and we can move quickly once the structure is confirmed.

100% Financing Plus Full Deduction — Why This Combination Changes the Math

Most businesses assume they have to choose between deploying cash to buy the equipment and capture the deduction, or finance it and give something up. That’s not the choice when you’re working with the right lender.

Why Most Financing Structures Leave Cash on the Table

Banks typically require a significant down payment before they’ll fund an equipment purchase. That upfront cash outlay reduces your working capital before you’ve seen a dollar of tax benefit. Add blanket lien requirements and exposure limits, and banks create friction at exactly the wrong moment.

The Equipment Leases Difference

We fund 100% of the project, not just the equipment cost, but:

- Shipping and installation

- Software and integration

- Warranties and soft costs

The entire qualifying project cost may be eligible for depreciation. You preserve your cash and still take the deduction.

On a $2 million dollar-out lease, your business may be able to claim 100% bonus depreciation on the full $2 million while keeping 100% of its cash in place. For companies making large-scale investments from $500K into the $100M range, this combination is a strategic advantage most banks structurally can’t match.

Your CPA can confirm the treatment for your specific structure and entity type.

In Practice

We funded a $9 million equipment upgrade for a Florida manufacturer that was technically unbankable after a difficult period. Full project financing. No money out of pocket. New equipment, new contracts, and a business back on a growth track. The tax strategy was their CPA’s work. Our job was making sure the capital was there to support it.

Finance the full amount. Keep your capital working. And still take the deduction.

Progress Funding Lets You Finance Complex Builds Without Missing the Year-End Window

For companies managing complex, multi-phase equipment builds, the financing timeline and the tax timeline are the same conversation. If equipment isn’t placed in service before December 31, the current-year deduction doesn’t apply, regardless of how far along the project is.

That’s where progress funding changes the picture.

What Progress Funding Actually Does

Progress funding allows us to deploy capital as your project moves forward, not after it’s complete. We fund each phase as it happens:

- Initial vendor deposits

- Milestone payments throughout the build

- International vendor invoices, including overseas deposits in euros

- Final installation and delivery

Your cash stays in place at every stage. The project keeps moving. And the equipment goes into service on a timeline that works for your business and your tax year.

Why This Matters for Large Builds

Most traditional financing requires the asset to be complete before funds are released, which means businesses carry the cash burden of deposits and milestone payments themselves, sometimes for months. For a $5 million equipment build requiring a 25% deposit upfront, that’s $1.25 million out of pocket before a single piece of equipment is in service.

Progress funding eliminates that burden. We handle those payments directly so you don’t have to.

The Tax Planning Connection

When equipment is placed in service before December 31, your business may be able to capture the full-year bonus depreciation benefit for that phase of the project. For companies running staged installations or multi-phase builds, how the funding is structured and timed determines whether that window stays open.

This is particularly relevant for manufacturers, pharmaceutical companies, and energy operations where custom builds, long lead times, and multi-vendor projects are the norm, not the exception.

Talk to your CPA about how placement-in-service timing applies to your specific project and structure.

Timing Matters — Same-Day Decisions for Year-End Tax Planning

The bonus depreciation benefit is tied to one hard deadline: equipment placed in service by December 31. The financing decision has to happen well before that. A lender that can’t move quickly isn’t just inconvenient, it’s a liability when the tax calendar is driving the timeline.

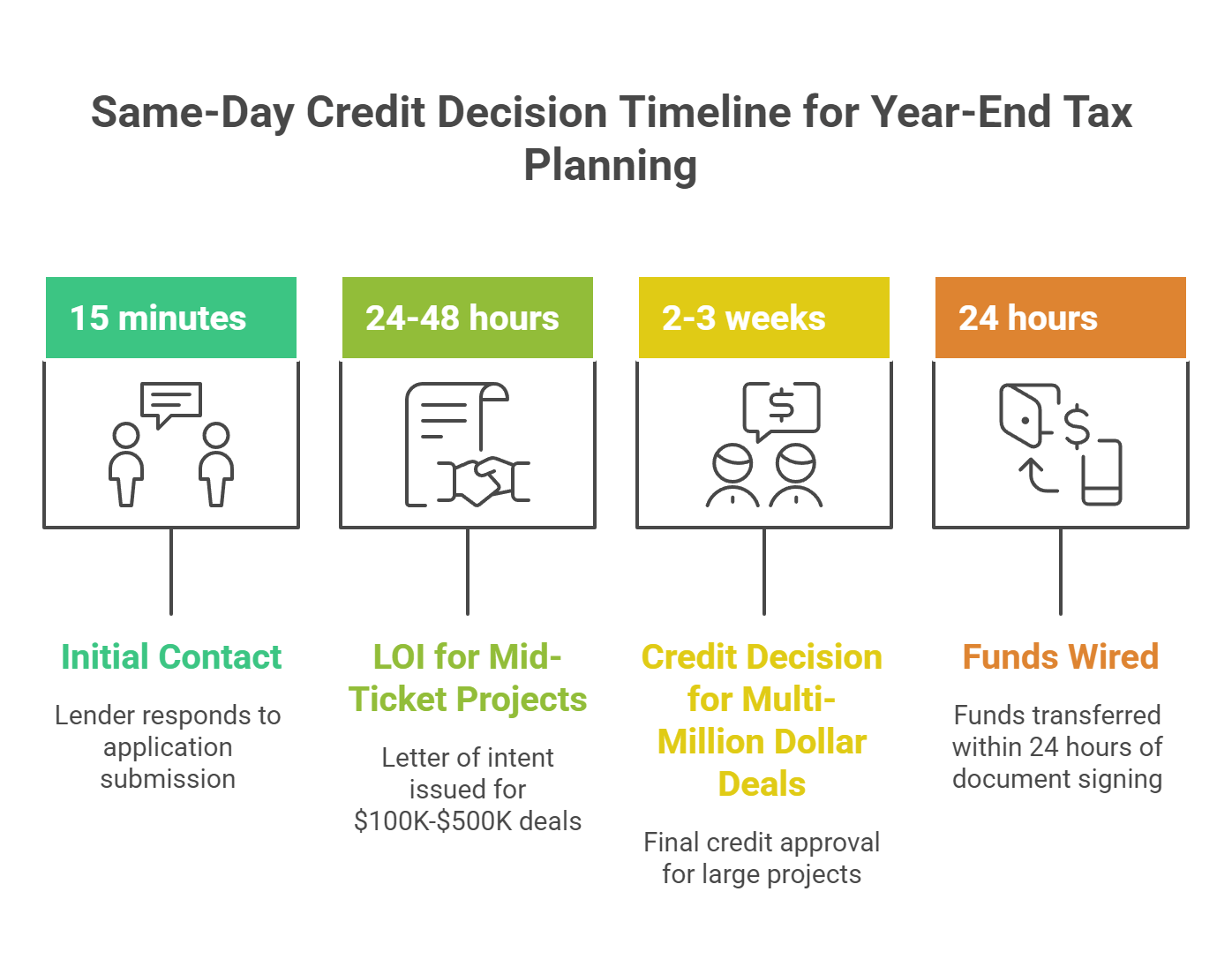

How Our Credit Process Works

Our credit committee is small by design, three to four senior decision-makers with the authority to move. When a borrower comes in prepared, we can deliver a same-day credit decision. Here’s what the timeline looks like:

- Initial contact: Within 15 minutes of application submission

- LOI for mid-ticket projects ($100K-$500K): Typically 24-48 hours

- Credit decision for multi-million dollar deals: Typically 2-3 weeks

- Funds wired: Within 24 hours of final documents

We’ve delivered same-day approvals for manufacturers who needed equipment in service immediately. That capability exists because of how the committee is structured, not in spite of deal complexity.

What Prepared Looks Like

Our timelines are preparation-dependent. The fastest path to a credit decision requires:

- A completed application with accurate business information

- Recent financial statements

- Equipment invoice or vendor quote

Our team will walk you through the full checklist upfront. No surprises, no unnecessary back-and-forth.

We Work Alongside Your Bank — Not Around It

We’re bank-complementary. That means we’re designed to work alongside the banking relationship you’ve already built, not compete with it or replace it.

What That Looks Like in Practice

If you’ve reached your bank’s exposure limit, we can step in without disrupting the relationship. If a covenant restricts additional debt, an operating lease structure may allow equipment to be financed off the balance sheet, which can reduce the risk of triggering those restrictions. Confirm the specific treatment with your CPA and banking partner before proceeding.

Because our collateral is limited to the equipment itself, we do not place liens on your receivables, real estate, or broader business assets. Your existing credit lines remain intact.

We want to be your first call. If we can’t do a deal, we’ll tell you who can.

Why This Matters in a Tax Planning Context

If your bank can’t move fast enough, can’t fund the full project cost, or can’t offer a structure that preserves your deduction eligibility, the bonus depreciation window can close, even when the opportunity is strong.

Bank-complementary financing allows you to protect your banking relationship while still capturing the potential tax benefit.

We Helped Advocate for This Policy — Now We Help You Benefit From It

When you work with Equipment Leases, you’re working with a team that doesn’t just understand the financing landscape, we’ve helped shape it.

Buddy Zarbock, CEO of Commercial Funding Partners, serves on the Equipment Leasing and Finance Association’s Capital Connections Political Action Committee. Every year, that committee travels to Washington D.C. to meet directly with members of Congress and senators about policies that affect how U.S. businesses invest, grow, and access capital.

Bonus depreciation was one of those conversations.

“Our political action work in Washington, D.C., helped advocate for business-friendly policies like the continuation of bonus depreciation. I’m proud to have been part of that effort.” – Buddy Zarbock

The 100% bonus depreciation you can take advantage of today didn’t happen by accident. We were part of the work that helped get it there. That’s the level of industry engagement and commitment you get when you bring us into your financing conversation.

One More Thing Before You Move Forward

Our job is to structure your financing. Your CPA’s job is to optimize your tax outcome. When those two conversations happen together, you capture the full benefit of both.

Before you proceed, confirm how current bonus depreciation rules apply to your specific assets, entity structure, and tax situation with a qualified CPA or tax advisor. We’ll make sure the capital is structured and ready when you need it.

Ready to Put This to Work?

The right financing structure determines whether you capture the bonus depreciation benefit or leave it on the table. We’re here to make sure your capital is in place, structured correctly, and moving on your timeline.

Apply for Equipment Financing

Start with a seven-minute application. Our team will be in touch within 15 minutes.

Talk to Our Team About Your Financing Structure

Not ready to apply yet? Let’s talk through your options FMV lease, dollar-out lease, or direct financing, before you commit.

See How Our Lease Structures Compare

Understand how each structure affects your tax position, balance sheet, and monthly payments before you decide.

Planning a capital equipment purchase before year-end? Let’s talk about timing.