Equipment Leasing for Private Debt Financing Groups

Equipment Financing for the Companies You Work With

Private debt funds work with companies that need equipment. When those companies need to finance CAPEX, Equipment Leases handles it directly. Fast underwriting, equipment-only collateral, no interference with existing credit arrangements.

When the companies you work with need equipment financing, Equipment Leases is where you send them.

We don’t participate in your fund’s transactions or take a position in your deals. Our role is to finance the equipment, and we get out of the way.

Our platform provides curated origination opportunities across middle-market borrowers seeking growth capital without overleveraging enterprise debt.

Equipment Leases is the origination platform of Commercial Funding Partners, a direct lender founded in 2012 with syndication relationships across private equity groups, family offices, banks, and credit unions. We underwrite our own deals. When transaction size warrants it, we bring in capital partners who trust our credit process. That model gives us the capacity to handle transactions from $250K to $200M+ per project without the delays that come with routing deals through third-party approval.

Credit decisions are led by Traci Dolphin, President, with 34 years in credit and finance and over a decade in equipment leasing. Our Chief Credit Officer, Terry Lutz, is a 25-year veteran of commercial finance who leads a senior credit committee that reviews every transaction, ensuring approvals move quickly without sacrificing discipline.

Why Private Debt Funds Work With Us

- Direct lender with deal capacity from $250K to $200M+ per project

- Dedicated senior credit committee for private capital projects, decisions in days, not weeks

- BBB A+ rated | 13+ years in business

- Over 40% repeat client rate — the clearest measure of a performing portfolio

- Active member of ELFA, NEFA, AACFB, and CLBA

How We Support Private Debt Fund Borrowers

Private debt funds work with middle-market companies that often have significant equipment CAPEX requirements, alongside the enterprise credit the funds provide. When those companies need equipment financing to expand capacity, replace critical assets, or manage a staged build, Equipment Leases steps in as a direct lender.

We don’t participate in your fund’s deals or take a position in your transactions. Our role is to finance equipment for the businesses you work with, cleanly and quickly, so your borrowers can preserve their credit lines and your fund can stay focused on its core strategy.

Finance Offerings Available for Your Borrowers

Equipment Financing and Leasing - Flexible structures to compliment the clients cash flow models and future projections

We finance new and used equipment across manufacturing, medical, construction, pharmaceutical, energy, food processing, transportation, and other equipment-intensive industries.

Borrowers get 100% project financing with equipment-only collateral, no blanket liens on company assets or receivables.

- Financing range: $250K to $200M+ per project

- Lease terms: 12–60 months, up to 72 months for select transactions

- FMV leases and dollar-out leases available

- Equipment-only collateral does not displace or compete with existing enterprise credit

- New and used equipment both eligible

- Progress Funding for Staged Builds

For companies undertaking multi-phase equipment installations, we manage milestone payments and vendor deposits directly, including international vendors. This eliminates the need for borrowers to tie up working capital during the build period.

- Down payment and milestone invoice coverage handled directly with vendors

- International vendor deposits supported, including payments in foreign currency

- No large upfront cash requirement for the borrower

- Payment timing aligned to project milestones

Sale-Leaseback - up to $200M+ for quality new or used equipment. Clients keeps the equipment in production we provide the cash infusion

If a portfolio company owns productive equipment outright, we can purchase and lease it back, converting embedded equity into immediate working capital without disrupting operations.

- Turns owned equipment into liquidity without operational disruption

- Borrower retains full use of the asset

- Useful for companies approaching bank exposure limits or needing capital for acquisitions

Bank-Complementary Structures - complex financing structures are our specialty without impact on current credit facilities

Many middle-market companies have existing banking relationships that have hit exposure limits or won’t cover certain equipment types. We work alongside those relationships, not against them.

- Supports borrowers who have reached bank exposure limits

- Operating lease and tax-advantaged structures available

- Does not compete with or displace existing bank credit facilities

- Handles equipment types banks often won’t, specialized machinery, non-standard assets, and certain industry-specific equipment

Why Private Debt Funds Refer Borrowers to Equipment Leases

When a portfolio company or borrower has an equipment CAPEX need, referring it to Equipment Leases means the fund doesn’t need to absorb it, restructure around it, or watch it stall. We take it from there.

- Contact within 15 minutes of application submission to understand the project completely

- Our dedicated Private Capital desk meets to create the doc files and prepare the project for underwriting.

- LOI delivered within 24–48 hours for projects up to $5,000,000. 5-7 days for complex multi-million dollar deals above $10M

- Direct lender model, no third-party bank approval required, no routing delays

- Handles difficult structures banks won’t touch: progress-funded builds, non-standard equipment, companies at exposure limits

- Equipment-only collateral protects the borrower’s broader credit position

- Master lease structures make future equipment additions simple, one master agreement, easy add-ons

- We protect the borrower relationship. We work to get deals done, not to find reasons to decline.

Not sure which approach fits your portfolio companies’ needs? Contact us to discuss how we can support your borrowers.

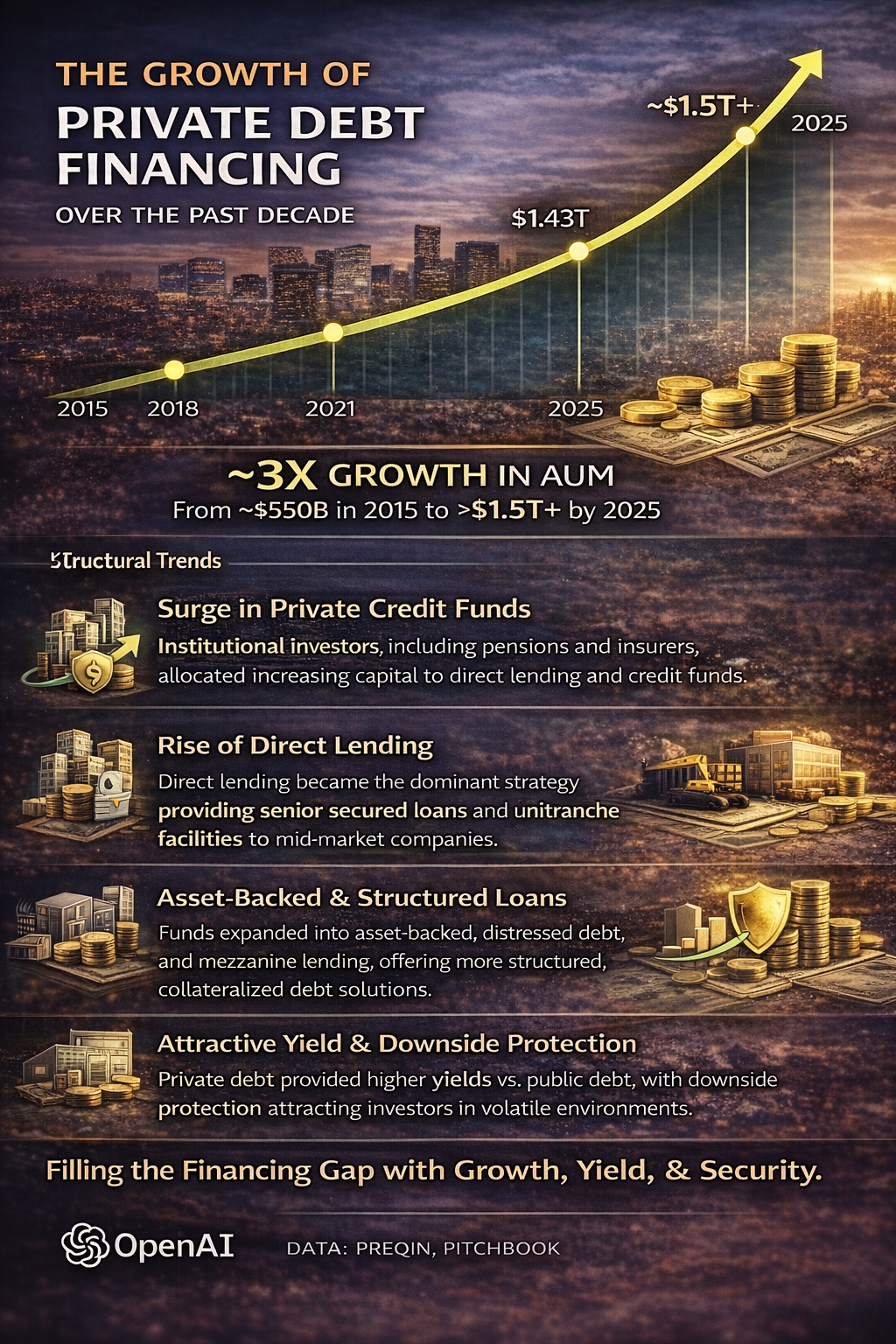

Private Debt Financing has exploded over the past 10 years, and so has our lending involvement in this niche.

The growth of private debt over the past decade has created a structural demand for asset-backed origination at scale. Middle-market direct lending has become increasingly competitive, compressing yields and raising covenant complexity. Equipment leasing sits within this landscape as a specialty finance allocation that delivers what traditional direct lending increasingly cannot: tangible collateral, shorter duration, and access to borrowers that most institutional platforms don’t reach.

Steady Expansion of Private Debt AUM

- Private debt has experienced substantial growth as institutional investors (pension funds, insurance companies, endowments) allocate more capital to direct lending and credit strategies outside the syndicated bank market.

- In 2015, the global private debt market was estimated at roughly $500 billion–$600 billion in assets under management (AUM).

- By 2025, private debt AUM is projected to exceed $1.5 trillion, representing ~3x growth over the past decade. This growth reflects a structural shift as banks retrench from mid-market lending and demand for non-bank lending rises.

- This 3x growth means thousands of portfolio managers seeking asset-backed deployment opportunities. Equipment financing with its tangible collateral and predictable amortization has become an increasingly attractive allocation within institutional private debt portfolios.

Drivers of Growth

- Bank Regulatory Retrenchment (Post-2008/2010 Regulations)

Stricter capital and lending requirements for traditional banks have reduced their appetite for mid-market loans, allowing private debt funds to fill the gap. - Institutional Investor Demand

Pension funds, endowments, and insurers seeking yield and income have increased allocations to private debt, attracted by higher returns than those of public fixed income. - Rise of Direct Lending

Direct lending has become the dominant strategy within private debt, providing senior secured loans and asset-backed structures for middle-market sponsors. - Diversification and Downside Protection

Private debt’s senior, secured positions provide downside protection and stable cash flow, appealing in volatile macroeconomic environments such as rising rates.

Summary: Private Debt Growth (2015–2025)

- 3x increase in AUM from mid-$500B to over $1.5T+ globally

- Increased role in middle market financing, replacing traditional bank credit

- Attractive yield vs. public markets, especially in rising-rate environments

- Growth in asset-backed and structured credit strategies

- Bank retrenchment has opened a middle-market equipment financing gap

- Institutional capital flowing into specialty finance strategies

- Equipment leasing provides an asset-backed alternative to traditional direct lending

- Enhanced yields available in less competitive market segments

- Strong collateral coverage appeals to risk-conscious allocators

Key Structural Trends

- Asset-Backed Focus: Lenders increasingly favor deals backed by tangible collateral (equipment, receivables, real estate), improving loss severity profiles.

- Equipment leasing epitomizes this trend: senior secured positions in identifiable assets with independent market value, providing enhanced recovery profiles and reduced loss severity relative to unsecured lending.

- Broad Strategy Expansion: Beyond direct lending, private debt has expanded into mezzanine, distressed credit, special situations, and equipment/asset-based lending.

- Higher Allocations from Institutional Investors: By the mid-2020s, many institutional portfolios targeted private debt allocations of 8%–12% or higher.

Private Debt in Practice

Case Study 1 - Private Debt Fund Deploys Senior-Secured Capital Through Equipment Leasing to Enhance Yield

Private Debt Investor Profile

Investor Type: Private Debt Financing Group

Investment Strategy: Senior secured private credit

Target Borrowers: Middle-market manufacturing and industrial companies

The Challenge

Private debt funds sought to deploy capital into secured transactions with predictable cash flow and tangible collateral. Traditional senior loans were becoming increasingly competitive, compressing yields and increasing covenant complexity.

The fund needed an alternative that provided strong asset protection, shorter durations, and scalable deployment without increasing enterprise-level credit risk.

The Equipment Leases Solution

The fund partnered with Equipment Leases to deploy $8.6 million in senior-secured equipment leasing transactions across multiple middle-market borrowers.

Equipment Leases structured transactions that featured:

- First-priority liens on equipment

- Predictable amortization schedules

- Conservative advance rates based on asset value

- Diversification across manufacturing and industrial sectors

Equipment Leases served as the origination and execution platform, allowing the fund to deploy capital efficiently while maintaining underwriting discipline.

The Results

- Enhanced yield relative to traditional senior loans

- Strong collateral coverage with clearly identifiable assets

- Reduced exposure to enterprise-level credit risk

- Consistent monthly cash flow

Private Debt Investors Benefit With Equipment Leases

Equipment Leases provided a scalable, asset-backed strategy that balanced yield and capital preservation.

Case Study 2 - Private Credit Fund Uses Equipment Leasing to Scale Origination Without Expanding Risk

Private Debt Investor Profile

Private Credit / Direct Lending Fund

Investment Strategy: Middle-market private debt

Primary Objective: Scalable deployment with downside protection

The Challenge

The fund sought to increase capital deployment while maintaining strict risk parameters. Building internal origination infrastructure would have increased overhead and slowed deployment, while traditional deal flow lacked sufficient asset-level protection.

The fund needed a consistent sourcing channel for secured transactions that aligned with portfolio construction goals.

The Equipment Leases Solution

Equipment Leases served as the fund’s outsourced equipment-leasing arm, sourcing and structuring $12.3 million in equipment-backed transactions tied to revenue-producing assets.

Key structuring elements included:

- Equipment-specific underwriting

- Senior secured collateral positions

- Defined amortization and exit paths

- Flexible tranche deployment

Equipment Leases enabled the fund to scale origination while maintaining portfolio discipline.

The Results

- $12.3M deployed across diversified borrowers and industries

- Improved capital deployment velocity

- Maintained conservative risk profile

- Strengthened portfolio yield and stability

Private Debt Takeaway

By partnering with Equipment Leases, the fund expanded origination capacity without sacrificing credit quality or risk control.

Underwriting Standards and Risk Management

When a private debt fund refers a borrower to Equipment Leases, the fund needs confidence that the underwriting is disciplined and the process won’t create problems for an existing lending relationship. Here is how we evaluate every transaction.

Credit decisions are led by Traci Dolphin, President, with over 34 years of credit and finance experience. Every transaction is reviewed by a 3–4 person senior credit committee before approval.

Equipment Lease Underwriting Framework

Equipment Value and Marketability

Every transaction begins with asset validation. Equipment is the primary collateral, and underwriting reflects redeployment realities rather than theoretical enterprise value.

- Independent equipment appraisals from certified professionals (when appropriate)

- Secondary market liquidity assessment

- Useful life analysis relative to the lease term

- Technology obsolescence risk evaluation

- Residual value projections

Advance rates are adjusted based on liquidity, resale depth, and equipment essentiality.

Borrower Credit Assessment

Asset-backed discipline does not replace borrower analysis. Both must align.

- Business financial statement analysis

- Cash flow review and debt service capacity

- Industry stability and economic sensitivity

- Operating history (prefer 2+ years; select startups considered with strong model and sponsor support)

- Management experience and operational depth

Cash flow coverage target: minimum 1.25x–1.50x debt service coverage, depending on credit profile and structure.

How Equipment Financing Fits Your Fund’s Strategy

Private debt funds provide enterprise-level credit to middle-market companies such as revolving facilities, term loans, acquisition financing, and structured capital. Equipment CAPEX is a different problem. It’s asset-specific, collateral-driven, and often sits outside what the fund’s mandate is designed to handle cleanly.

Equipment Leases fills that gap. We finance the equipment; your fund handles the enterprise credit. The two don’t compete.

Where Equipment Financing Sits

Equipment CAPEX needs arise at every stage of a portfolio company’s lifecycle such as expansion, replacement, acquisition-related build-outs, and cash preservation during growth phases. In many cases, the company’s bank or primary lender is already at exposure limits, can’t move fast enough, or won’t finance that specific equipment type.

That’s where a referral to Equipment Leases solves the problem without creating a new one. We use equipment-only collateral with no blanket liens, no displacement of existing credit arrangements, no covenant complications.

The Practical Fit

- Equipment financing is asset-specific: it doesn’t require a view on the borrower’s enterprise value or overall creditworthiness in the way enterprise lending does. The collateral is the equipment itself.

- It’s shorter duration (24–60 months): the borrower’s equipment obligation is resolved and off the table well before most fund-level credit facilities mature.

- It’s operationally clean: monthly payments, defined term, equipment-only lien. No surprises that complicate the fund’s existing credit arrangements.

- It preserves the borrower’s cash position: which directly supports the borrower’s ability to service the fund’s own credit.

When portfolio companies can get their equipment financed quickly and correctly, they grow faster, operate with less cash strain, and are better credit risks across the board.

What Changes for Your Borrowers

Without Equipment Leases | With Equipment Leases |

|---|---|

Borrower ties up cash on equipment CAPEX | 100% financed; cash preserved for operations |

Bank at exposure limit; deal stalls | Equipment Leases funds it independently |

Progress-funded build requires upfront vendor deposits | We handle vendor payments directly |

Owned equipment is illiquid capital | Sale-leaseback converts it to working capital |

Fund absorbs equipment credit or watches deal die | Fund stays focused; we handle the equipment piece |

Frequently Asked Questions from Private Debt Funds

What types of borrowers do you work with?

We work with U.S.-based businesses across manufacturing, medical, construction, pharmaceutical, energy, food processing, transportation, and other equipment-intensive industries. We handle both bankable credits and companies that have reached bank exposure limits or need financing structures their bank won’t provide. What drives our decision is the quality of the underlying equipment and the borrower’s ability to service the obligation, not a rigid credit score threshold.

What deal sizes do you handle?

We finance transactions from $250K to $200M+ per project. Our average transaction is approximately $2 million. For larger or more complex deals, our direct lending capacity and syndication network, private equity groups, family offices, banks, and credit unions which allow us to scale without routing delays.

Do you compete with the fund’s existing financing arrangements?

No. We use equipment-only collateral. We don’t take blanket liens, don’t compete with revolving credit facilities or enterprise loans, and don’t create covenant complications. In many cases we help borrowers stay within existing bank covenants by keeping equipment off the bank’s balance sheet entirely. We are designed to work alongside existing credit relationships, not displace them.

What if the borrower already has a relationship with their bank?

That’s often exactly why they come to us. Banks frequently hit exposure limits on great clients, or decline to finance certain equipment types, or simply can’t move fast enough. We work in parallel with those relationships. We’ve been referred deals by major banks because the bank wanted to protect a long-standing client relationship but couldn’t underwrite the specific transaction. We get it done without threatening what the bank and client have built.

What happens if a referred borrower defaults?

We manage the default process entirely, it doesn’t come back to the referring fund. Our recovery sequence moves from restructure or forbearance where the borrower is viable, to repossession and redeployment, lease assignment to a qualified replacement lessee, and liquidation as a last resort. Because our collateral is specific, identifiable equipment, recovery doesn’t depend on the borrower’s overall enterprise health. Equipment holds value regardless of what happens to the company.

Can you handle complex or non-standard transactions?

That’s where we differentiate from banks. We regularly handle:

- Progress-funded builds with milestone payments across multiple vendors

- International vendor deposits, including payments in foreign currency

- Transactions for borrowers at bank exposure limits

- Non-bankable credits with strong equipment collateral

- Large-ticket multi-equipment projects requiring syndication

- Sale-leaseback transactions for companies needing liquidity from existing assets

Our credit committee evaluates the full picture of the equipment, the business, and the transaction structure, rather than running a deal through an automated scorecard.

What industries and equipment types do you cover?

- Manufacturing: Production lines, CNC machinery, industrial equipment

- Medical and Healthcare: Diagnostic equipment, surgical systems, imaging technology

- Construction: Heavy equipment, cranes, yellow iron

- Pharmaceutical: Cleanroom equipment, manufacturing lines

- Food Processing and Packaging: Processing lines, commercial kitchen equipment

- Transportation: Trucks, trailers, fleet vehicles

- Energy: Power generation equipment, renewable infrastructure

- Aviation: Aircraft, engines, parts

Both new and used equipment are eligible.

What does the process look like for a referred borrower?

- Step 1: Borrower submits a 7-minute online application with financials and equipment invoice

- Step 2: Our team contacts the borrower within 15 minutes of submission

- Step 3: Credit review and underwriting — 24–48 hours for standard transactions

- Step 4: LOI issued to borrower

- Step 5: Final documentation — typically within 1–2 weeks of LOI

- Step 6: Equipment Leases wires directly to the vendor within 24 hours of executed documents

For borrowers with a master lease already in place, future equipment additions are significantly faster, often requiring only an updated invoice.

How do we start referring borrowers?

Contact our team directly. There’s no formal agreement required to make a referral, point the borrower to us and we handle everything from there. If you’d prefer to establish a formal referral arrangement or discuss how Equipment Leases can serve your broader portfolio, we’re available for that conversation at any time.

Refer a Borrower or Start a Conversation

If you work with middle-market companies that need equipment financing, Equipment Leases is built to handle it.

When to Reach Out

- A portfolio company needs equipment CAPEX and the bank is at exposure limits

- A borrower needs a progress-funded build or has complex vendor payment requirements

- A company wants to convert owned equipment into working capital via sale-leaseback

- A deal has non-standard equipment the bank won’t finance

- You want to discuss how Equipment Leases can serve your broader portfolio on an ongoing basis

What to Have Ready

- We contact the borrower within 15 minutes of application submission

- We handle underwriting, documentation, and funding

- The borrower gets their equipment financed; you stay focused on your fund’s strategy

Due Diligence Materials

Available under NDA:

- Detailed portfolio data

- Transaction-level samples

- Credit and servicing workflows

- Legal documentation framework

- Reference conversations

Confidentiality is standard practice. NDA execution can occur immediately upon request.